By Majid Ahamed

About the Company

Founded in 2000, All E Technologies Limited (Alletec) has emerged as a dominant player in the Microsoft Business Applications and Digital Transformation space. Alletec enables clients to stay competitive with Intelligent Business Applications and is now getting them ready for AI transformation. By leveraging Microsoft Dynamics 365, Power Platform, Data & AI and Azure, along with collaboration platforms – its industry specific solutions empower clients to succeed in a rapidly evolving business environment.

The solution offerings and services span through – Digital Core Modernization, Enterprise Applications, Process Optimizations, System Integration, Data & AI Solutions, and Change Management.

Alletec’s customer base resides in 30+ countries with 900+ Project Engagements.

Investment Rationale:

- The company looks to expand at a rapid pace in the coming years

- Increasing share of IP-led software, leading to margin accretion going forward

- Aims to leverage AI adoption within small and medium enterprises (SMEs) globally, by providing strategic and tailor-made AI-powered solutions for digital transformation.

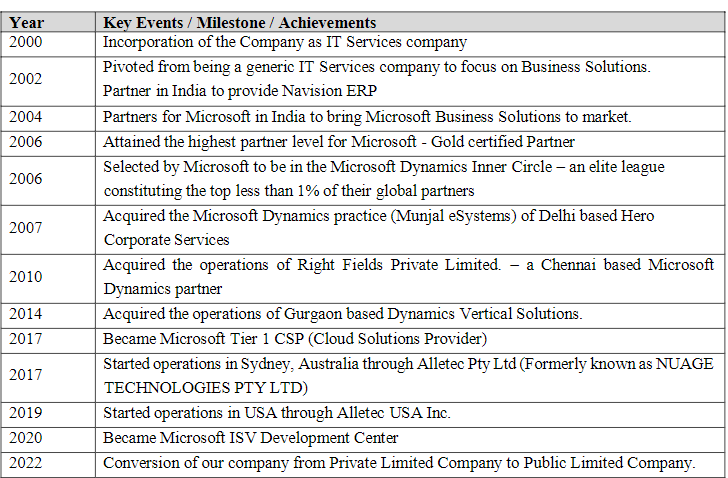

History of the Company:

Source: DRHP

Business Segments:

The core business the company operates as follows:

Digital Core Modernization: Upgrading a company’s business systems to be more efficient and scalable.

Enterprise Applications: Helping organizations manage key processes like finance, HR, and supply chains.

Process Optimizations: Improving business operations to make them more efficient through streamlined processes.

System Integration: Connecting different software systems within a company to ensure they work together seamlessly.

Data & AI Solutions: Using data analytics and artificial intelligence to help businesses make smarter, faster decisions.

Geographical Classification

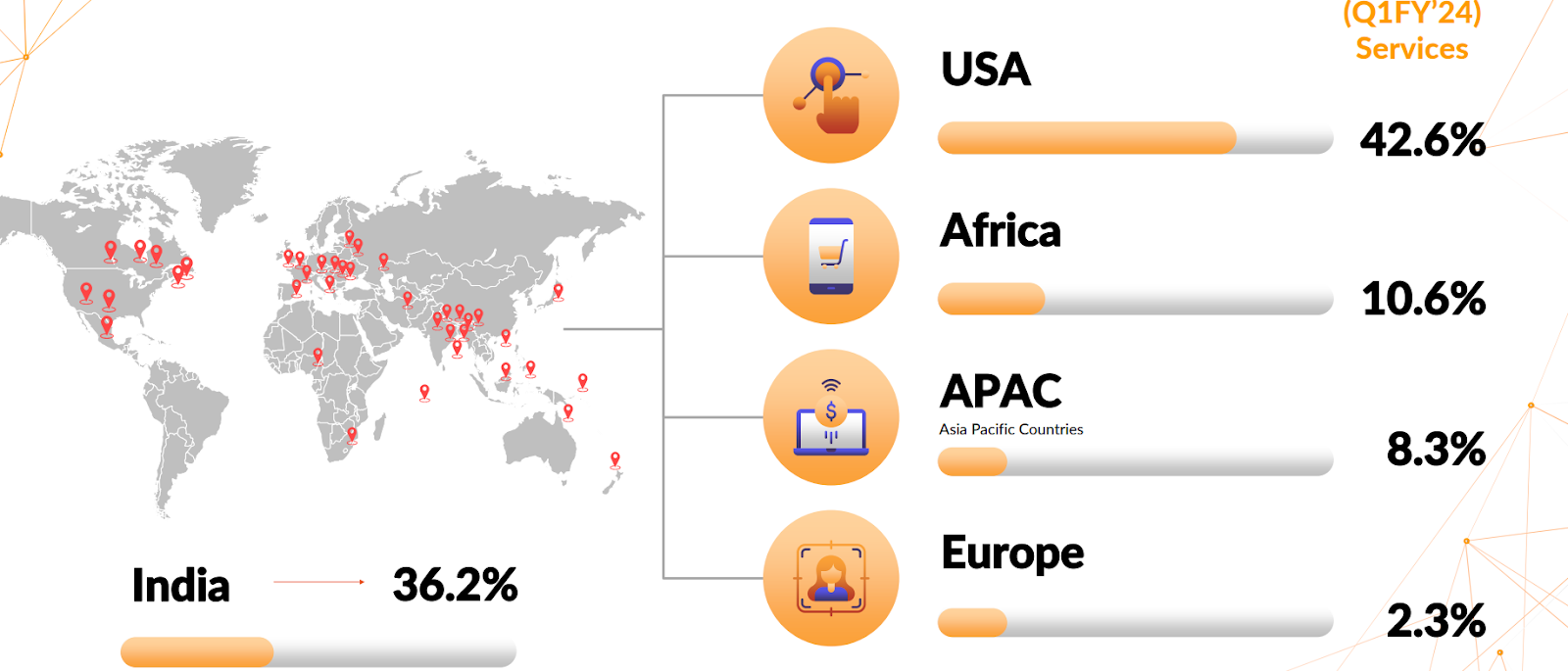

In Q1 FY25, most of Alletec’s customers were from the US market, which contributes over 60% to the top line, followed by India at 25% and Africa at 5.3%. In comparison, during Q1 FY24, the US contribution was 42.6%, with India at 36.2%. This represents a significant increase in the US market contribution, from 42.6% to 60%, while the exposure in India and Africa has reduced notably, with a slight increase in the European region.

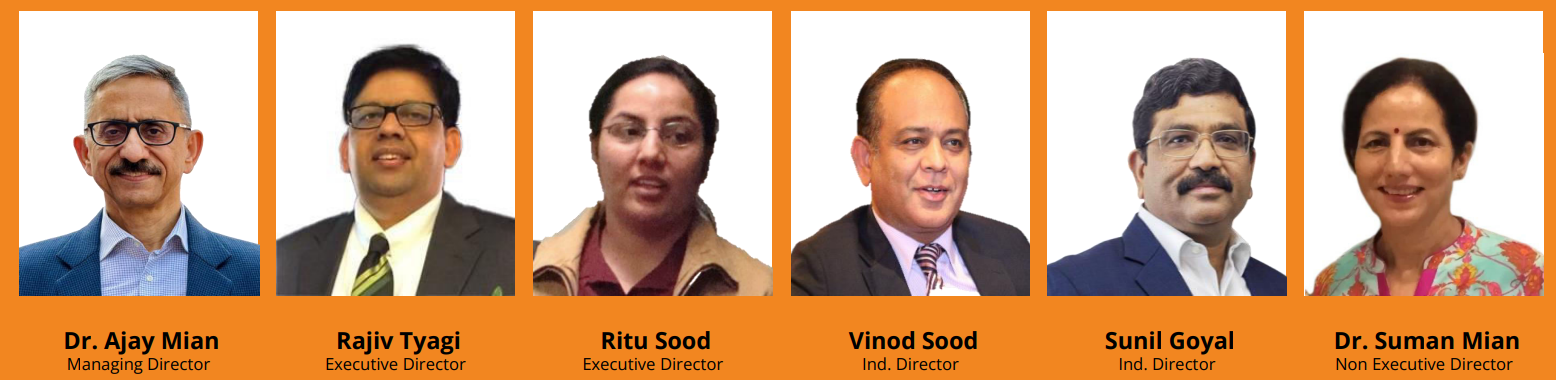

Management

- Dr. Ajay Mian (MD & CEO):

- Has around 20 years of experience in Digital Transformation.

- The driving force behind the company’s success and growth.

- Mr. Rajiv Tyagi (Executive Director):

- Over 25 years of experience in the computer software industry.

- Strong expertise in Finance, Supply Chain, and CRM.

Promoter Stake:

- The promoter currently holds a 50% stake in the business, which is considered reasonable for the size of the company.

Board Composition:

- The company’s board consists of experienced members with over 25 years of experience in IT & Digital Transformation Services.

- Dr. Suman Mian, wife of the MD and a qualified medical doctor, assists with the company’s administration.

Deep-Dive on the Investment Rationale

The company looks to expand at a rapid pace in the coming years

The company is expecting 25-30% annualized growth in the short to medium term, as it expands its offerings and adds new customers on a quarterly basis. In Q1 FY25, the company added 15 new customers and anticipates continued growth, supported by the overall expansion of the Microsoft Business Application market, which is projected to reach USD 51 billion by 2025, with an annual growth rate of 20%.

The company is actively pursuing M&A opportunities to enhance its offerings and diversify its services beyond reliance on Microsoft. With a strategic focus on mergers, acquisitions, and organic growth—particularly in international markets—the company presents a strong investment rationale for long-term capital compounding.

Increasing share of IP-led software, leading to margin accretion going forward

The business contributes 10-11% from IP-led solutions overall, which has resulted in high customer retention rates of over 90%. By offering personalized solutions rather than just standard IT services, the company sets itself apart. As they scale their offerings, the potential for operational leverage increases, which is expected to boost margins in the coming years. Their customizable IP-led software provides a key competitive edge in the market.

Aims to leverage AI adoption within small and medium enterprises (SMEs) globally, by providing strategic and tailor-made AI-powered solutions for digital transformation.

With the rise of Generative AI and other AI tools, widespread adoption is underway, presenting a significant opportunity for the business to capitalize on. Their AI-led solutions, integrated with the Microsoft platform, position the company to offer customized solutions that drive rapid growth. As of 2023, the global AI market is valued at $207.9 billion and is projected to surge by 788.64%, reaching $1.87 trillion by 2030. This market is expected to grow at an annualized rate of 18-20%.

The company’s focus on bolt-on acquisitions and an expanding portfolio of marquee clients—such as Manipal Education, MakeMyTrip, Microchip USA, New York Cosmetics, and Yatra—supports its strong growth trajectory in this fast-evolving space.

Risk/Threats

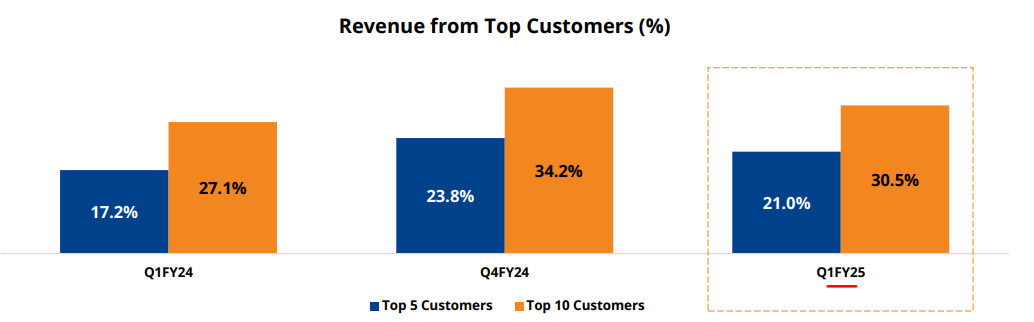

Customer Concentration: The customer concentration for TOP 5 customers stood Q1FY25 at 21% and TOP 10 Customers for 30.5%, though there has been decrease in sequently, with a slight increase in YoY basis, this is a key risk the company have as losing a major customer could a material impact in the company’s revenue and earnings.

Microsoft Software Concentration: The company currently has Microsoft as their partner for IT solutions. While Microsoft is a great business with strong market acceptance, it is important for the company to diversify to other providers. There are multiple companies, like Odoo for Finance, that can offer software suites for businesses. By diversifying their partnerships, the company can remain flexible and adaptable to changes in trends. Relying solely on Microsoft could impact the company’s future growth if there is a shift towards other applications.

Delays in M&A: The company raised around ₹10 crore from its IPO for acquisitions, but after two years, they have yet to acquire any company. Although they have sent Letters of Intent (LOI) to potential targets, they are still awaiting responses. This delay of over two years raises concerns and is considered a risk. It is crucial for the company to maintain valuation discipline and partner strategically to grow the business. If they are unable to find a suitable acquisition, they may need to deploy those funds into organic growth to expand the business.

Intense Competition: The company faces intense competition, particularly from the Big Four (EY, Deloitte, KPMG, and PwC), which poses a significant risk to their IT solutions business. If the company fails to adapt to the latest technological advancements and strategically build competitive IP-led solutions, they may face challenges in margin expansion as they scale. The heightened competition makes it imperative for the company to stay ahead with innovative offerings.

Financial Analysis & Valuation

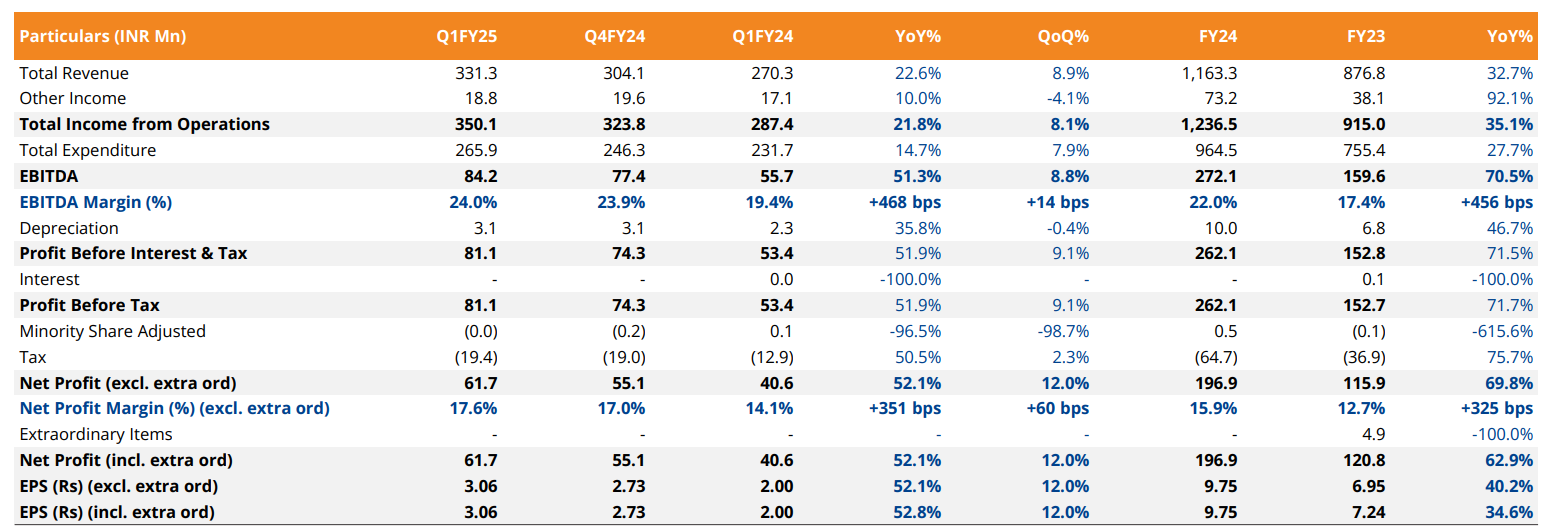

The company has grown its revenue by 32% year-over-year (YoY). It has increased its EBITDA margins by 456 basis points (bps) YoY, and the net profit margin has improved by 325 bps, from 12.7% to 15.9%. Net profit has increased by 63%. The company has an operating leverage of 2 times, meaning that as sales increase, the EBITDA or operating margin would increase twice as much. The Return on Capital Employed (ROCE) is very good and healthy, ranging from 21% to 24%, primarily due to higher net profit. The company fundamentally looks healthy and strong, with no debt on the balance sheet.

Valuation

As of September 12th, the company’s market capitalization stands at ₹922 Crores, with a trailing twelve months (TTM) P/E ratio of 42.3. Judging this business solely based on the P/E ratio, it appears expensive. However, considering the EPS growth in the range of 35-40%, primarily due to high operating leverage, the business shows strong growth potential. The company is focused on expanding into global markets, introducing new offerings, and looking to acquire new businesses. With rapid expansion of new customers and a high retention rate of 90%, the business is reasonably valued with strong prospects. The adoption of AI and data analytics is crucial for scaling, and the company is a strong provider with their IP-led solutions globally.

Disclaimer: This article is in no way a recommendation to buy or sell the stock being mentioned or talked about above.