About the Company

MPL is a customer-centric pharmaceutical company. It is one of the leading pharmaceutical companies with a strong foothold in highly regulated markets, specializing in OTC and prescription (Rx) drugs.

The company operates primarily in two segments:

- OTC

- RX

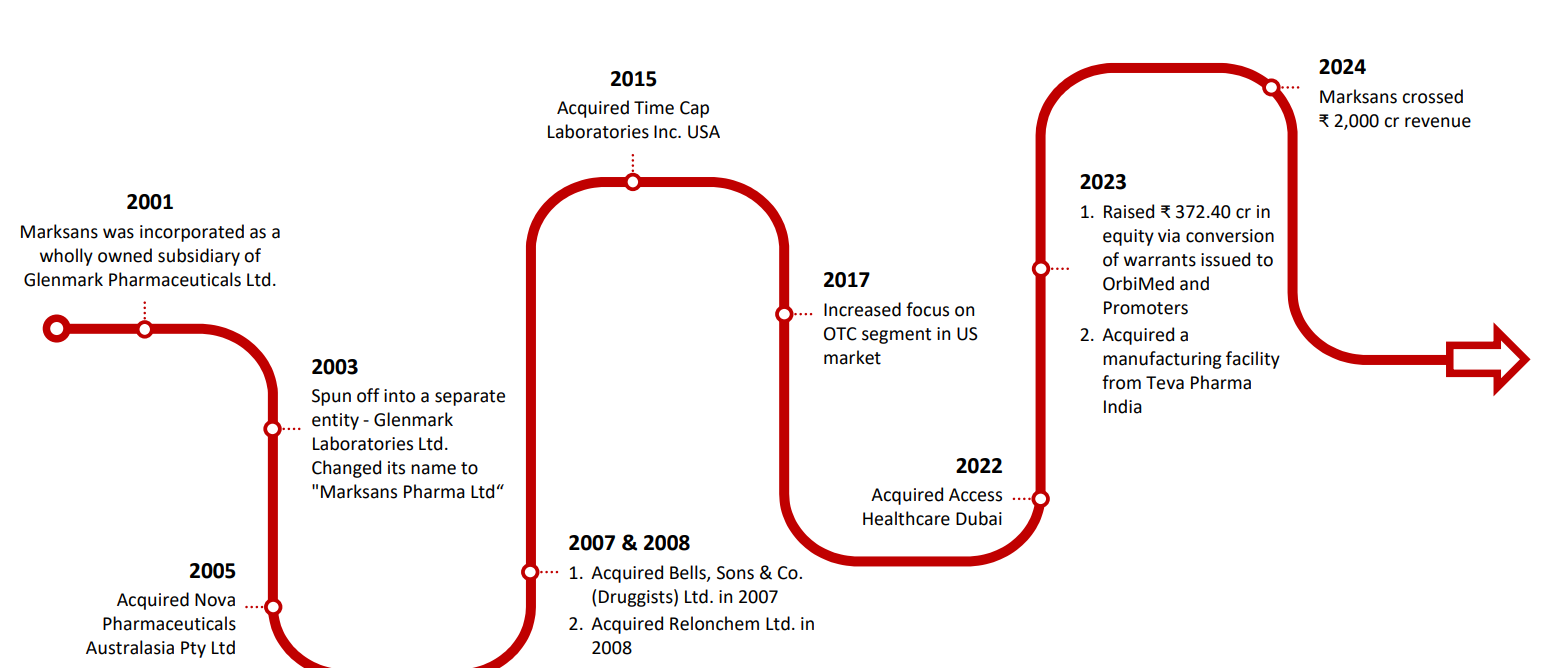

History of the Company:

Source: Investor Presentation

Business Segments:

OTC Segment

The OTC segment involves the sale of generic medicines directly in the marketplace. This includes products for pain management, cough, and cold. The OTC market comprises drugs that are available without a prescription and are intended for self-care. These medicines are sold directly to customers, and this segment alone contributes nearly 75% of the total revenue.

Rx Segment

The Rx segment involves pharmaceuticals that require a doctor’s prescription and are dispensed by licensed pharmacists. This segment focuses on specialized medicines, which are generally high-margin but come with a high risk of price erosion. The Rx segment contributes nearly 23–25% of the total revenue.

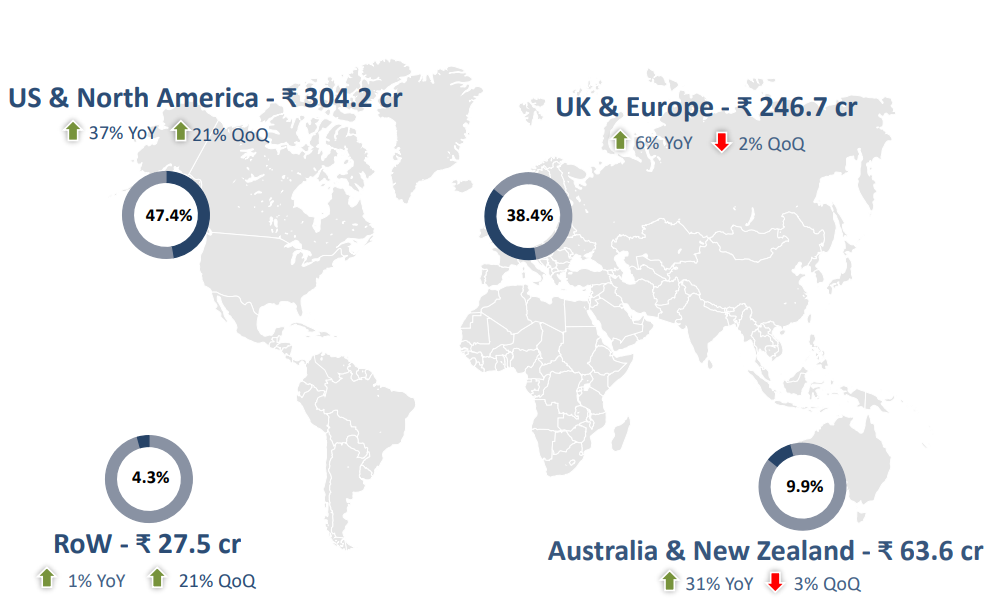

Geographical Classification

The majority of the income comes from the US and North America, contributing 48% of the total revenue in Q2FY25. The UK and Europe follow, accounting for 38.4% of the overall revenue. Australia and New Zealand contribute 9.9%, while the remaining 4.3% comes from other countries.

Case Study Report

- THE ENTRY STAGE & Rationale Behind it

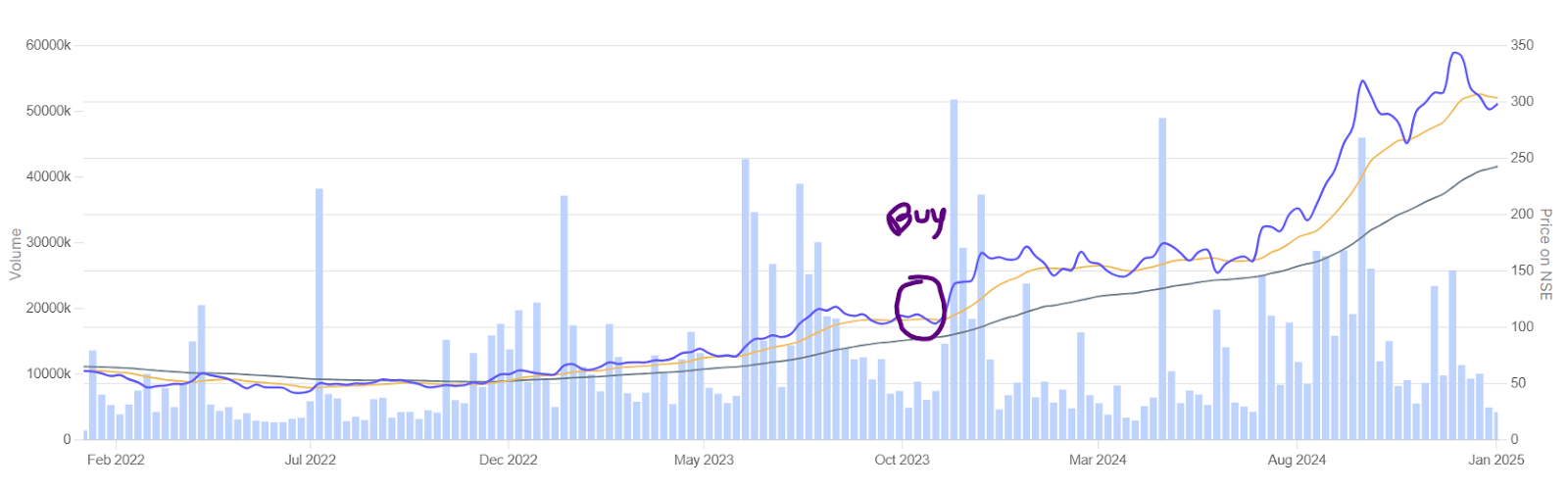

- Our firm invested in the company in October 2023 at a price range of ₹106. At that time, the company announced the acquisition of Teva’s factory in Goa, signaling a strategic move toward effective capital deployment. As of FY23, the company reported cash reserves of approximately ₹715 crores, primarily driven by a capital raise through preferential allotment to marquee investors.

- At that time, the company’s market capitalization stood at around ₹4,300 crores, meaning its cash-to-market capitalization ratio was approximately 17%—significantly higher compared to peers in the industry. This robust cash position highlighted the company’s financial strength, particularly in the highly competitive OTC and Rx market segments.

- However, the company has faced significant stagnation in recent years, following the post-pharma boom in FY21, making its strategic actions and capital deployment initiatives crucial for future growth.

- The company revived strategically in the developed markets and has invested in brands and deep penetration in those developed markets after getting the required medicines in the region that had led to strong revenue growth and margin expansion for the company the key geography that is leading the growth in US & UK market, wherein they have focused on deep penetration and taking away market share through new product launches in this market which led to the strong revenue and PAT growth, with the upcoming capacity utilization that occurred in the newly acquired facility in GOA.

- As the company started delivering growth in subsequent quarters, a major FII, The Endowment Fund of Massachusetts Institute of Technology, took a stake in the business. Investors in the retail side increased as well, from 2.07 Lakh investors in Q2FY24 to 2.48 Lakh investors in Q2FY25.

- Where the company’s sales growth started to moderate post Q3FY24, and then in Q4FY24 there was a sharp dip in the margins for the company sequentially of over 300 bps that had led to negative profit growth for the company.

The rationale behind the EXIT of the company

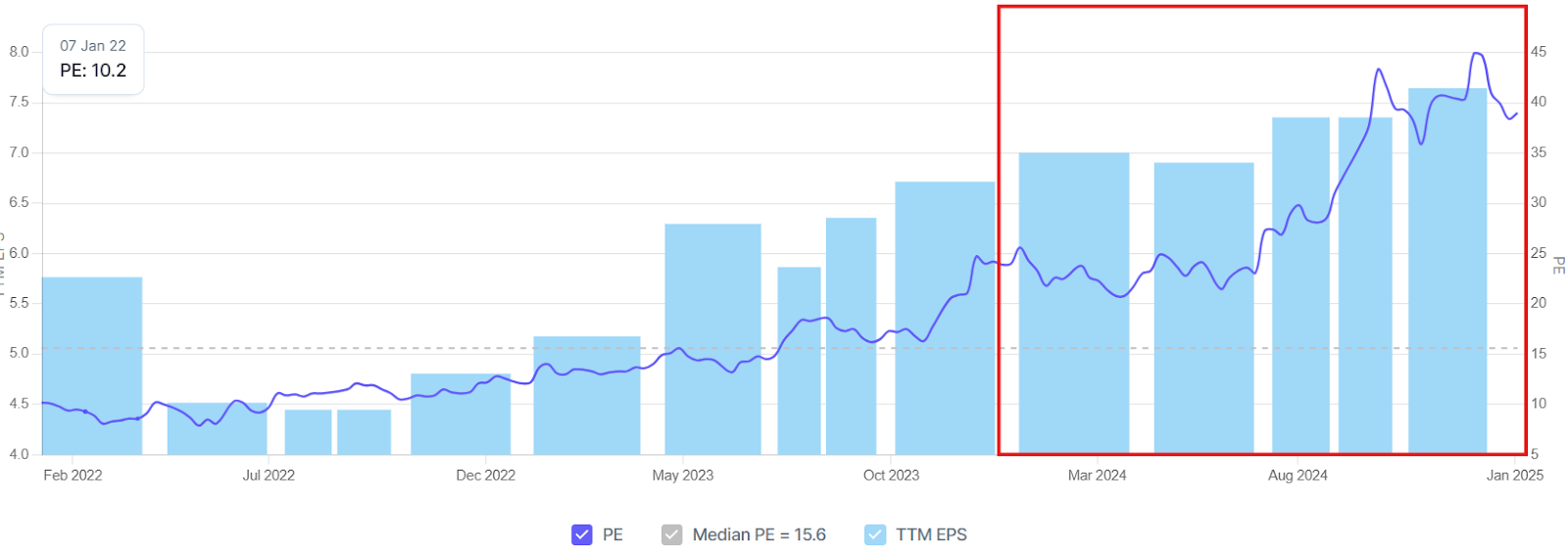

- At this pace the company was also trading at a very high multiple, from a median multiple for the company was in the range of 15-16 times earnings, and at the time, we sold it was trading at a very high multiple of over 40 times nearly 2.5 times from the initially invested multiples whereas the earnings growth started to taper due to the fact there is price issue in the developed markets.

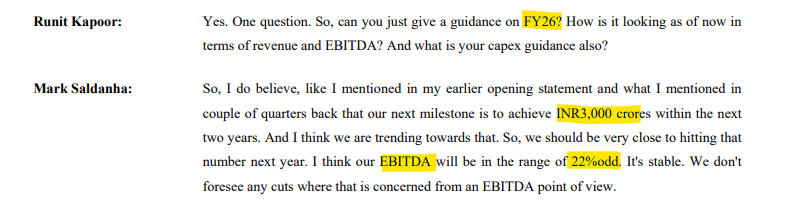

- As per the recent conference call with the analyst, the company has provided guidance for FY26, projecting revenue of ₹3,000 crores with an EBITDA margin of 22%, resulting in an estimated EBITDA of ₹660 crores. This implies a forward EV/EBITDA multiple of 19.75x for FY26, compared to the current EV/EBITDA multiple of 23.5x. Even if the stock continues to trade at its current multiple, the forward return potential for investors over the next two years would be approximately 18%, leaving limited upside for investors.

- Given that all optionality and the bull case have already been priced into the market, the company’s P/E ratio reflects the high growth expectations in the business. As a result, we decided to exit our position in October 2024, achieving strong returns for investors who were invested in the company.