Jay Bee Laminations Ltd.

31 October 2024

By Majid Ahamed

About the Company

Jay Bee Laminations Limited was established in 1988 as a manufacturer of CRGO Silicon steel cores for the emerging power & distribution transformer industry of India.

With two manufacturing units in Noida (UP), they have developed facilities for the supply of CRGO & CRNGO steel cores with applications in transformers, inverters, reactors & rectifiers. Various reputed manufacturers of distribution and power transformers rely on Jaybee for world-class products and an excellent quality of collaboration. With production facilities spread across a total area of 117,090 sq. ft, with a current capacity they have established our core competencies in the design, development, and manufacturing of Electrical steel cores conforming to global quality standards.

The major products the company sells are as follows:

- Slit Coils

- Cut Laminations

- Assembled Cores

- Others

Investment Rationale:

- The power transformer industry is experiencing strong tailwinds, with a diversified focus on both power and distribution transformers.

- The company is well-positioned to capitalize on the ongoing capital expenditure, supported by strong market positioning and marquee clientele.

- Strong management pedigree and very low order rejection rates are expected to support the company’s sustained growth.

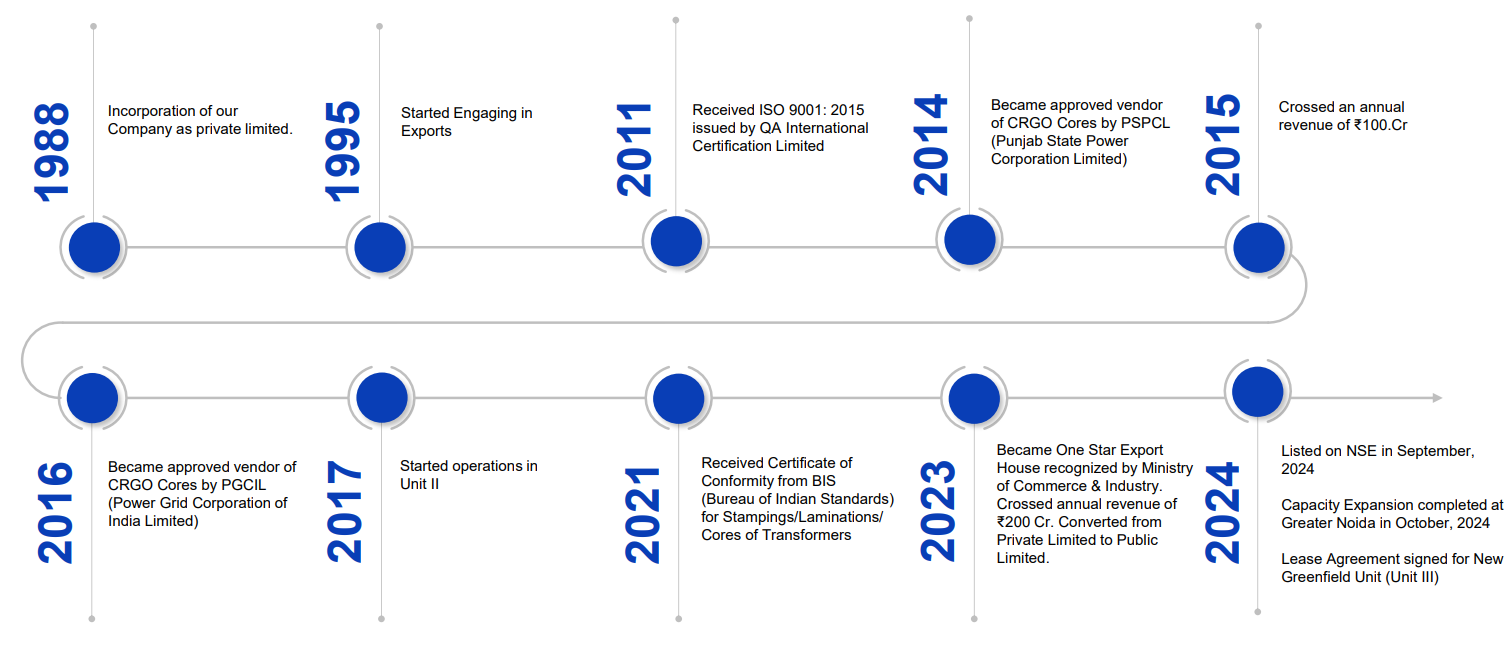

History of the Company:

Source: Investor Presentation

Product Segments:

The company has the following product segments as follows:

Slit Coils

The Slit Coils, where the CRGO & CRGNO steels mother coils undergo processing through slitting to be transformed into slit coils. This operation is carried out utilizing high-speed semi-automatic slitting machines, where the Slit Coils contributed 4.6% of the total revenue in FY24

Cut Laminations

The Cut Lamination Product is the next step of the process, where the silt coils are cut to laminations with the assistance of automatic CNC Cutto-length machines. This segment makes, most of the revenue where the cut lamination alone contributes around 75.4% of the total revenue in FY24

Assembled Core

Assembly involves a manual labor-intensive process of stacking cut lamination sheets atop each other and securely clamping them using channels, bolts, and insulation material to form an assembled core. The Assembled Core segment contributed around 17.45% of the total revenue in FY24.

Geographical Classification

The majority of the Income comes from India which contributed 88-90% of the total revenue in FY24, Exports Contributed 10-12% of the overall revenue in FY24.

Management

- The company’s management is led by Mr. Munish Kumar Aggarwal (Chairman) who has nearly 32 years in the industry.

- Mr. Mudit Aggarwal, the son of the Chairman has nearly 12 years working in the company as the Managing Director and has a qualified Master’s in Engineering, from Columbia University

- Ms. Sunita Aggarwal, the wife of the Chairman has more than 26 years of experience in the field of Human Resources and administration of the company and has been Director since 1992

- The promoter currently has a 70.41% stake in the business, which is reasonable for the size of the business

- The company’s board comprises experienced members with backgrounds in the field of plastic manufacturing, law, and the field of public sectors enterprise which ensures strong diversity among the board of directors

- But there is again concern about the salary for Ms. Priya Jain the wife of Mr. Mudit Aggarwal through the related party transaction of 18 lakh p.a this is a related party transaction given to a family member without any designation or work in the company. It brings skepticism when in the case of the public company

Deep-Dive on the Investment Rationale

Strong Tailwind the power transformer Industry, with a diversified focus on both power and distribution transformers

The company earlier was only serving the distribution transformers, currently, the company as H1FY25 has a very good mix of both Power and as well Distribution Transformers with a mix of 50%, Power and 40% Distribution Transformers, as in the Power Transformer generally the transformer which is been built would cost 5 to 25 crores with that high capital investment required for such transformers there is high scrutiny for the cores that needs to installed, where in Jaybee has well positioned and have got approval for Power Grid of 220 KV, and the company expects to get approvals from the clients on the approved vendor for the 400 KV and 768 KV.

The company will position to capitalize on the ongoing capex with a strong market positioning and marque clientele

The company has seen a strong order flow from well-known companies in the transformer industry. With the projected growth of 12-13% CAGR in this sector, the company has leased new land in Noida to increase its production capacity for 400 KV and 765 KV transformers. This expansion is expected to help the company grow and enhance its market share.

Additionally, to diversify, the company plans to increase its capacity for Amorphous Core production, positioning itself to capitalize on anticipated industry growth over the next two years. Capacity for CRGO steel production is also expected to increase, from 9,400 tonnes to 25,000 tonnes by FY26. The company’s total addressable market (TAM) is currently valued at 3 lakh, with a market share of 3%, which is projected to increase to 5-6%.

The company maintains strong relationships with key players, including Skipper Ltd, BHEL, Indo Tech, Voltech, and Shilchar. For end clients, it has secured critical approvals for power transmission from Adani Gas and Power Grid Corporation of India.

Strong management pedigree and very low order rejection rates are expected to support the company’s sustained growth.

The company, with a small capitalization of less than 1000 crores, benefits from a strong management pedigree in both educational qualifications and quality of experience accumulated over the years. For instance, Mr. Mudit Aggarwal, a qualified engineer from Columbia University, USA, brings nearly 12 years of experience to the company. His expertise has been instrumental in securing additional orders while maintaining a low rejection rate of less than 0.7%.

The company’s robust management, complemented by strong operating cash flow—growing from 3 crores in FY22 to 16 crores in FY24—supports sustainable growth without requiring significant additional working capital financing.

Risk/Threats

Competitive Intensity: The company faces stiff competition from both organized and unorganized players, including both listed and unlisted entities. With 10-15 organized players in the industry, it is crucial for the company to focus on value-added products and leverage economies of scale to build a robust business model and drive growth.

High Dependency on Suppliers: The company is highly dependent on suppliers for raw materials, especially CRGO steel, which is not produced in India. Approximately 30-40% of these materials are sourced from China, which poses a risk in the event of geopolitical tensions. To mitigate this, the company has been developing close relationships with domestic stocking centers. As of H1 FY25, the company has made progress in diversifying its supply sources to reduce dependency on imports.

Higher Operating Leverage: The company has a high operating leverage, with a ratio of 1.5x. This implies that a 10% increase in revenue could lead to a 15% increase in profits, while a 10% revenue decline could result in a 15% decrease in profits. This creates a significant risk, as any slowdown in revenue growth could heavily impact profitability. Effectively managing this leverage is critical to the company’s financial stability.

Exposure to Cyclicality in End-User Industries: The company’s growth is closely tied to the transformer industry, which is cyclical and heavily dependent on government capital expenditure. Any slowdown in government spending could directly impact the company’s growth prospects. The industry faced significant challenges between 2010 and 2020, highlighting the importance of managing cyclicality risks. Investors should be aware of the cyclical nature of the transmission industry, as it directly affects this business.

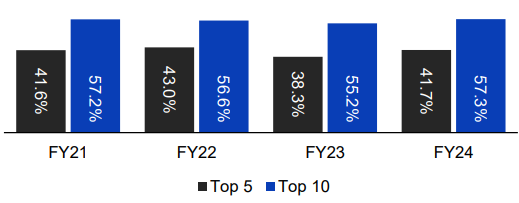

High Customer Concentration:

The company has a customer concentration of the top 5 contributing to 41.7%, top 10 customer concentration of 57.3%. This makes the company makes it quite risky, where even leaving major customers could significantly decelerate the company’s revenue growth, and impact the earnings the company, hence this needs to be tracked.

Valuation

As of November 1st, the company’s market capitalization stands at ₹783 crores, with a trailing twelve-month (TTM) P/E ratio of 40.4 and an EV/EBITDA of 23.6x. This valuation appears reasonably valued; however, the company has strong volume growth with a projected CAGR of over 30%. The company’s strategy includes sourcing materials domestically, improving end-customer licensing, and focusing on increasing the power transmission contribution to the overall volume, supported by growth drivers such as rising demand in the electricity primarily due to increase in data centers and increased government capital expenditure in the power sector.

The company is well-positioned to benefit from these favorable conditions, making it a strong investment thesis. In comparison, unlisted competitors like Kryfs struggle with profitability, achieving only around a 4% PAT margin, while other players like Amod Stampings and Vardhman Stampings demonstrate healthy growth with robust PAT margins, which ensures the Industry overall has a strong potential to grow in the coming years.

However, potential investors should consider risks such as the cyclicality of end-user industries, high working capital requirements, customer concentration, and supply chain dependencies in terms of key suppliers and geographical regions. These factors should be carefully evaluated before investing in this business.