Techno Electric & Engineering Co Ltd.

10 November 2024

By Majid Ahamed

About the Company

Techno Electric & Engineering Company Limited (TEECL) builds, operates, and maintains high-end power infrastructure for electricity generation, transmission, and distribution. The company has strengthened its capabilities in delivering advanced and sustainable power solutions, including high-voltage direct current (HVDC) transmission, Flue Gas Desulphurisation (FGD), and Advanced Metering Infrastructure (AMIs).

Its portfolio comprises the successful execution of over 400 projects in India and overseas, facilitated by a team of 400 experienced and young professionals. In 2021, it ventured into the data center domain by building on its extensive and multidisciplinary electrical, mechanical, civil, and structural engineering expertise. With a vision to revolutionize digital infrastructure, TEECL is dedicated to establishing data centers with an investment of US$1 billion by FY2030.

The company operates primarily in Four segments:

- Power Generation

- Transmission

- Distribution

- Data Centers

Investment Rationale:

- Strong Book Inflow is expected to increase in the coming years, which would drive strong and sustainable revenue and profit growth

- Strong Focus and Investment in Data Centers which is going to be a key growth lever that would accelerate the revenue and earnings growth in the coming years

- Increased Expenditure in Smart Meter would be another trend and growth setter that would boost its EPC business with a 5 lakh crore commitment from the government

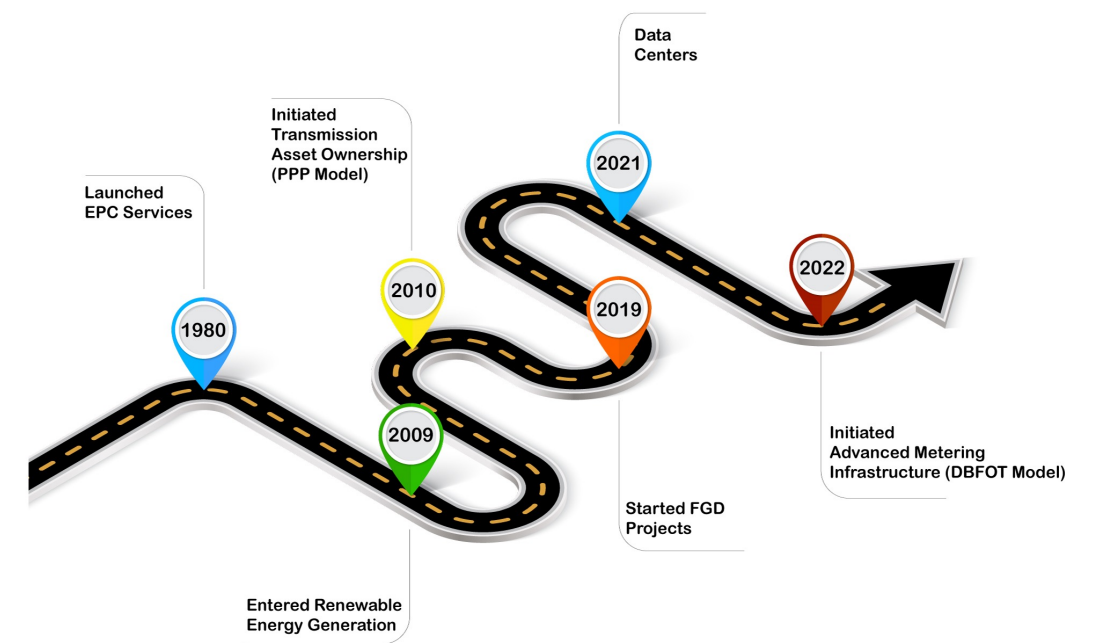

History of the Company:

Source: Investor Presentation

Business Segments:

EPC Business Overview

- Power Generation: The company provides engineering, procurement, and construction (EPC) services for power plants, focusing on Balance of Plant (BOP) works for thermal power. It deploys advanced technologies such as flue gas desulfurization (FGD) systems to reduce emissions and improve plant efficiency. Turnkey solutions include captive power plants up to 200 MW, utilizing waste heat recovery to maximize efficiency for industrial clients. Current projects include FGD installations at thermal power stations in Bokaro, Jharkhand (500 MW); Jhalawar, Rajasthan (two 600 MW units); and Kota, Rajasthan (210 MW and two 195 MW units).

- Transmission: The company specializes in EPC for substations, supporting capacities from 220 kV to 765 kV for both public and private clients. Expertise includes extra high voltage substations, air and gas-insulated switchgear, and grid stability solutions like static synchronous compensators up to 300 MVar.

- Distribution: The company undertakes rural electrification projects and provides digital solutions for distribution companies, including advanced metering infrastructure (AMI) and smart metering for enhanced energy management and billing accuracy.

Transmission & Distribution Assets: The company frequently partners with government entities on DBFOOT (design, build, finance, own, operate, and transfer) projects. It has completed three transmission projects in Haryana, Punjab, and Nagaland and has secured bids for two new 400 kV projects in Assam. In 2024, it won contracts for projects in Assam under the North-Eastern Region Generation Expansion Scheme-I.

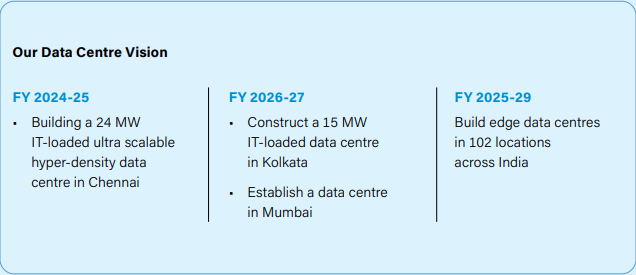

Data Centres: Expanding into data centers in 2021, the company launched a hyperscale facility in Chennai (40 MW capacity) and has acquired land for a new center in Kolkata. It has also partnered with RailTel Corporation to develop and maintain edge data centers in 102 cities across India over the next five years.

Geographical Classification

The majority of the Income comes from India which contributed nearly 100% of the total revenue in FY24.

Management

- The company’s management is led by Mr. P. P Gupta (MD) who has nearly 40 years in this industry and has experience in merchant banking and worked as a Management Consultant in BHEL. He holds a Bachelor’s degree in engineering and a Master’s in business management from the Indian Institute of Management (IIM) in Ahmedabad

- Mr. Ankit Saraiya (WTD) He is a highly accomplished individual with a Bachelor’s degree in science, specializing in corporate finance and accounting) from Bentley University in Waltham, Massachusetts, US. Mr. Saraiya has been instrumental in driving TEECL’s ambitious diversification into anti-emission and digital infrastructure initiatives.

- The company has a board of directors who have extensive experience in M&A, Engineering, Investments, and the Energy & Power Industry which makes the board is well-positioned with industry experts and professionals

- There has been concern in terms of increment equity dilution made by the company where the company’s stake has reduced from 61.52% to 56.93%

Deep-Dive on the Investment Rationale

Strong Order Book Inflow is expected to increase in the coming years, which would drive strong and sustainable revenue and profit growth

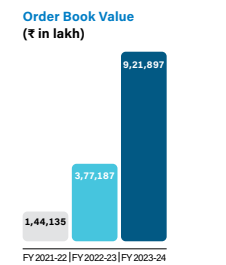

Key growth drivers and levers for the company include a strong order book, as the company received in FY24, as of FY23 the company had an order book of around 3771 crores, and currently as of H1FY25 the company has an order book of over 9200 crores, which is set to execute in the next 2-3 years of the company, the company is well-diversified order book portfolio across the power, transmission, distribution (smart meters) and Data Centers with a strong tie-up with Global MNC in terms of tech collaboration with a marquee client in terms of the Order book inflow ensures the company is set to grow at a faster pace with sustained growth in the coming years.

Strong Focus and Investment in Data Centers which is going to be a key growth lever that would accelerate the pace of growth and profitability in the coming years

The company is well set to grow in the data center business by investing massively in the space by building data centers in Chennai and Kolkata, currently by Q3FY25 the company’s phase 1 data center is set to be operational, and this data center will hyperscaler where the data center is given for company’s for their intensive cloud computing, and they have acquired the land in Kolkata which is expected to be operational in FY27, along with that company had made a tie-up RailTel Ltd in building 100 edge data centers across the nation with a expected investments over 1000 crores with a massive growth in the industry of over 43% CAGR coupled with strong execution capability makes the company exponentially in this segment would drive significant growth with strong margin expansion as expected EBITDA margin in this segment would be north of 65%+.“We are committed to revolutionizing digital infrastructure with an ambitious investment of $1 billion by FY 2029-30. We focus on building ultra-scalable, hyperdensity data centers that align with India’s growing demand for robust digital infrastructure and contribute to the nation’s technological advancement.”

Increased Expenditure in Smart Meter would be another trend and growth setter that would boost its EPC business with a 5 lakh crore commitment from the government

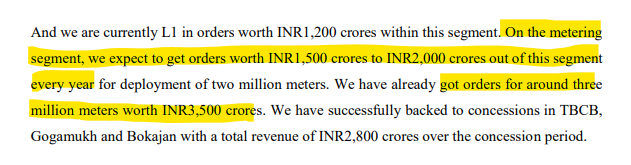

The company is capitalizing on the growth in the smart meters which is expected to a strong budget allocation of 5 lakh crores from the central government, the company has a strong order book of around 2000 crores to install 2 million smart meters where the company expects to have a 1000-2500 crore order book annually in these segment which again would drive the growth strong as they execution becomes stronger and robust. The company is also actively bidding on projects for 40 lakh meters, totaling ₹4,500 crore, which drive the growth exponentially in the coming years.

Risk/Threats

Raw Material Volatility:

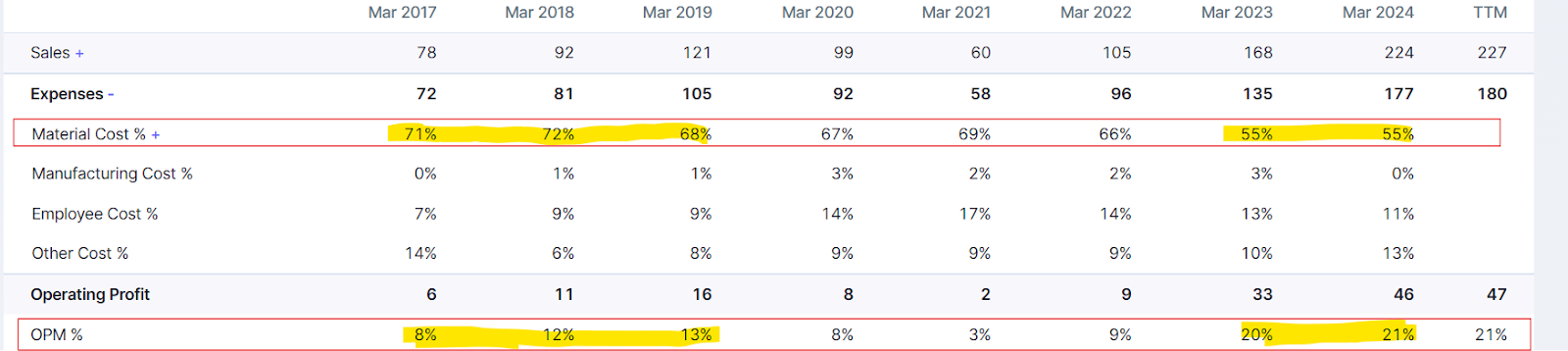

If we can see the P&L statement majority of the cost of the company has been material cost, as we can see how the raw material prices have been fluctuating over the year from FY17-19 where the prices were at peak led to margin contraction over the year the prices of steel and allied materials prices has been moderated due to shift from EPC model to Data Centers and other division which made company significantly goes down, that being said there is a risk of high raw material prices which out would effect EPC portion of the business.

Working Capital Intensive Business:

The company operates a highly working capital-intensive business, especially in its EPC segment. It must collect payments (receivables) from government bodies while purchasing materials from suppliers, which has led to significant working capital demands. This strain on cash flow has resulted in negative operating cash flows and slowed down growth, prompting the company to raise funds through equity, and leading to share dilution.

Currently, the company’s working capital is heavily tied up, with debtor days (the time taken to collect payments) exceeding 150 days, though it has managed payables more effectively since FY22. Effective working capital management is crucial for the company to achieve sustainable growth.

Competitive Intensity: The company faces stiff competition from established players in each segment of EPC model where they’re big contractors such as Kalpatru, Tata Projects, Anant Raj in Data Centers where the company has many organized players competing, which would again be a major risk as the company’s high return and the profit pool would decrease with multiple players trying to get orders, its essential the company can build strong and order pipeline with the government to ensure they can grow sustainably with the very intensive competition across segments.

Poor CFO to PAT Conversion: The company has extremely poor CFO to PAT conversion where the company has a 30-35% conversion of the CFO to PAT, and they had multiple issues in the cash flow conversion of the company the company’s earnings over the years, as a result, the company has diluted the equity and started raising a massive amount of capital and have invested in shares and bonds.

Valuation

As of November 8th, the company’s market capitalization stood at ₹19,248 crore, with a P/E ratio of 65x. This valuation appears high, considering the cyclical nature of earnings in this sector and the multiple regulatory risks involved.

The company is shifting focus toward the data center segment, which shows strong growth potential, projected at a 40-45% CAGR over the next five years. This shift could drive revenue growth and profitability in the coming years, especially with a data center under development. Phase 1 of this project is expected to be operational in Q3 FY25, at which demand and execution in this segment can be better assessed.

In the smart meter segment, the company is well-positioned with a solid order book and the growing need for smart meter replacements. It is pursuing both EPC and DBFOOT (design, build, finance, own, operate, and transfer) models, which could generate steady revenue over the next 20 years.

While the company’s growth has been impressive, its valuation remains high, and further P/E expansion is speculative. Earnings growth will likely drive future returns, but translating profits into cash flow remains a concern. Additionally, the company has been raising capital through QIPs, leading to equity dilution, which requires monitoring.

In summary, while the company demonstrates growth potential, investors should remain cautious of associated risks, including client concentration, high working capital requirements, regulatory changes, and weak cash flow from operations (CFO) conversion. Careful monitoring and analysis of these factors are essential before making an investment decision.