Opening a Demat Account (Including NRIs!)

"The bazaar is open. Your broker is ready. Now you need the right pass; and it's a three-part system."

In the previous Article, you chose your broker.

Now comes the part that intimidates most beginners: the paperwork.

But I want you to take a breath, because what sounds complicated is actually a clean, logical three-account system; and once you understand what each account does, the whole thing clicks instantly.

The Three Accounts, Simply Explained

Think of it as a pipeline that money and shares flow through in one direction when you buy, and in reverse when you sell.

Your Bank Account is the starting point; the reservoir of funds. Your salary arrives here, your bills leave from here, and your investing capital begins its journey from here. You almost certainly already have one.

Your Trading Account is the active desk; the interface where you actually place buy and sell orders. When you tap "Buy 5 shares of Infosys," that instruction goes through your trading account. It holds your funds temporarily while an order is being executed.

Your Demat Account (short for Dematerialised Account) is your digital locker. The moment your purchase is complete, the shares arrive here and sit safely under your name; not as physical certificates (those went out of fashion decades ago) but as electronic entries, secured by SEBI-regulated depositories called NSDL and CDSL.

The flow, simply put: Money leaves Bank → Order placed via Trading Account → Shares land in Demat Account.

That's the whole pipeline.

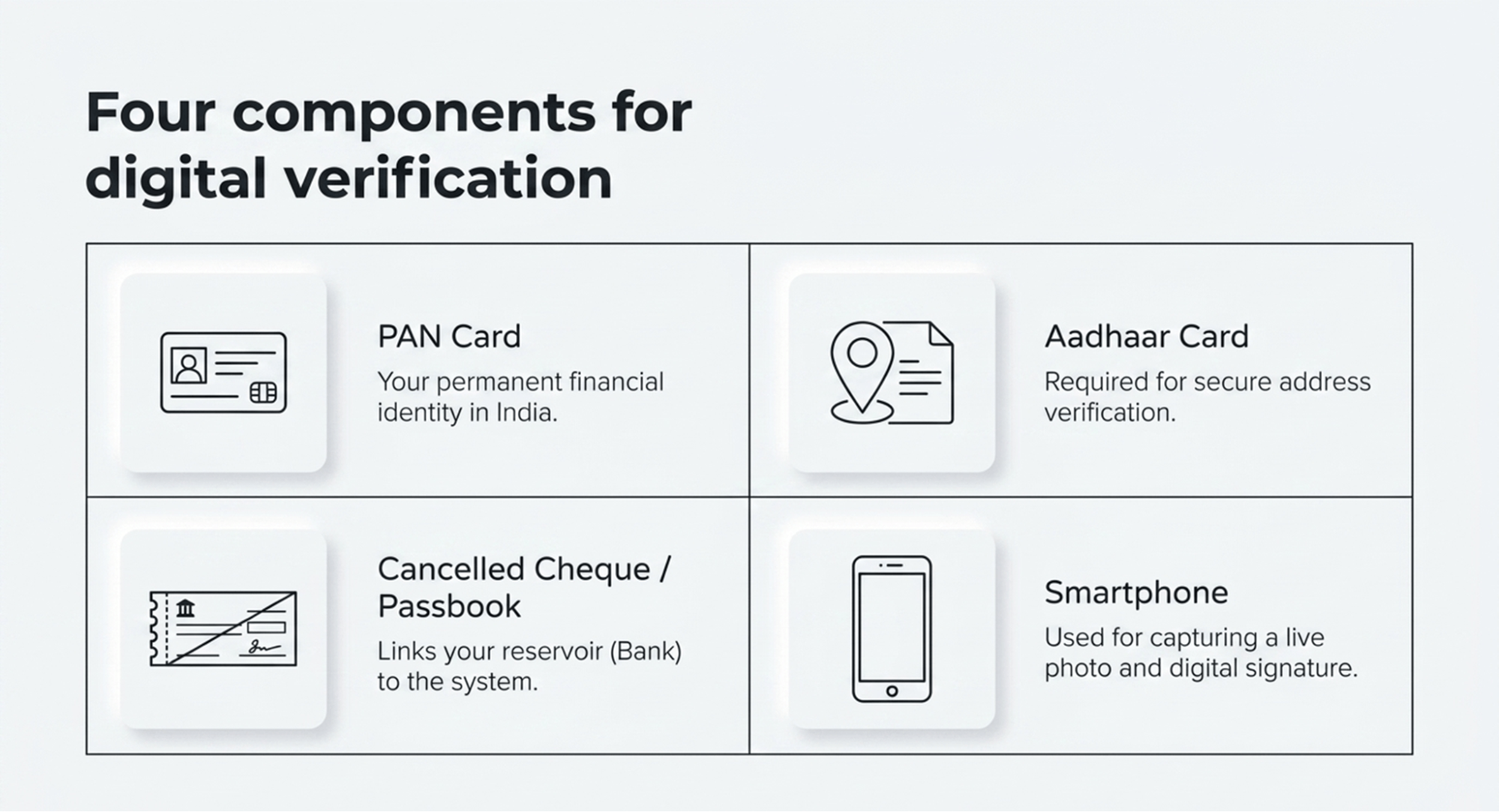

The KYC Process: What You'll Actually Need

Opening these accounts is now almost entirely digital and takes 15–30 minutes on most platforms. You'll need your PAN card (your permanent financial identity in India), your Aadhaar card for address verification, a cancelled cheque or bank passbook copy, and a smartphone for the live photo and signature verification. Most brokers complete verification within 24 hours.

A Special Note for NRIs

If you're an Indian citizen living abroad, you can absolutely invest in Indian equities; and many NRIs do, because India's growth story is compelling. But you need to route your investments through the correct banking pathway.

NRE Account (Non-Resident External): Funded with foreign earnings. Fully repatriable; meaning you can move your money and profits back abroad freely. Most NRI investors prefer this route.

NRO Account (Non-Resident Ordinary): For income earned within India (rent, dividends, etc.). Repatriation has some limits and tax implications.

Your Demat and trading accounts as an NRI will be linked to whichever of these you open. The process involves a few additional documents, but the structure is the same.

Your accounts are live. The pass is in your hand.

But before you spend a single rupee, you need to answer one fundamental question: “What kind of player do you want to be?”

The next Article is about defining your Master Plan.