CPCL Financials - Fractionally Distilling Volatility

In the first part, we left off with how the financials have been volatile for CPCL, and that volatility is not good. Volatility increases risk even if it comes with higher returns.

Is Volatility Really Bad?

Consider a simple example as an INR 100 investment. Let’s say you invest in a penny stock that provides you a return of 25%. However, in the next period, you lose 25% of your value due to the company not performing. What is your effective return for these two periods?

You may think you are at no profit and no loss. But you would be wrong, and so was I. The total return would be:

From INR 100 to INR 125 - A 25% increase

Ethica Invest

Serious about long-term investing?

Unlock our professionally managed portfolios.

And then from INR 125 to INR (125*0.75) = INR 93.75. So you are at a loss.

The reverse scenario of first losing 25% and then having a gain of 25% would also lead to the same investment value of INR 93.75.

Now, if the increase and decrease were smaller, say only 5%. Your investment would be:

INR 100 * (1+0.05) * (1-0.05) = 99.75. Hence, the loss is much less. It shows why volatility is not good. And this is exactly what happens with oil refiners due to changes in the price of crude oil.

Firing up the Furnace

We will deep dive into financials and ratios for CPCL to see if the returns are worth the risk.

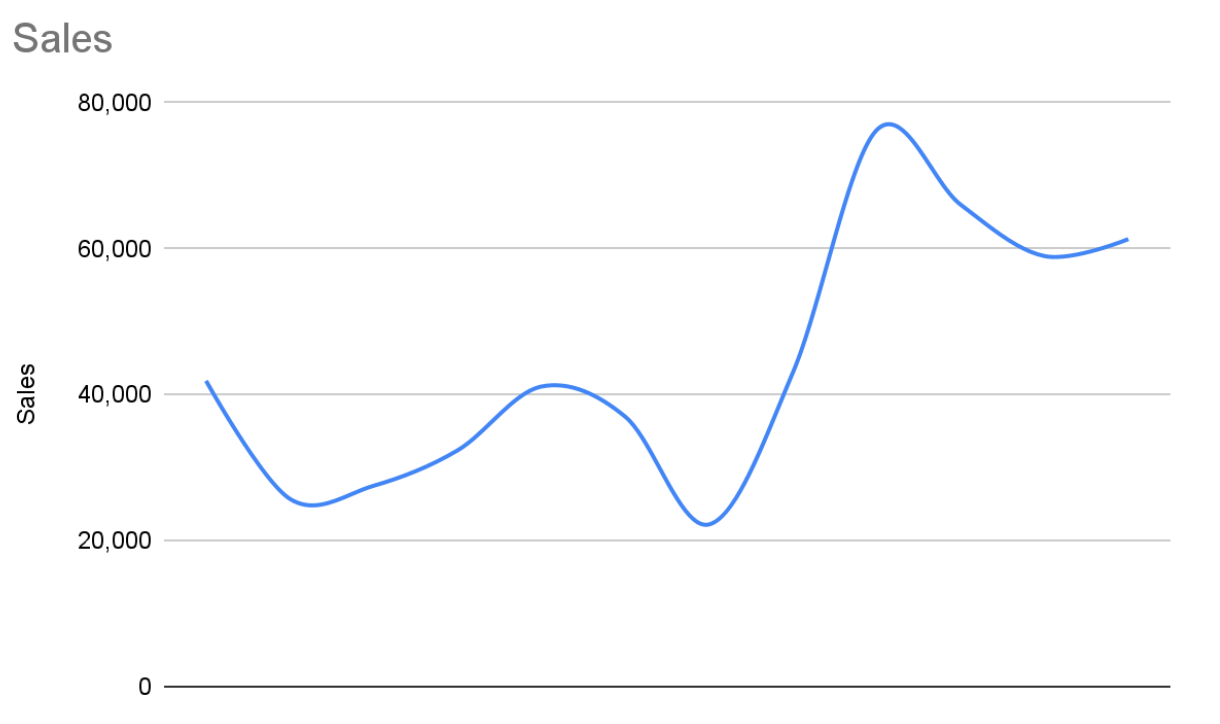

Let’s begin with the annual results, as we are looking at a long-term investment. Sales have been bumpy, but have seen a rising trend, which is something that is positive.

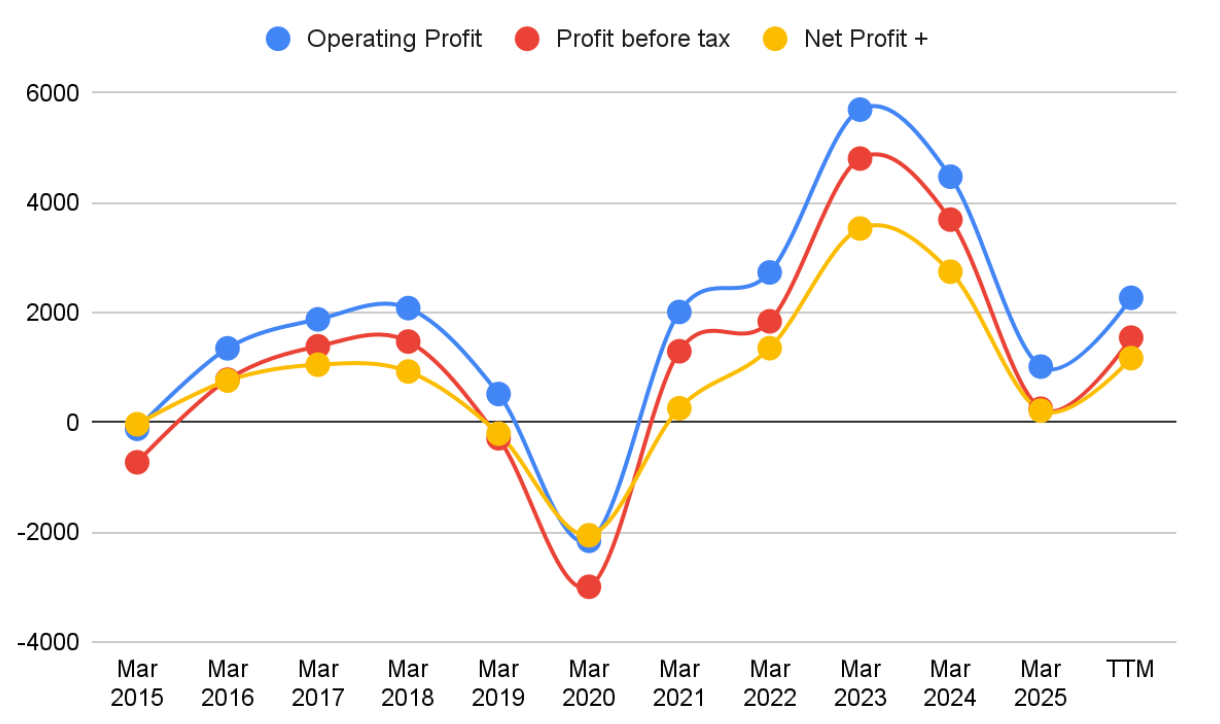

Profit Margins

The income benchmarks mirror each other to a great extent. Profits have been negative in the past, but we need to discount that because it was during the COVID era. Other than that, profits have been generally positive, although volatile.

For the recent periods, the TTM figure is above the latest FY result, which might be an indication that we can have a good FY 26 ahead.

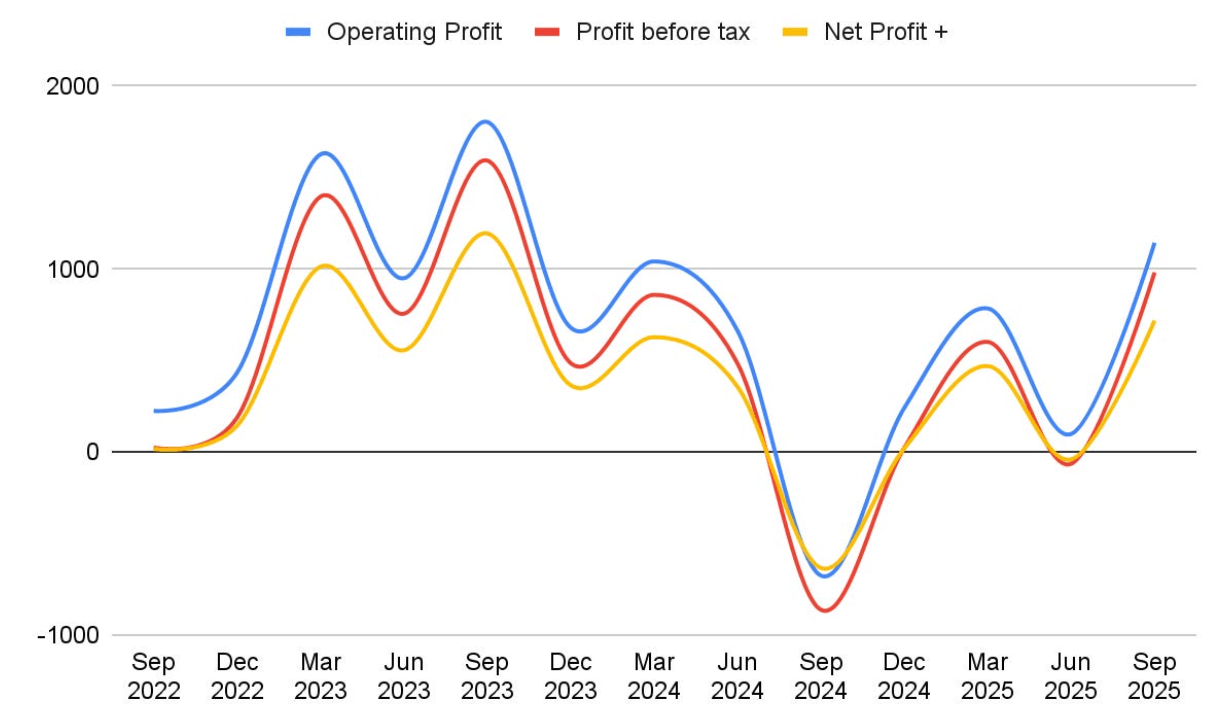

Even the quarterly figures show volatility, and as we saw earlier, FY 2024 and 2025 were not good. The stock price also plummeted. From a high of around INR 1050, the stock fell to less than INR 500. We can see the potential for the stock at that price if profitability rises. While no one can be sure of the pricing of a stock, past valuations can be an indication. We will next look at some ratios and see how they compare to the general industry.

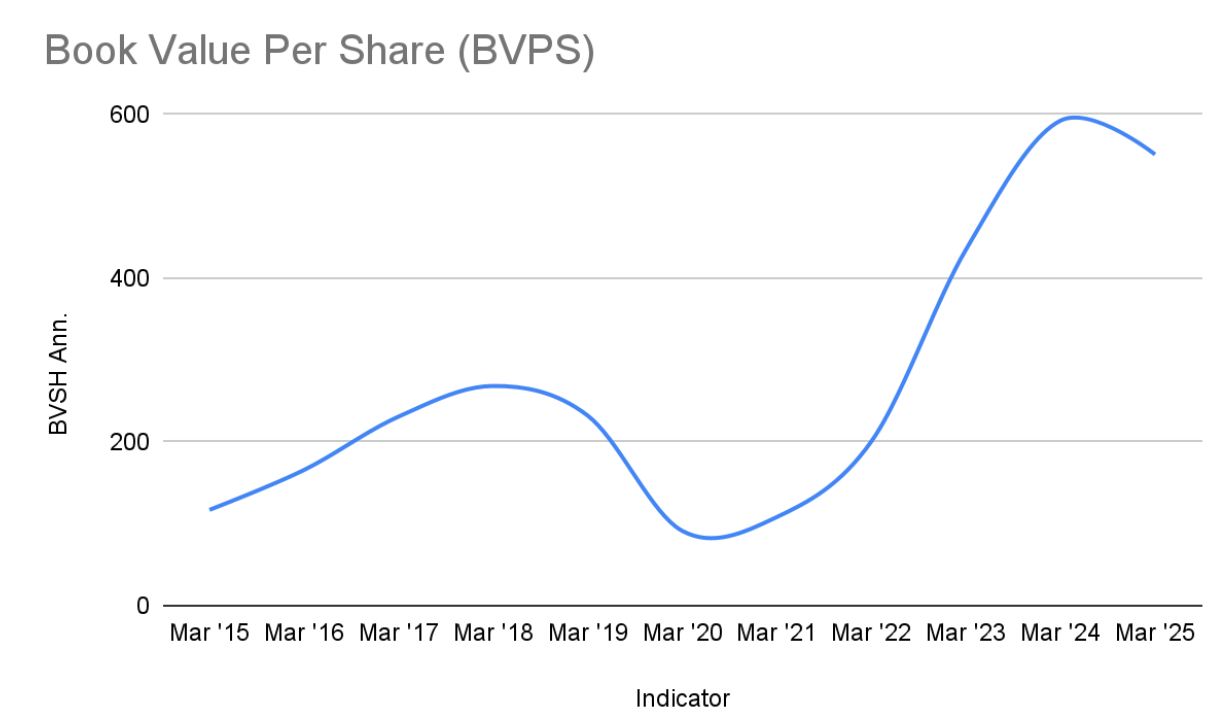

Book Value per share has seen some setbacks but has risen over the past decade. This is a sign that the company is investing in revenue-making assets, generally, Plant and Machinery. The drop in FY 2025 can be attributed to the lower income for the fiscal year. However, things improve, and considering the book value per share to stock price ratio, we can get an indication of the stock price.

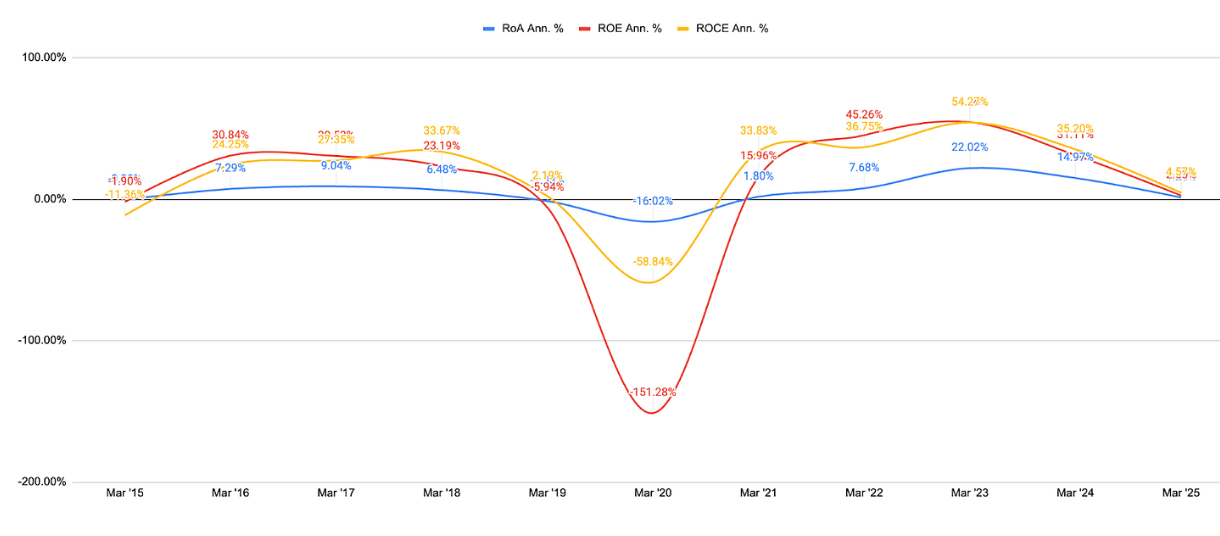

Asset Returns

Returns on assets and capital have been generally good except for the time around COVID. The petrochemical industry has an average ROCE of around 15% which comes with its own set of volatility. The average ROCE for CPCL is around 16.53% with a median of 27.35%. This is above the industry mean, implying that the company is performing slightly better than its peers.

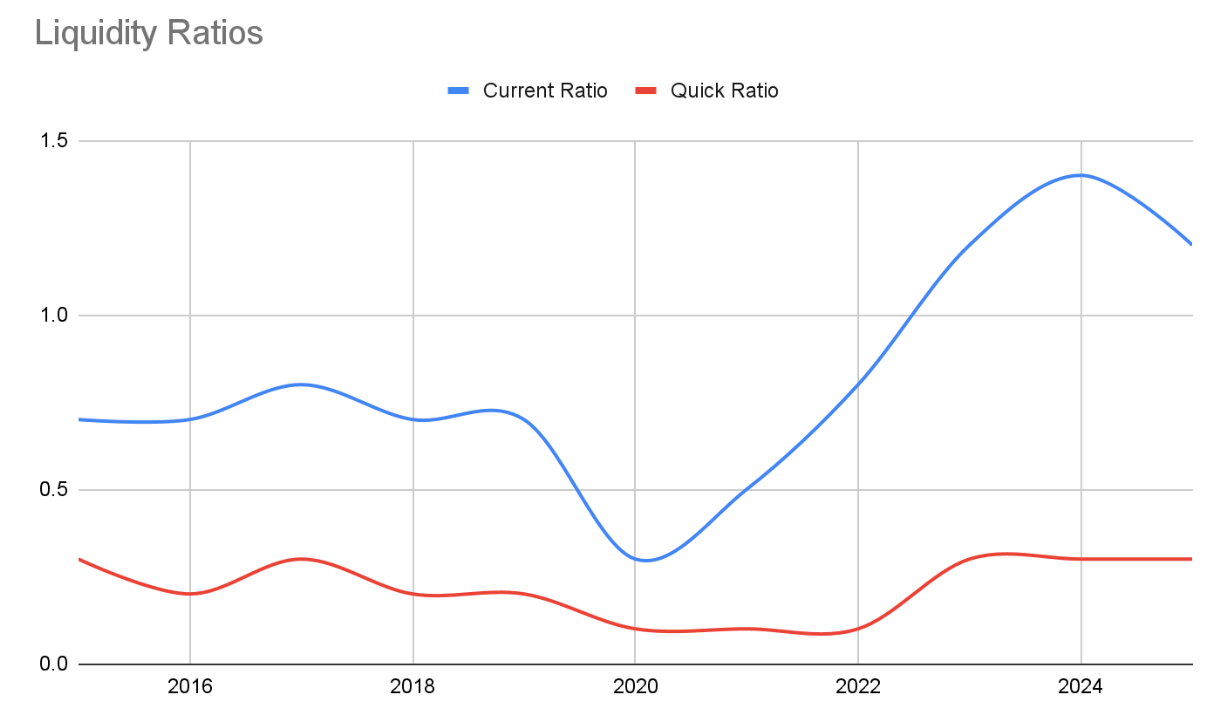

The current ratio seems to improve, especially in the post-COVID era. The quick ratio is stable and has been, more or less, similar over the years. Maintaining a good current ratio is surely a positive sign for a company that sees large variances in the raw material (crude) costs.

Ethica Invest

Serious about long-term investing?

Unlock our professionally managed portfolios.

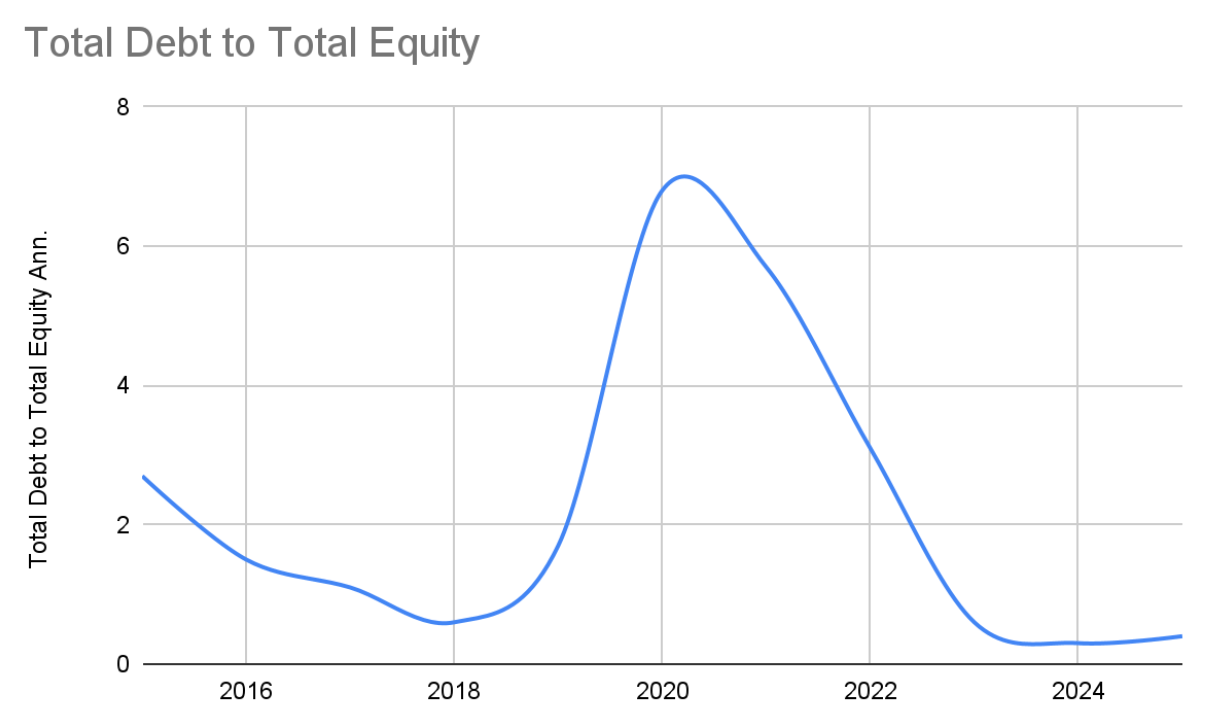

The debt-to-equity ratio has improved, and debt has gone down. This brings stability to the company and implies confidence from managers.

Quarterly Results

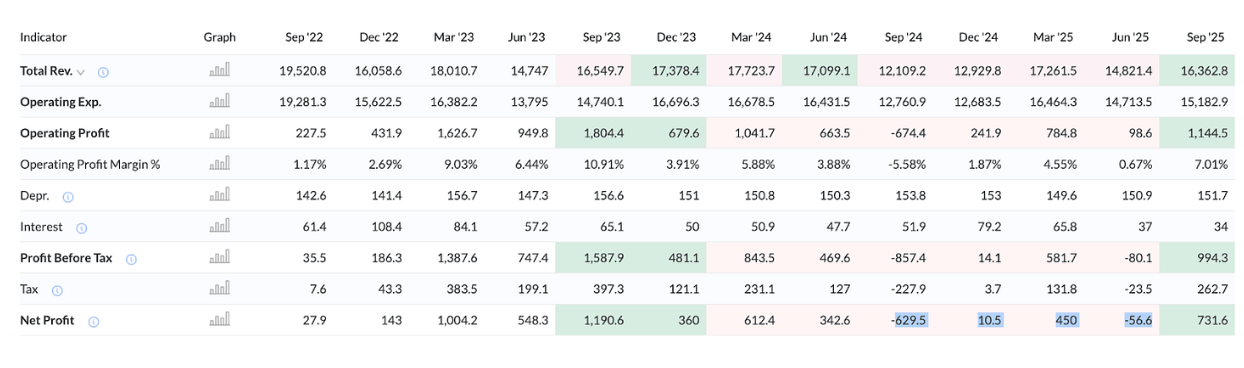

The quarterly results provide a breakdown for the past three years. For the most recent quarter, for which the results were released only a few days back, the company has shown:

- A spectacular QoQ growth of 35.13%.

- Operating margin has improved significantly, too, and is at 7.01% in this quarter.

- A positive net profit of 731.6 crores, a performance that is best in the last 8 quarters.

- TTM Net Profit is 1,135.40 crores, which indicates a revival of profitability.

Some Valuation Measures

We can assess from the previous analysis that the financials of the CPCL are not inducing confidence because:

- Profitability is not positive.

- Volatility is always an issue, and small changes in crude can affect profitability easily.

However, the stock price has seen a significant upswing in the previous month. In addition, there is always the option that the parent IOCL or the government will bail it out in case anything goes wrong. This allays the fear of the company going bust, and investors flock even when there is a small amount of profitability.

The crude price has been mostly below $100 post-COVID. The stock price for CPCL reached its highest ever, INR 1022, in April 2024, which was based on expectations of enhanced profitability due to the purchase of Russian oil.

Oil from Russia reached its then highest in April 2024 of 1.9 barrels per day, and at that time the oil was being discounted up to 20% or somewhere $15-$20 per barrel. This discount has now significantly decreased, and pressure from the USA has led to a decrease in imports. However, during late September, discounts have started increasing again due to market factors.

The recent increase in the price of stock can be attributed to:

- Increase in profitability for the quarter ended June.

- Stable crude oil price and expectations of further fall in prices.

- Russian crude discount rising again.

The average crude price in April 2024 was more than $80, and the crude price today averages about $65, which might indicate that the stock price has a similar or slightly more momentum than April 2024, ceteris paribus. This would indicate a stock price of INR 1,000, which is similar to the recommendation provided by the SEBI Analyst at Ethica.

Enterprise Value

The average EV/EBITDA for refineries in India is around 6 to 9. Using the TTM EBITDA of INR 2,270 crores, we can calculate the average stock price. Assuming an average EBITDA of 7.5.

EV for CPCL = INR 2,270*7.5 crores = 17,025 crores

No of stock outstanding = 14,89,10,000

Price per stock = 170250000000/148910000 = INR 1143

Now, valuation measures cannot account for a lot of factors, and we should always discount them as a safety net. Discounting even by 10% would bring this valuation in the range of INR 1,000 per stock, which is the recommended price per the SEBI analyst. Discounting is needed because:

- CPCL is a small company, and the smaller the company, the greater the risk premium.

- Volatility of the raw material, which is the crude price.

Therefore, the recommendation, as provided by the SEBI Analyst at Ethica, is around INR 1,000. Since the stock is near that level, caution is to be exercised.

The E20 debate

The Bharat Stage 6 norms mandated E20 fuel, which recommends the addition of ethanol in Petrol up to 20% by Volume. Vehicles manufactured in 2023 and after need to work on E20. Fuel pumps in India, including IOCL, have already reached E20 levels and are disbursing a 20% ethanol mix in petrol.

This helps with the profitability of IOCL, as Ethanol comes cheaper when the crude is at a higher price. However, this might result in lower revenue for CPCL as 20% of its sales have decreased. While nearly 55% of its sales come from Diesel and only 14% accounts for Petrol, it can still lead to a loss of revenue of 2%-3%. This further decreases profitability.