Menon Bearings: Micro-Metals, Macro-Margins

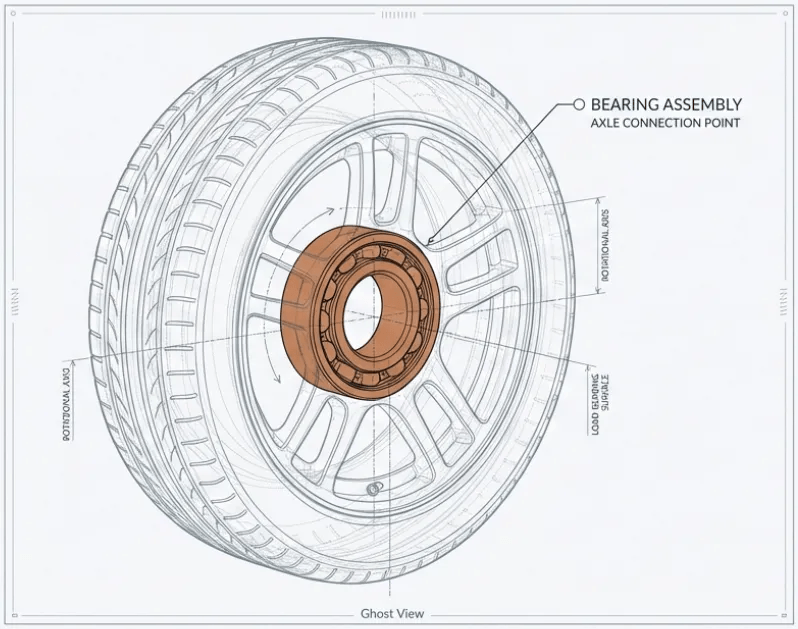

You know that the wheel is one of the greatest inventions of all time.

You use a vehicle with wheels for your daily commute. And while your vehicle stays steady, the wheels spin freely.

So, have you ever wondered what makes that possible?

Well, let me introduce to you; “The Wheel of The Wheel” - ‘Bearing’.

Ethica Invest

Serious about long-term investing?

Unlock our professionally managed portfolios.

This hidden component keeps your vehicle planted on the road while allowing smooth wheel spin.

But here’s the thing: bearings aren’t just for wheels.

They are of different types. And, they power engines, gearboxes, axles, tractors, generators, and industrial machines wherever motion meets heavy loads.

And here’s where things gets interesting.

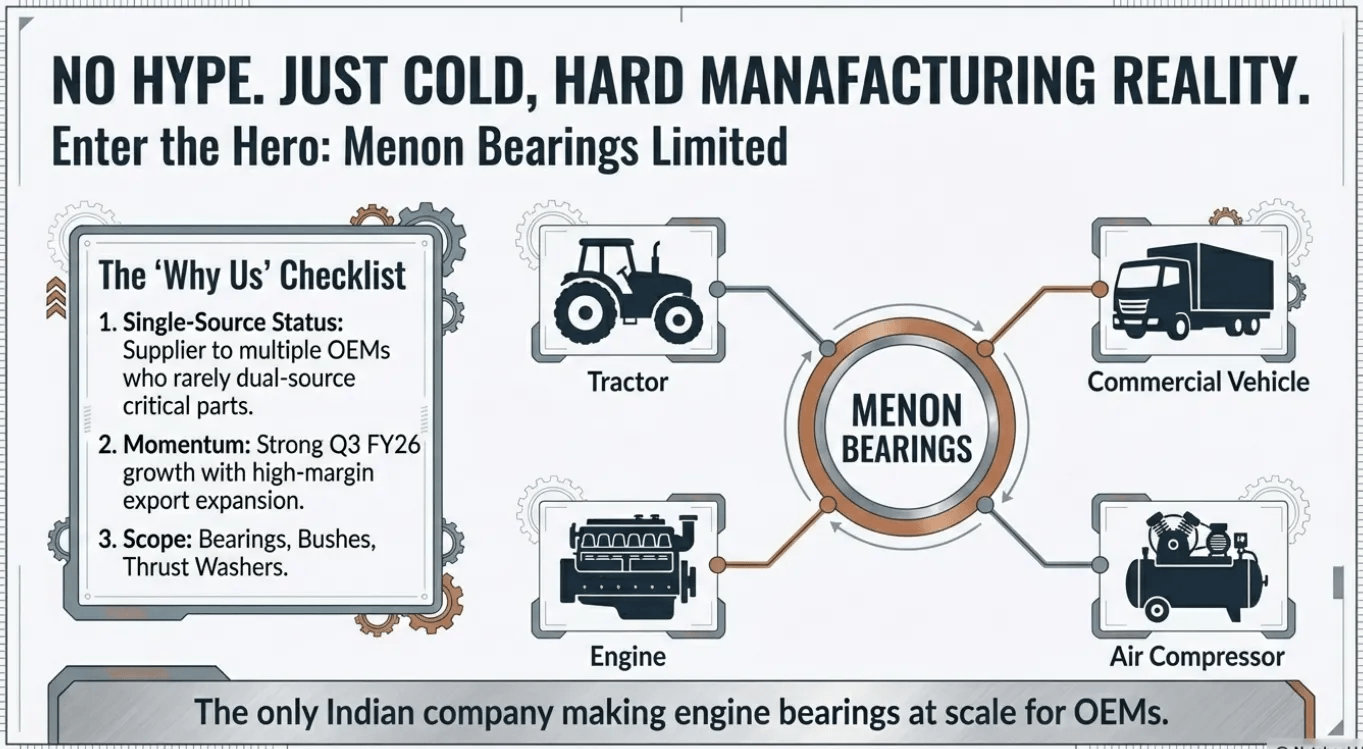

India manufactures millions of engines every year, and there is only one Indian company that makes engine bearings at scale for OEMs.

Menon Bearings Limited

They produce critical engine parts: bearings, bushes, thrust washers; that OEMs rarely dual-source.

Today, this company:

- is a single-source supplier to multiple OEMs,

- has delivered strong growth in Q3 FY26,

- is expanding capacity,

- and is building a high-margin export business.

Intrigued?

Let’s uncover the full story.

Firstly, we will understand the “Auto Components Industry” in which Menon operates.

Now,

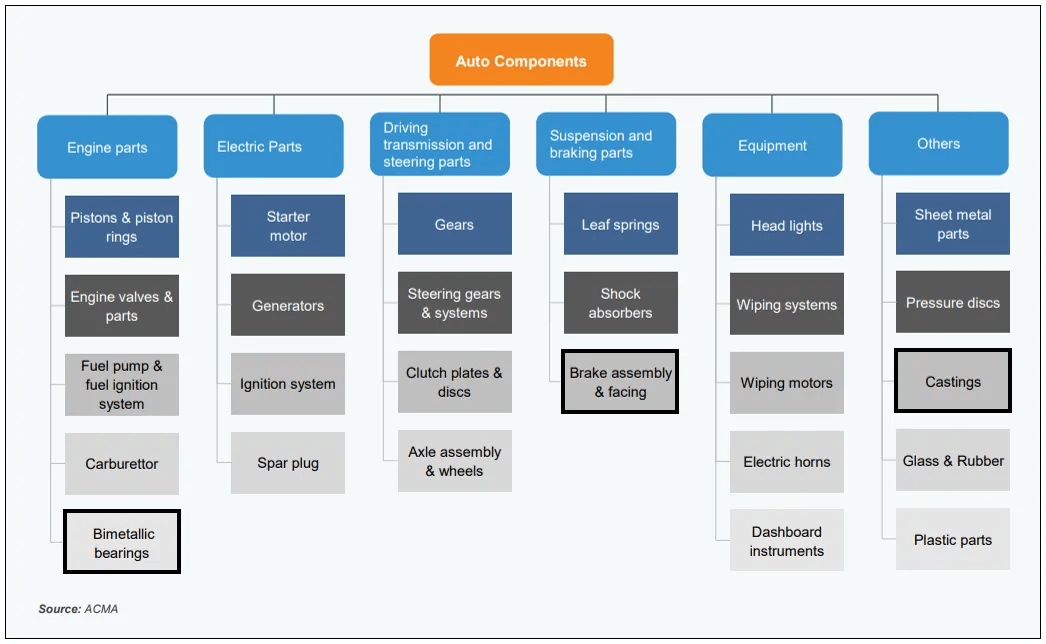

The auto components industry manufactures items like engines parts, brakes, bearings, castings, electronics, and body parts. These components are supplied to vehicle makers (OEMs) and also sold later as replacements in the aftermarket.

Ethica Invest

Serious about long-term investing?

Unlock our professionally managed portfolios.

In simple terms, automobile companies assemble vehicles, while auto component companies make the parts that make vehicles work.

So, let’s have a good look at the Auto Components Industry.

Big Tailwinds: Why Things Look Strong

First, Indians are simply using more vehicles.

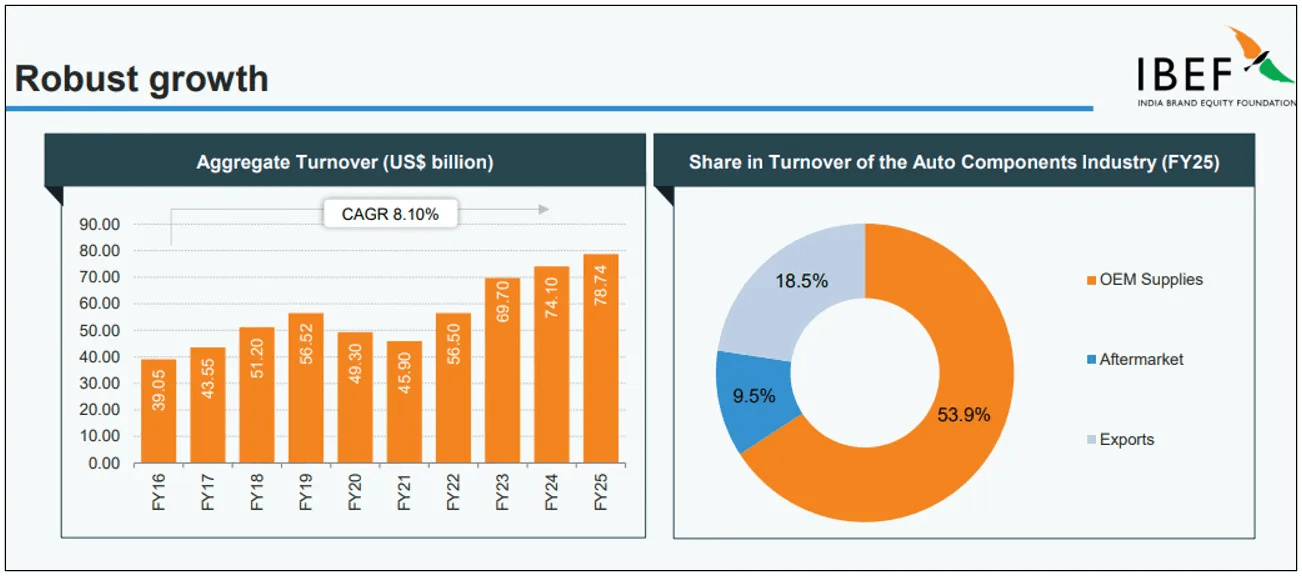

In FY25, India made over 3.1 crore vehicles across cars, two‑wheelers, commercial vehicles and three‑wheelers. And on top of that, the total number of vehicles on the road is expected to jump from about 33 crore to over 43 crore by 2030.

You can see this in the money.

The auto components industry did about Rs 6.73 lakh crore (US$ 78.7 billion) of business in FY25 and has been growing at roughly 14% a year since FY20. About half of this comes from supplying parts to vehicle makers (OEMs), a slice from exports, and a steady 10% from the replacement market.

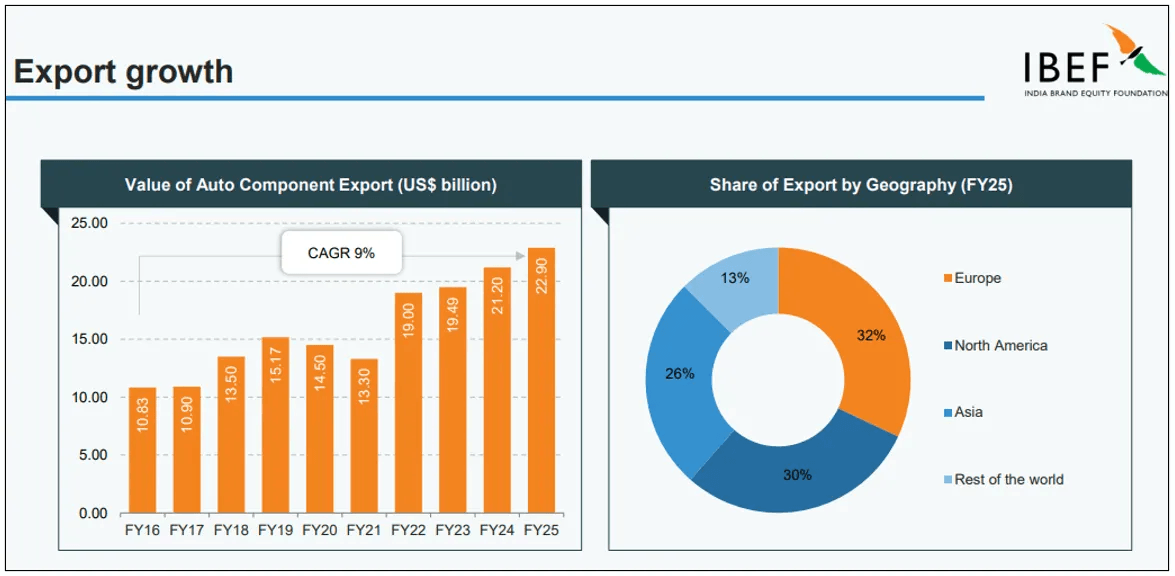

Exports are the second big boost.

More than one‑fourth of all parts made in India now go abroad. Exports grew 8% in FY25 to US$ 22.9 billion, with Europe leading the charge. The industry is openly targeting US$ 100 billion of exports by 2030.

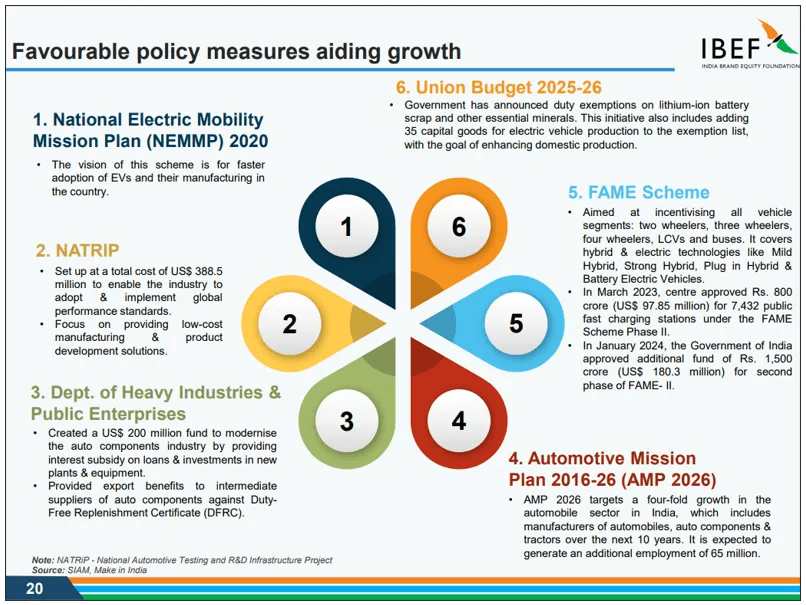

Third, Policy is clearly leaning in this direction.

Beyond PLI and FAME, schemes like NEMMP, AMP 2026, NATRiP, and budget measures such as duty cuts on lithium‑ion battery inputs are all designed to pull more of the value chain into India and push the industry up the technology ladder.

Structural Changes: How the Industry Itself Is Shifting

Now, the shape of the industry is changing too.

Earlier, Indian firms were mostly “local vendors.” Today, the country is turning into a global hub. Big names like Ford, Fiat, Suzuki and GM use India as a base for small engines and parts, and companies like Varroc even supply lighting systems to Tesla.

There’s also a shift in technology.

Companies are putting money into R&D labs, software‑defined vehicles, ADAS (driver‑assist features), and EV‑focused components. Tata Motors, Tata Technologies, NXP, Bridgestone and others are all expanding tech centres in India.

Headwinds: What Can Go Wrong

Global demand is uneven.

Europe, which still takes around 32% of India’s component exports, actually shrank a bit (about 2% decline) in FY25. If global auto sales slow, export‑heavy suppliers feels the pain.

Costs are another headache.

This sector uses a lot of metal, and there is a need for constant modernization and investment to stay cost‑competitive. India still imports roughly Rs 1 trillion (US$ 13.6 billion) of components, which the government wants to halve in 4-5 years.

Competition is also heating up.

Global Tier-1 suppliers are scaling up in India, and Chinese players like BYD, which targets 40% of the Indian EV market by 2030, are raising the bar on both price and technology. Smaller Indian firms without scale, R&D strength or strong OEM relationships will struggle to protect margins.

The story so far is about “where the industry is going”, now the next question is:

What exactly are we making inside this ecosystem? This is where product segments comes in.

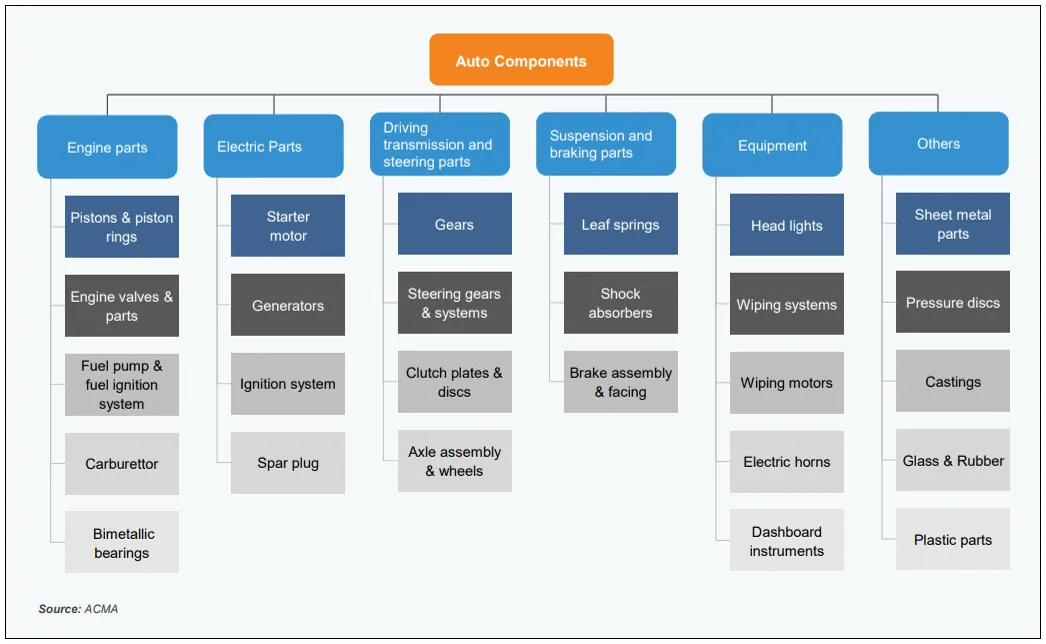

Product Segments

- First, you have engine parts. These help the engine breathe, burn fuel and handle heat.

- Then come electric parts. These bring the vehicle to life. As vehicles go more electronic and electric, this bucket keeps getting bigger.

- Next are driving, transmission and steering parts. These send power to the wheels and help you turn; gears, steering systems, clutches and axles with wheels.

- You also have suspension and braking parts. These keep the ride stable and help you stop safely; leaf springs, shock absorbers and brake assemblies.

- On top of that sit equipment parts. The things you actually see and use: headlights, wipers and wiper motors, horns and dashboard instruments.

- Lastly, there’s an “others” group: They may look basic but they form the body, structure and finishing touches.

Together, these buckets cover everything from the heart of the engine to the lights, panels and plastics you notice on the outside.

Now, you might think; where does Menon operates in this? Let me help you out.

The highlighted boxes is where Menon operates:

- Bi‑metal bearings,

- Alkop (aluminium castings), and

- Brakes.

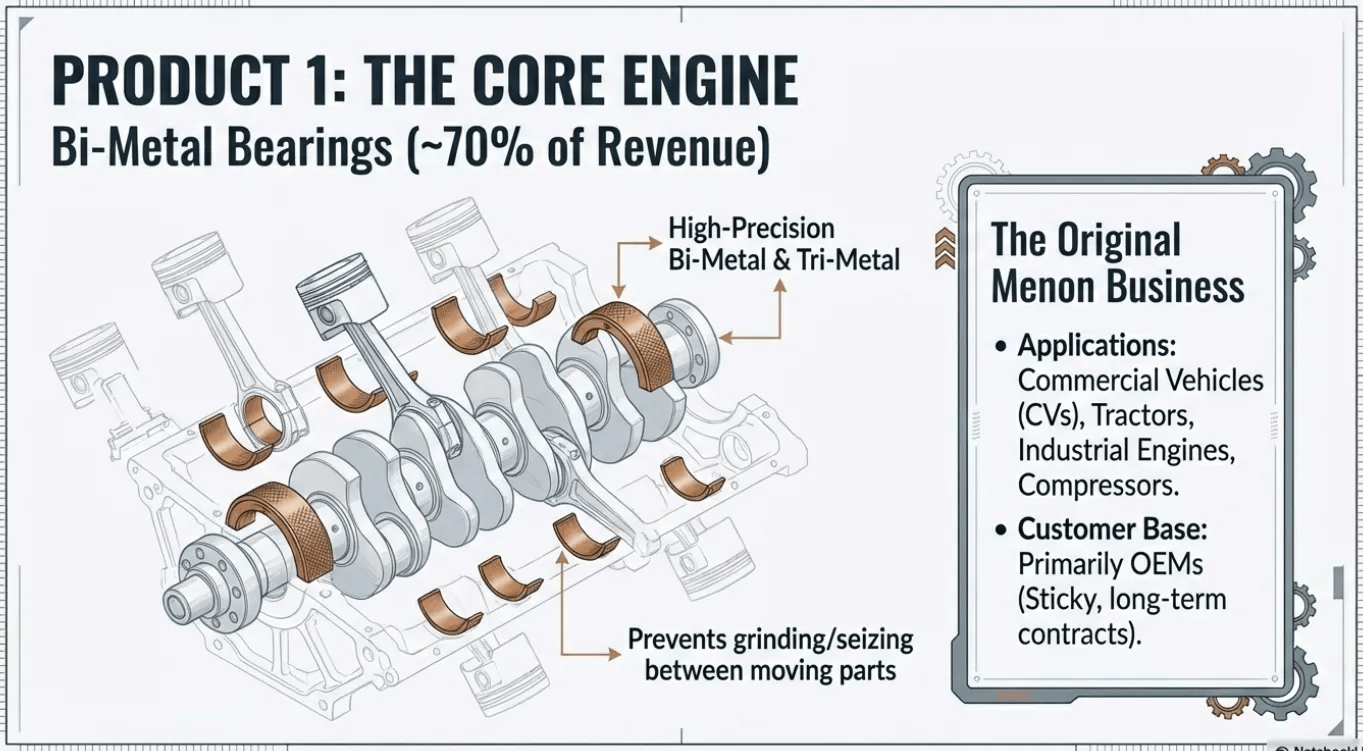

1. Bi‑metal bearings – the core cash engine

This is the “original Menon” business.

Here they make engine bearings, bushes and thrust washers; the thin metal layers that sit between moving engine parts so nothing grinds or seizes.

These are high‑precision, bi‑metal and tri‑metal parts used in CVs, tractors, industrial engines and compressors, mostly for OEM customers. This division contributes roughly 70% of total revenue, making it the main profit driver.

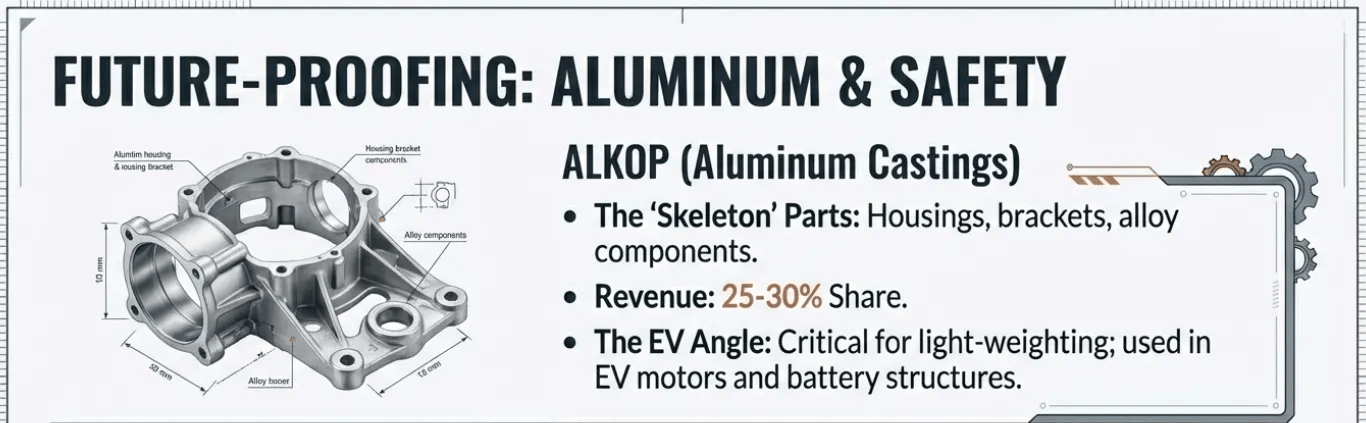

2. Alkop – aluminium castings

Alkop is Menon’s aluminium die‑casting vertical.

Think of it as the “skeleton parts” around the engine and drivetrain; housings, brackets and other alloy components that need to be light but strong.

This business rides the same OEM relationships but is more EV and light‑weighting‑friendly, because aluminium castings are used in EV motors, battery structures and power‑electronics enclosures. Alkop accounts for about 25–30% of revenue, and management is guiding for strong growth here over the next few years.

3. Brakes – the new growth option

The youngest leg is the brakes division.

Menon makes asbestos‑free brake linings, shoes and pads for commercial vehicles; basically the stuff that helps a loaded truck actually stop.

This segment is still small; only a single‑digit share of revenue today; but it is scaling up as new OEM approvals come through. The company positions it as an eco‑friendly, OE‑grade niche rather than a cheap aftermarket play.

Menon Bearings today is not “just a bearing maker.”

It is running three tightly linked but distinct businesses, each with its own role in the auto components value chain.

So, is it the same from the start? No.

To understand this. Let’s have a look in the history.

History

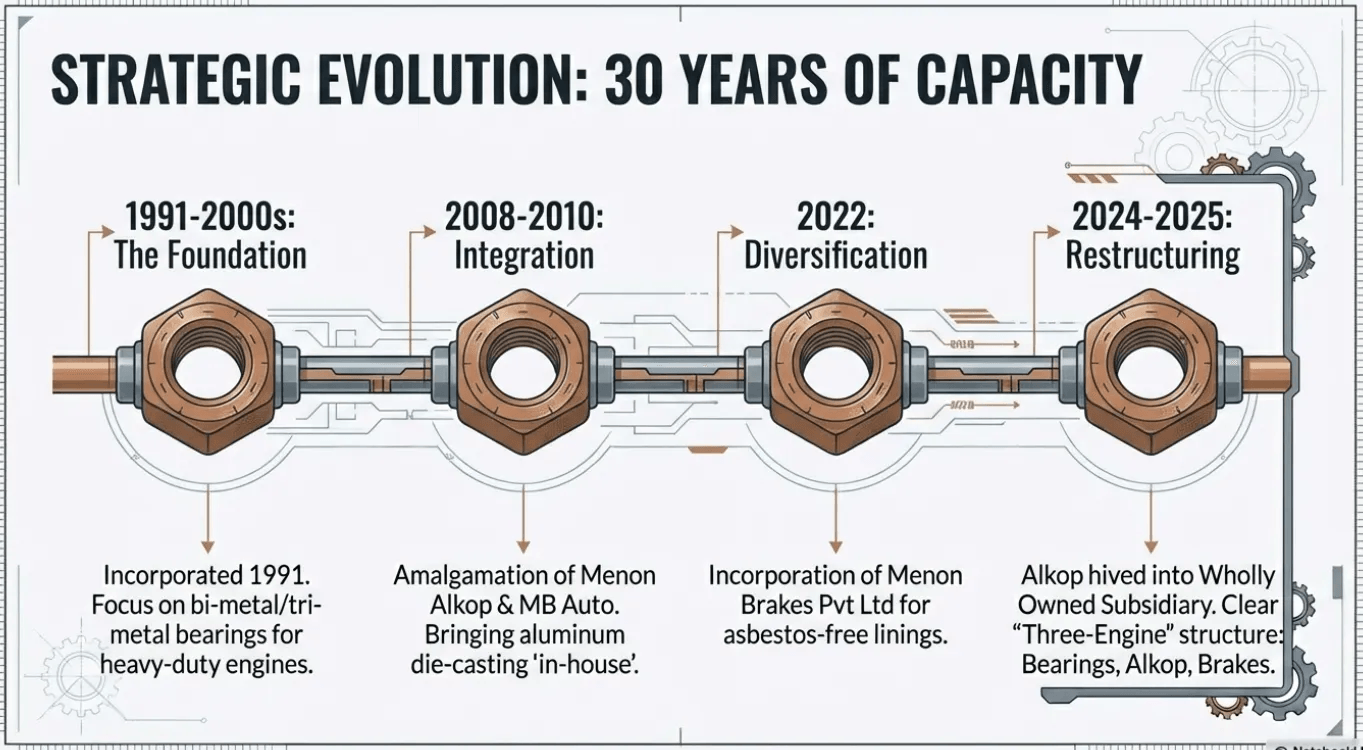

1990s–2000s – Building the bearings franchise

Menon Bearings Ltd is incorporated as a public limited company on 4 July 1991, promoted by Menon Pistons and the Menon family.

Through the late 1990s and early 2000s, Menon focuses on bimetal/tri‑metal engine bearings and bushes for heavy‑duty diesel engines, multi‑axle CVs and tractors, adding a second bearings plant as volumes grow.

2000s – Stepping into aluminium castings (Alkop roots)

To tap light‑weight engine and transmission parts, Menon creates Menon Alkop Pvt Ltd and M B Auto components Pvt Ltd as wholly owned subsidiaries for aluminium die‑casting. These entities supply fully‑machined aluminium alloy components to automotive and industrial customers.

2009 – Alkop businesses folded into the parent

The Bombay High Court approves a scheme of amalgamation of Menon Alkop Pvt Ltd and M B Auto components Pvt Ltd with Menon Bearings, effective 1 October 2008. This brings aluminium die‑casting formally inside the listed company, creating a second business leg.

2010s – Consolidation as a two‑engine player

Through the 2010s, Menon runs two tightly linked businesses:

- Bimetal bearings/bushes/thrust washers

- Aluminium die‑castings (Alkop)

The company deepens OEM relationships in CVs, tractors and industrial engines, and exports start scaling.

2022 – Brakes arm incorporated

Menon Brakes Private Limited is incorporated in 2022 as a wholly owned subsidiary to make asbestos‑free brake linings, pads and riveted brake shoes for LCVs and HCVs. This marks Menon’s formal entry into braking systems.

2024 – Alkop hived into a new WOS

To sharpen focus, Menon incorporated Menon Alkop Limited on 23 January 2024 as a new wholly owned subsidiary and sells its Aluminium Division to this entity on a slump‑sale basis, after shareholder approval in April 2024. Aluminium die‑casting becomes a distinct but fully controlled vertical again.

“So, where does MBL stands today?”

2025 – Three‑engine structure in place

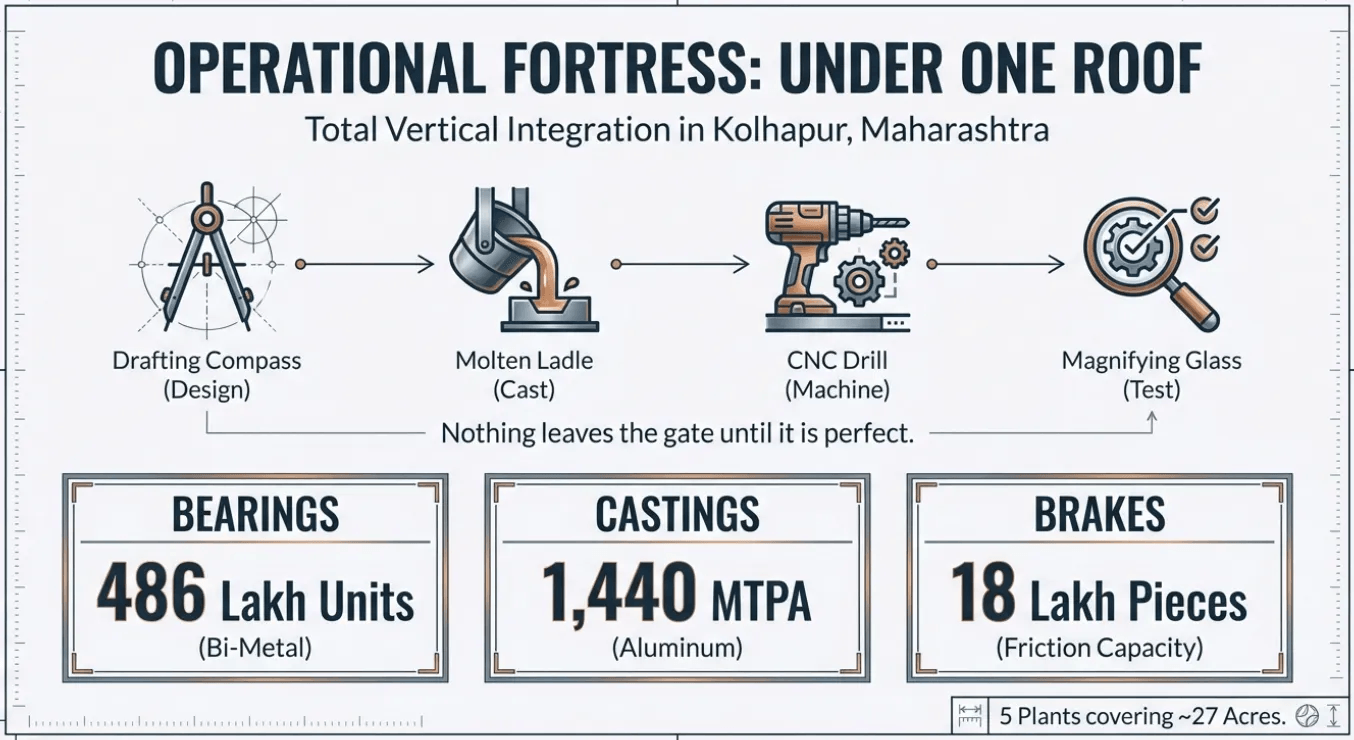

The company runs about five plants in and around Kolhapur, Maharashtra, spread over roughly 26–27 acres.

And, in FY25 Menon Bearings Limited was operating:

- 486 lakh units of bi‑metal bearing capacity,

- 1,440 MTPA of aluminium‑casting capacity, and

- 18 lakh pieces of brake‑friction capacity.

These are fully integrated facilities where Menon designs tools, casts or forms the metal, machines it in‑house, finishes it, and tests it before it ever leaves the gate. That “under one roof” approach is a big reason OEMs trust them with critical engine and brake parts.

On the demand side,

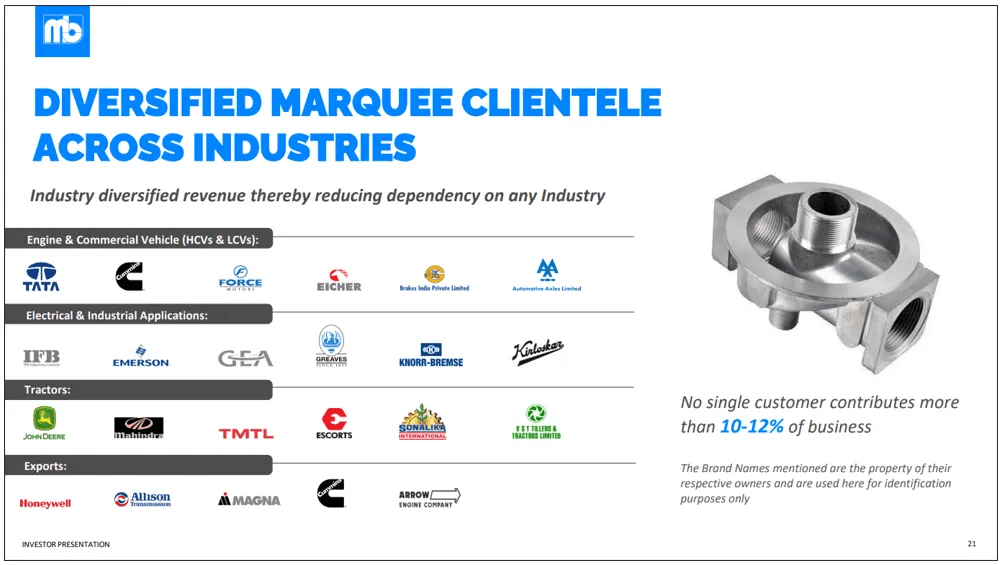

Menon is plugged into serious names. Across engines, tractors and CVs, it supplies to marquee OEMs in India and abroad.

That business is complemented by a deep reach in the replacement market:

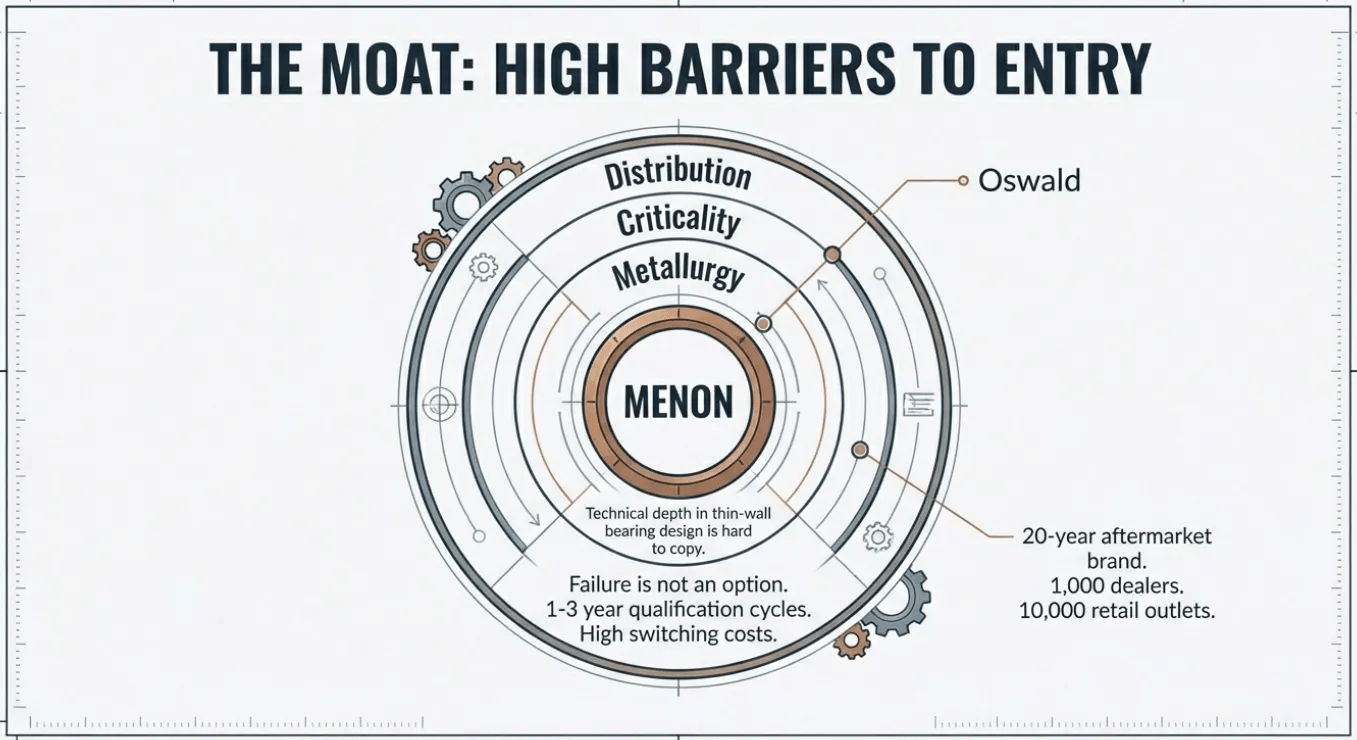

A 20‑year built brand in the aftermarket, a network of ~1,000 dealers and distributors, presence in 10,000+ retail outlets, and relationships with over 30,000 mechanics and re‑borers across India.

In plain English: when a fleet owner or local garage needs a premium bearing or bush, Menon is a known name on the shelf.

If you’ve stayed with the Menon story till here, the next thought now is: “Okay, but what’s ahead?”

“Does Menon Bearings have the advantages and growth drivers to grow?”

And just as important; “what could slow them down?”

Thesis: Why Menon Bearings works as a business

Moats

Narrow niche, high expertise

Menon is in a narrow lane: engine bearings/bushes, heavy‑duty industrial applications, aluminium castings and CV brake linings.

This focus shows up in two ways.

One, the technical depth in metallurgy and thin‑wall bearing design is hard to copy.

Two, Menon’s sales engine is not spread thin; it is aimed at a known set of OEMs and platforms.

This tight niche positioning of Menon is a competitive advantage.

Deeply embedded in critical applications

Now, because this niche is specialised, there simply aren’t many serious players. And the parts that Menon supplies sit inside engines, axles and braking systems for CVs, tractors, industrial engines and gensets; are places where for OEMs failure is intolerant.

For an OEM, qualifying a new supplier here is a 1–3 years testing, field trials and audits. Once Menon is “designed in” on a platform, the buyer has very little incentive to switch to another vendor. That long qualification cycle, combined with a small pool of capable competitors in this niche, is what gives Menon its moat.

Growth Drivers

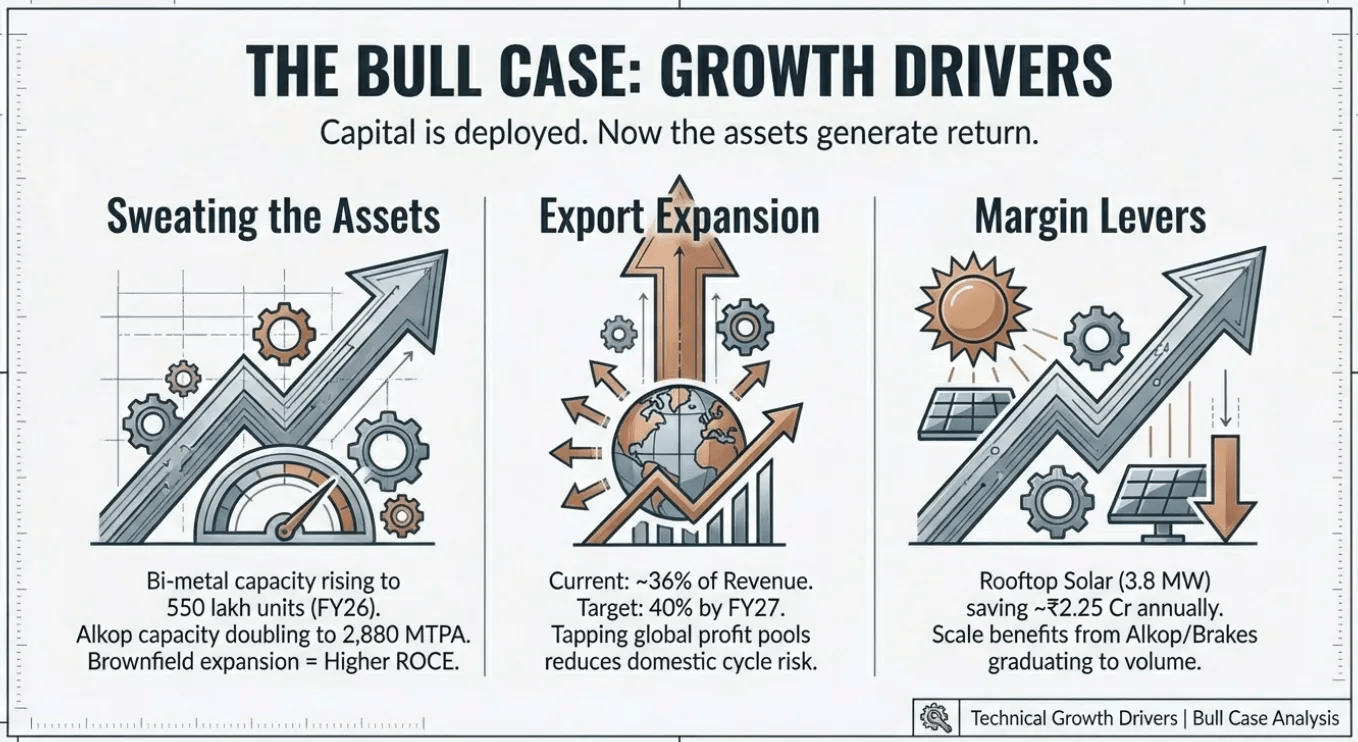

Capacity is already built; now it has to sweat

Menon has quietly done the heavy lifting on capex.

Its Bi‑metal capacity is stepping up from 486 lakh units in FY25 to 550 lakh units in FY26, Alkop is planned to be doubled from 1,440 to 2,880 MTPA over the next two years, and brakes moving from 18 lakh to 24 lakh pieces by FY27.

Most of this is brownfield and debottlenecking, not grand new plants. And so, even mid‑teens volume growth can translate into faster profit growth because the fixed cost base is already in place.

Exports shifting from “nice add‑on” to core engine

The second big driver is exports. They’re already more than 36% of revenue, and management is openly talking about taking that closer to 40% by FY27.

The growth levers are quite specific:

- bigger, higher‑value bearings on new global engine platforms,

- the US aftermarket,

- and new beachheads in Africa and other emerging markets.

Why does this matter?

Because it reduces Menon’s dependence on the India CV/tractor cycle and usually carries better pricing power and margins. You’re basically using a Kolhapur cost structure to tap global profit pools.

Margin levers: mix, scale and cheaper power

In Q3 FY26, EBITDA margins bounced back above 20%, helped by a richer mix (more premium bearings and Alkop work), better utilisation across plants, and the ability to pass on raw‑material inflation to customers.

There’s also a structural angle: rooftop solar of 3.8 MW that shave roughly ₹2.25 crore off annual power costs once fully ramped. Put together, if volumes grow even modestly from here, a disproportionately large part of that shows up in operating profit rather than being eaten by fixed costs.

Alkop and Brakes are graduating

Alkop is being re‑tooled to chase high‑volume, high‑value castings, with management itself talking about building a ₹50-60 crore annual business in the next couple of years.

Brakes, though still small, is no longer a side project. The company is putting in a full dynamometer, adding presses and explicitly targeting export and rail/OEM approvals. If this business scales, it stops diluting margins and starts adding to them.

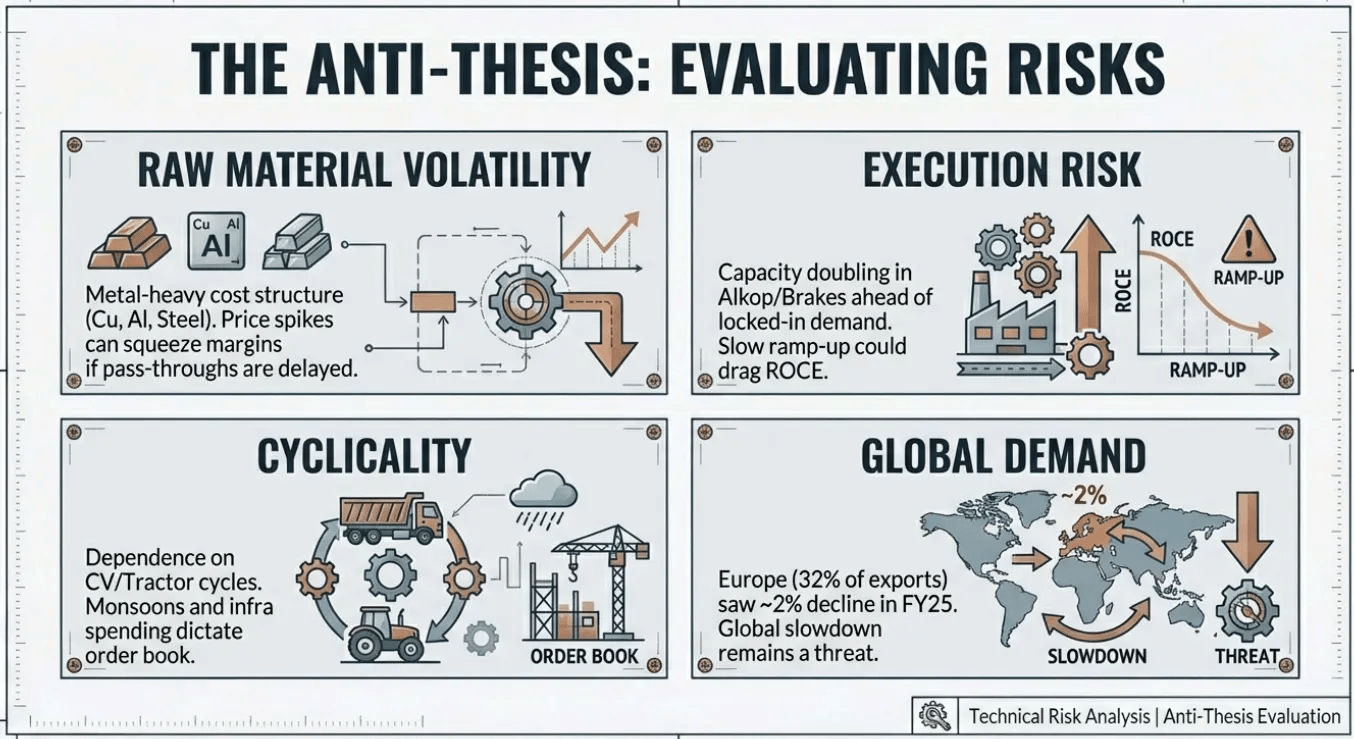

Anti‑thesis: What can hurt this story

Raw‑material swings and OEM bargaining power

This is still a metal‑heavy business. Copper, steel and aluminium price spikes can squeeze gross margins if OEMs push back on price hikes or if pass‑throughs are delayed. The Q3 FY26 recovery shows Menon can handle cycles, but investors should assume margin volatility is there, especially when newer divisions are not yet at optimal utilisation.

Execution risk in Alkop and Brakes

Capacity is being doubled or expanded ahead of fully locked‑in demand in Alkop and Brakes. If the expected ₹50-60 crore Alkop ramp or brake export orders are slower than planned, those plants can drag on overall ROCE.

The brakes business, in particular, operates in a crowded field with players who have long aftermarket and OEM relationships. Winning here will require time, brand‑building and more working capital than in a pure bearings play.

Cyclicality and macro shocks

Menon is tied to CVs, tractors, industrial engines and exports. A down‑cycle in any of these; say, weak infra spends, poor monsoons hitting tractor sales, or a global slowdown; will hit order books. The company is diversifying, but it’s still small enough that one bad macro year will show up sharply in earnings.

Till now, we looked at the complete narrative.

Now, let us look at the numbers, and see whether the narrative is actually backed by the numbers or not?

Financials

As in the products section, we have already looked from where the money comes in.

So, let us now look at: Where the money goes – cost lines that matter

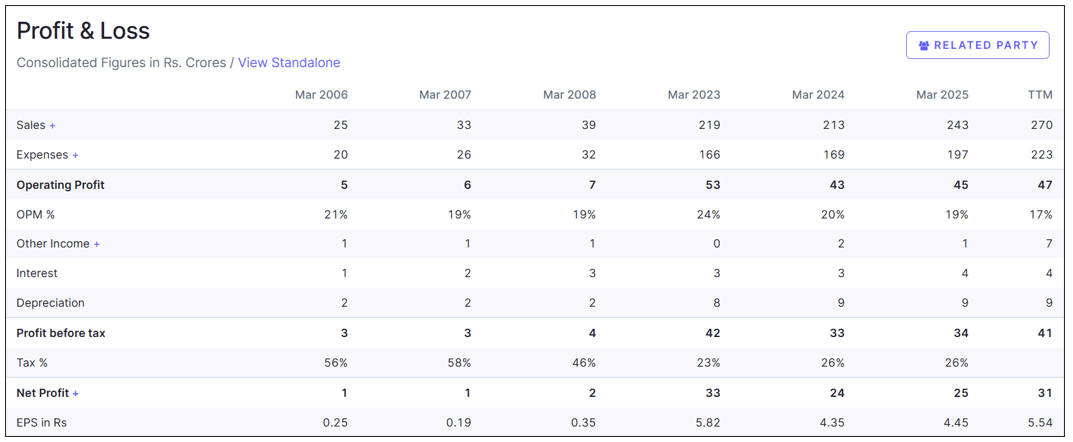

On the cost side, three line items dominate:

- Raw materials – steel, copper, aluminium and friction materials. In FY25, “cost of material consumed” plus purchases of stock‑in‑trade were the largest expense block by far. This is where commodity swings show up.

- Employee costs – factory and technical talent in Kolhapur. These are meaningful but relatively stable as a percentage of sales.

- Other operating expenses – power, fuel, repairs, logistics and overheads. Management has highlighted higher OpEx as a reason margins dipped temporarily in FY26 before recovering.

Valuation – how to think about the price tag

On valuation,

Menon currently sits in that middle but interesting zone. It isn’t a throwaway bargain, and it isn’t priced for perfection either. The trailing 12‑month P/E stands at about 20x, which indicates that the market already sees it as a decent quality compounder, but not yet as a “can‑do‑no‑wrong” story.

Management, however, is guiding to a much bigger earnings base ahead. On recent calls, they’ve spoken about:

- FY26 revenue around ₹285–290 crore and 18–20% growth the following year;

- sustaining EBITDA margins in the 19–20% range, with a target of 20%+ from FY27;

- doing this largely on existing capex, without major new spends until at least 2027–28.

What does that mean?

You shouldn’t buy Menon hoping for a “re‑rating miracle” alone.

The more sensible way to look at it is: if the company actually delivers mid‑teens to high‑teens revenue growth, near‑20% margins and doesn’t dilute returns with fresh capex, then the price appreciation will come from earnings compounding rather than multiple re-rating.

General Disclaimer and Release: Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument.