Netweb Technologies - SuperComps, Assemble!

The turn of the millennium was a good time, with the effects of liberalisation of the Indian economy starting to bear fruit. With growth starting to pick up, consumption also built up. Personal computers were both a fad and a necessity. You needed it for your office work as well as your education.

If you recall, computers were “made” by sourcing different parts, such as a monitor, hard disk, motherboard, processor, etc. and were assembled according to your needs. So you could have your hard disk, RAM, monitor, CD drive, and other features as per your requirements. Personally, I just went with how the salesperson guided me. At the end, what you got was an “assembled computer.” It helped me with coding (programming was used then), but then that was not the reason why I pestered my parents. You know better (hint: gaming 🙂).

Anyways, as hardware was completed, the salesperson or the technical guy would load up pirated Windows and some other needed software, such as Adobe Reader. And then the computer was ready to go to its final destination, where it will be used solely for coding (Not really!).

Netweb Technologies - Assembler for Businesses

Netweb Technologies does something similar and also something different. Not for mere mortals like me, but for large companies and institutions. It develops and manufactures supercomputers, from initial design to final deployment, including software. This is known as High-end Computing Solutions (HCS). NetWeb works in three major segments and other minor segments.

Ethica Invest

Serious about long-term investing?

Unlock our professionally managed portfolios.

These segments include both software and hardware features. Thus, the company provides “engine rooms” for modern technology in several key ways:

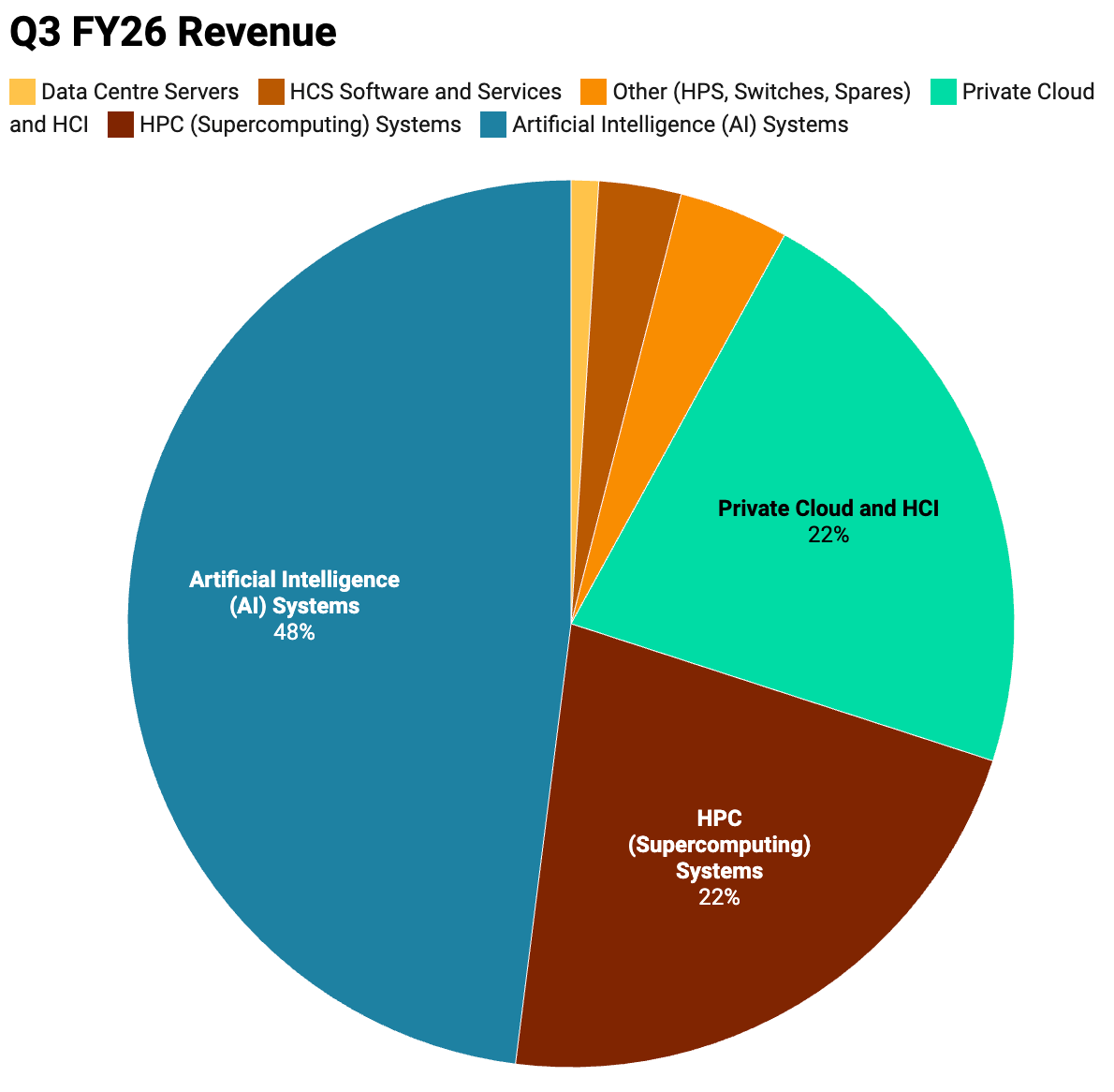

Supercomputing (22%)

They build high-speed supercomputers used for complex tasks, including weather forecasting, space research (ISRO), and Defence.

Artificial Intelligence (AI) Systems (48%)

They create the specialised machines (AI Training Servers/Clusters: Machines packed with multiple high-end GPUs) needed to train and run Artificial Intelligence. It helps companies and institutions build their own in-house AI system or “Sovereign AI.” The company is also helping build AI systems for governmental bodies in India by providing supercomputers based on NVIDIA’s chips.

The real magic isn’t just selling powerful computers, it’s the software that makes them work smarter. Their Skylus.ai is like a smart sharing system for expensive AI chips. Imagine buying one $30,000 NVIDIA chip that normally sits mostly idle while one person uses it. Skylus splits that chip so 7-8 people can use it at the same time, like turning a single-family home into an efficiently shared co-working space. This saves customers money and makes them dependent on Netweb’s platform. Kubyts is like an app store for AI researchers, instead of spending days installing complicated software, they click a button and instantly get a ready-to-use AI development environment.

Pay-As-You-Go for Universities: Netweb also runs a rental model for universities and research labs. Instead of spending millions upfront to buy a supercomputer (which most can’t afford), institutions can rent access to Netweb’s complete AI setup: hardware, software, and support included. Students and researchers get cutting-edge computing power without the university needing to own, maintain, or worry about the infrastructure. It’s like Netflix for supercomputers.

Private Clouds (22%)

For companies that want their own private “internet” for storing data securely, rather than renting cloud space from Google or Amazon. Netweb builds these Private Clouds so businesses can keep their information strictly on their own premises.

Brief History

Founded in 1999, Netweb Technologies has spent over two decades building a reputation as India’s premier High-Performance Computing (HPC) specialist. The company’s journey is characterized by a gradual climb up the value chain: from simple server assembly to complex supercomputer design and now, to AI infrastructure manufacturing.

The Evolutionary Arc

- Phase 1 (1999–2010): The Formative Years: Netweb began as a system integrator, focusing on assembling white-box servers and storage solutions. The company established its Tyrone brand, which became synonymous with cost-effective, customised enterprise computing in India.

- Phase 2 (2011–2020): The Supercomputing Era: The company pivoted towards high-complexity HPC solutions. A defining milestone was the deployment of Param Yuva II, one of India’s fastest supercomputers at the time. This phase cemented Netweb’s relationship with government research bodies like C-DAC (Centre for Development of Advanced Computing) and IITs.

- Phase 3 (2021–Present): The AI & Manufacturing Pivot: Recognising the impending AI boom and the government’s PLI (Production Linked Incentive) schemes, Netweb invested heavily in manufacturing depth. The inauguration of its high-end SMT (Surface Mount Technology Line) facility in Faridabad marked its transition to a true OEM. The IPO in July 2023 provided the capital war chest needed to scale operations and secure large inventory positions required for the AI era.

The company today stands at the confluence of three secular mega-trends redefining the Indian economic landscape:

- Localisation of high-value electronics manufacturing (Make in India),

- Rapid proliferation of Generative Artificial Intelligence (GenAI),

- The geopolitical imperative for Sovereign AI infrastructure.

Competitive Advantage(s)

Now, you might think that any company can source processor chips, hardware, and software from different vendors and combine them to make supercomputers or AI Systems. But this is not as easy as it seems. Integrating different pieces of hardware and software for efficiency is hard. And AI systems need high efficiency and computing power.

So, what Netweb does is that it handles most of the tasks itself, rather than relying on outside vendors. Having SMT lines capable of handling complex server motherboards means Netweb can manufacture the actual circuit boards that go into their AI servers and supercomputers in-house, rather than outsourcing this critical step. The only major thing it sources is chips from companies like AMD and NVIDIA. So the competitive advantages come from the following:

Superior Value with Lower Costs

Netweb reduces costs and improves efficiency by minimising reliance on third-party vendors and tightly integrating all system components.

The traditional approach: Companies buying AI infrastructure typically deal with fragmented vendors - one for hardware, another for management software, another for monitoring tools, and so on. Each vendor charges separate annual license fees that increase as the system scales, forcing customers to manage and renew multiple licenses from different players year after year.

Netweb’s unified approach: Since Netweb develops its own software and middleware (like Tyrone and Skylus), customers get a complete, integrated solution from a single provider.

Ethica Invest

Serious about long-term investing?

Unlock our professionally managed portfolios.

It provides a web-based interface for managing the entire cluster: provisioning nodes, monitoring health, and scheduling jobs. For a scientist at a research lab, Tyrone abstracts away the complexity of the underlying Linux command line, making the supercomputer accessible.

By owning and controlling the entire stack - hardware plus software - Netweb delivers better value to customers while maintaining operating margins of 14-15%, significantly higher than the industry standard of 9-10% or less.

Technical Optimisation and Rapid Deployment

The company builds servers on a dual processor design which enhances efficiency, speed and space utilisation. Netweb’s AI suites, such as Skylus.ai and Kubyts, bundled with servers, make for easy and fast installation.

Indigenous Design Capabilities

Most “Indian manufacturers” in the IT hardware space operate on a SKD (Semi-Knocked Down) or CKD (Completely Knocked Down) basis, essentially assembling kits imported from Taiwan or China. Netweb distinguishes itself by controlling the Design phase.

- PCB Design: Netweb designs its own server motherboards. This is non-trivial engineering. By owning the Gerber files (PCB design files), Netweb can modify the board layout to remove unnecessary components for specific government use-cases (enhancing security) or add specialised connectors.

- Thermal Engineering: AI servers run extremely hot. Netweb designs custom heatsinks and airflow baffles to ensure these systems can operate reliably in India’s often non-ideal ambient conditions.

The firm designs complex 24-layer printed circuit boards and proprietary software stacks in-house.

Aligned with India’s sovereign Goals

Governments worldwide are racing to develop their own AI models for strategic purposes and to enhance the welfare of their citizens. These are being built to provide training, enabling public-private partnerships, analysing data for welfare schemes, defence projects and nearly every other aspect.

Suffice to say, India, with significant talent, can be a forerunner for AI Tech. Netweb is a key partner in the National Supercomputing Mission (NSM) and the IndiaAI Mission. With an outlay of nearly 10,300 crores by the GoI, Netweb is among the top companies to garner a significant portion of this spending. Its major advantage is being a wholly owned Indian company, reducing the chances of technology falling in hands of other countries. The company has already provided systems like AIRAWAT, India’s fastest AI supercomputer

As a result, the company is among the few that are eligible for incentives under both the IT Hardware and Telecom & Networking PLI schemes of the Central Government.

NVIDIA Partnership

Netweb is NVIDIA’s only OEM partner in India, and it provides it with a significant advantage. This allows the company to get NVIDIA chips 12-24 months earlier than its competitors. During the fast-growing AI phase, this offers a high advantage. This is something similar to getting an iPhone 18 or even 19 when Apple just launched the iPhone 17.

Designing

The company has a significant advantage in designing PCBs and Kernels. The kernel is the software that joins the software and the hardware. A good design skillset leads to better integration and efficiency, making machines perform better than competitors.

Unlike traditional Electronic Manufacturing Services (EMS) companies that operate on thin assembly margins, Netweb commands a scarcity premium due to its proprietary intellectual property (IP): specifically the Tyrone software stack: and its elite status as NVIDIA’s primary manufacturing partner in the region, with priority access to next-generation chip architectures.

This ‘first-mover’ status allows them to deploy cutting-edge technology nearly a year before it becomes widely available in the general market, providing a significant competitive window in the high-stakes high-performance computing segment.

Future Growth Clarity (Capex):

In one of the previous concalls (May 2025), the management admitted that they will need another capex around FY27-FY28 as they are around 2,000 crore turnover. With the TTM figures already at 1,825 crores, this may need to be sped up to reduce the risk of operational bottlenecks and revenue losses. Now, the good thing is that the capex is not big when compared to the revenue generated, so it should not be difficult.

AI Industry Tailwinds

Since the AI industry is new and still in high growth phase, estimates for CAGR growth through 2030 range from 30% to 40%. Suffice to say, the tailwinds are pretty strong (Gale) for the companies in the space. With more and more high-speed computing needed, the macro trends are the least of worries for a company in this space.

Competitive analysis

Financials

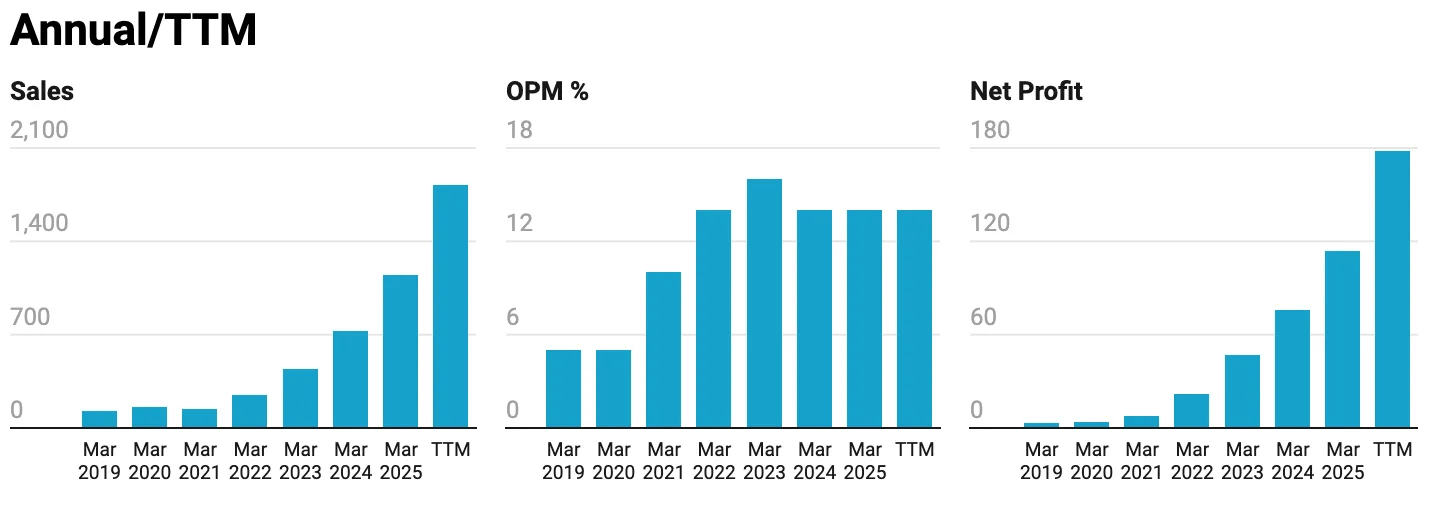

Netweb has performed pretty well over the past 5-6 years. It has grown at nearly 71% CAGR for the past 4.75 years, considering the latest 9-month results (ending December 2025).

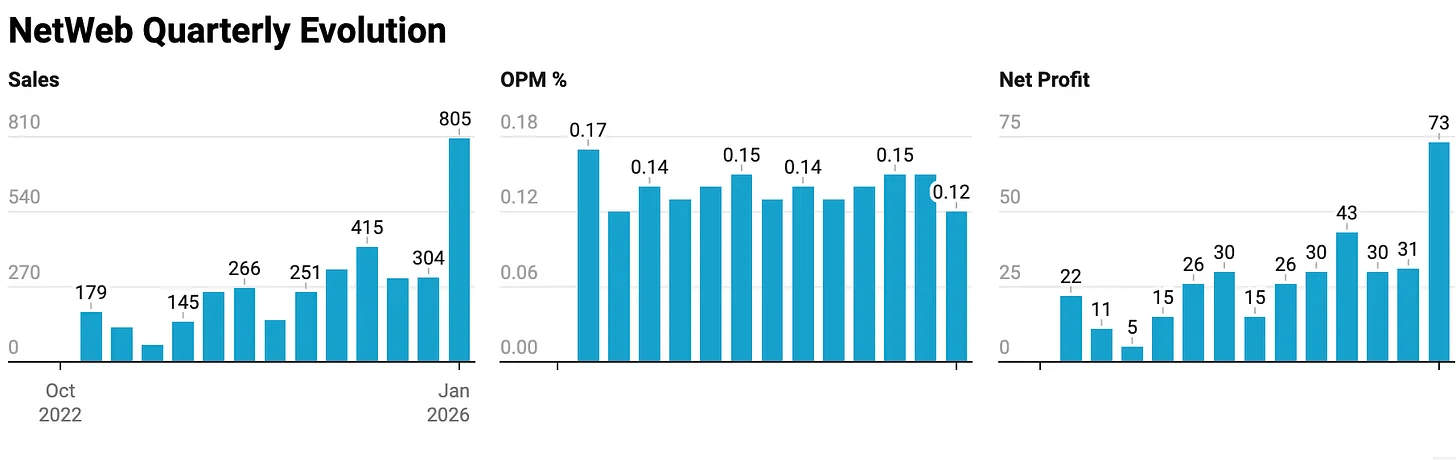

The quarterly results provide better insights into what is happening currently.

More often than not, the latter half of the financial year is better for the company, lending it a bit of cyclility. Q3 FY26 has been a good quarter for the company. Highlights of the quarter include:

- Revenue growth of 141% or 2.4X, on a YoY basis.

- The first nine months, 9MFY26, saw 92% growth YoY.

- TTM revenue is 1,825 crores compared to FY25 revenues of 1,149 crores.

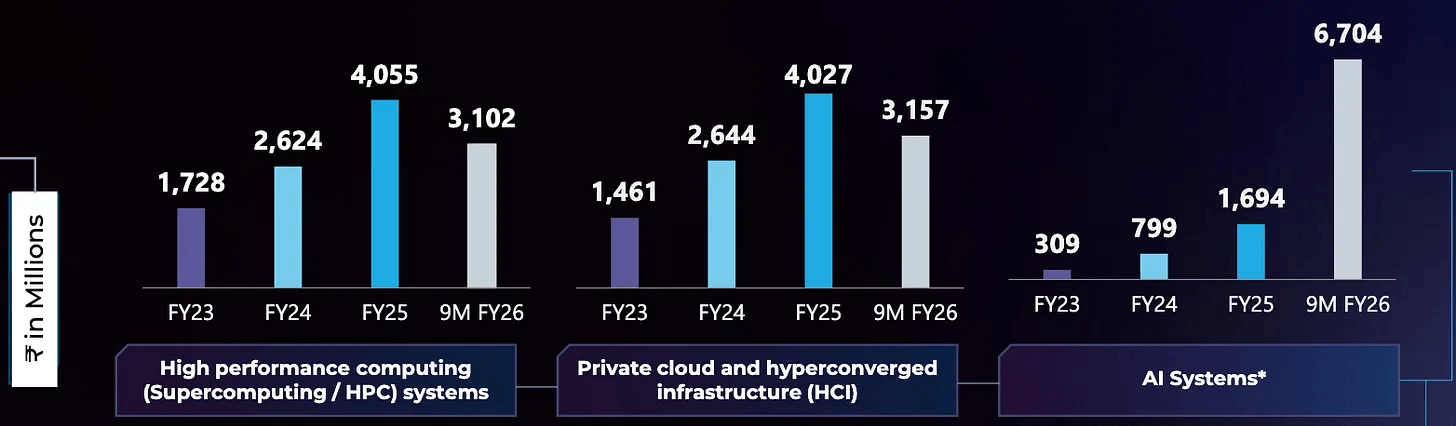

The growth came primarily from an increase in revenue from AI systems. AI revenue for the first nine months increased to approximately 4X, compared to the whole FY 25.

Supercomputing/High Power Computing (HPC) systems and Private Cloud/Hyper Converged Infrastructure (HCI) sectors have remained muted when we compare interpolated figures for the complete financial year from the first nine months.

However, this does not mean that these two sectors are a cause for concern. Some of the supercomputing and Cloud/HCI revenue can also be incorporated into AI systems, as the tech used has overlap. In the most recent con-call yesterday, the management indicated that these two sectors will see growth on an annual basis.

The record revenue was primarily driven by Netweb successfully executing a large strategic order valued at ₹450 crores, reaffirming its position as India’s largest OEM in high-end computing solutions.

Now the company’s execution cycle is on the lower side (8-16 weeks), so orders like this one are expected to be completed in one quarter. This enhances revenue for the quarter, but is also a risk since an order like this might not be available each quarter.

Margin Erosion

Operating margin decreases to 12.17% from the usual range of 14%-15%. Since the AI space is highly dynamic, the company has been expensing some R&D costs rather than capitalising them. In addition, the government projects tend to be lower margin, which has further reduced the margins.

But a higher margin is still forecasted because the company is driving towards higher-margin AI solutions, private cloud offerings, and incentives from the government PLI scheme for the Make in India initiative.

However, this margin is expected to improve when the non-government pipeline picks up again. Even accounting for lower margins on government projects, the margin is still higher than the competitors, which see a margin of less than 10%.

A Metric Snapshot

ROE and ROCE are doing pretty well at 23.9% and 32.4%. For the most recent quarter, Q3, FY26, these are much better at 30.5% and 41.3%.

Valuation ratios such as PE at 109X and EV/EBITDA at 73.7X seem high, even for a company in the tech space. Tech space companies can have PE ratios anywhere from 30s to 60s. There are PE ratios for companies like AMD at above 100, but those are generally outliers. It begs the question if the stock is overvalued.

However, two important considerations:

- Forward-looking perspective: As new earnings are reported, the P/E ratio should compress (decline), assuming the stock price remains stable. If the company’s earnings growth continues as expected, the valuation multiples will normalise over time.

- Historical context: Looking at the chart, the stock traded at much higher P/E ratios of 140-180x approximately two years ago, maintaining those levels for nearly a year. The P/E ratio then dropped sharply around the time DeepSeek was released (about a year ago). After a brief spike, it has settled back to levels similar to a year ago.

Conclusion: The current P/E of 109x, while appearing elevated in isolation, may not be excessively inflated when viewed in historical context. The stock has traded at significantly higher multiples before, suggesting the current valuation might be relatively moderate (or only slightly overvalued) for this particular company’s growth trajectory.

Capex

Capex is one thing that does not worry the management since the asset turnover is approximately 30X and is good until 2,500-3,000 crore annual revenue, as indicated during the con-call held yesterday. Even when needed, with a high turnover ratio, it is estimated to be minimal.

Challenges and Risks

- Order Inflow Dependence – Brief 8–16 week execution cycles mean orders need to keep coming in. Any cessation in orders can lead to revenues slowing and enhancing risk.

- Margin Pressure – Rising competition from large tech giants (HPE/Dell)and Indian IT firms in the HPC space and AI infrastructure is likely to affect margins.

- Reliance on Nvidia’s chips – High dependence on Nvidia’s GPUs makes Netweb vulnerable to supply chain disruptions or strategic changes. Although the partnership is solid, macroeconomic factors can still affect supply lines.

- AI Mission Uncertainty – The GoI’s AI mission outlay of Rs. 10,300 crore is a major opportunity, but the execution timeline remains unclear.

- Customer Concentration - Top 10 customers account for nearly 80% of the revenue, while the top 5 account for nearly 65% of the revenue. This enhances risk due to less diversification of customers. A customer moving away to the competitor will result in a significant revenue reduction.

Summary Snapshot

What lies ahead

We discussed the opportunities and the competitive advantages. The financials for the Netweb are pretty solid with a growth rate beyond management’s estimated of 35%-40%. Some important points that can be added to the investment thesis can include:

- A good relationship with NVIDIA/AMD which doesn’t seem to be going away anytime soon.

- Spending on R&D at 3% with more than 100 engineers engaged is likely to enhance competitive advantage.

- Open to working with new ASIC technology rather than chips, helping innovation and retaining a competitive edge.

- Valuation metrics, while still high, seem to have come back to the levels seen 1-2 years ago.

Enjoyed reading this? Ethica Invest works to provide investment options that have been screened for Ethical Compliance. If you found this interesting, please feel free to have a word with us. You can also get in touch with our SEBI registered Analyst for clarifications.

General Disclaimer and Release: Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any stock, investment product, vehicle, service or instrument.