Power Mech: Girders. Growth. Execution.

Electricity is part of our everyday life.

Lights come on with a casual flick of a switch, and we rarely think about it; until it doesn’t. Then we call our neighbours, check the meter, and suddenly notice how fragile the convenience was.

The process of making and delivering electricity can sound dull: big machines, long schedules, and lots of invisible work. That “boring” part; building, installing, testing and fixing the equipment that makes a plant run is what keeps the lights on.

And a company focused on that invisible work is Power Mech Projects Limited (PMPL).

Ethica Invest

Serious about long-term investing?

Unlock our professionally managed portfolios.

It doesn’t sell electricity. It builds and commissions boilers, turbines and control rooms, then maintains them so plants keep running safely and on time.

The business might look boring to you. But, the story is not.

Where PMPL stands today?

Power Mech today looks very different from its early, pure‑maintenance days. It has quietly moved from shutdown jobs and plant repair to becoming a full‑scale execution partner across the power and infrastructure value chain.

It now erects and commissions boilers and turbines, runs long‑term O&M contracts, executes heavy civil works, and operates large coal mines under MDO models. Its reach spans thermal power, renewables‑linked balance‑of‑plant, railways, water, mining and metals; diverse lines that share one common thread: disciplined execution at difficult sites.

Let’s walk through those segments, one by one.

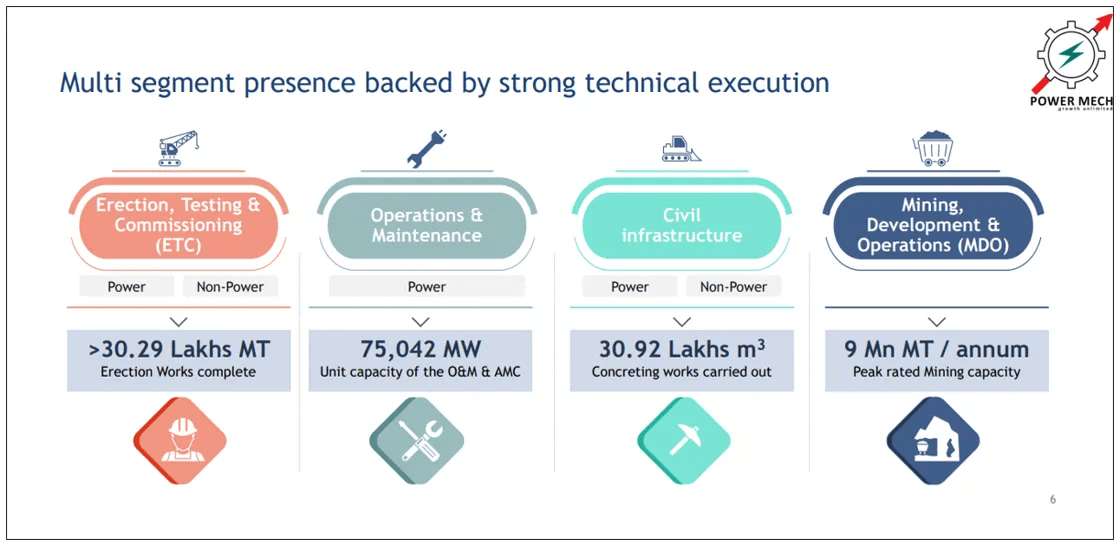

Segments

Erection, Testing & Commissioning (ETC) - turning drawings into running plants

In ETC, PMPL erects, tests and commissions boilers, turbines, generators (BTG) and balance‑of‑plant (BoP) systems not just for thermal power, but also for nuclear, oil & gas, petrochemicals, steel and mineral projects.

Think of it as assembling a jumbo jet on the runway and proving it can fly - only here, the “runway” is a power‑plant site, and the passengers are megawatts.

Commercially, ETC comes in waves. Big orders, chunky revenues, uneven timing. But it does something nothing else can: it earns trust. A utility that has seen you bring a troubled site back on schedule is far more willing to hand you the O&M, the next unit, or the tricky retrofit nobody else wants.

Operations & Maintenance (O&M)

O&M is the opposite of lumpy.

It is the “annuity engine”; long‑term contracts to run and maintain power and industrial plants day in, day out.

In plain terms, the company provides integrated mechanical, electrical and control‑room services; operating units from the control desk, handling boiler and turbine overhauls, and taking responsibility for uptime.

Ethica Invest

Serious about long-term investing?

Unlock our professionally managed portfolios.

Commercially, O&M matters because it offers recurring revenue, better visibility, and cross‑selling into new builds and retrofits.

Civil Infrastructure

Civil is the concrete and steel backbone, foundations, decks, cooling towers, roads, and broader urban and industrial infrastructure.

Power Mech’s civil work now stretches beyond plant foundations into metro, rail, water and township infrastructure. The company reports 30.92 lakh cubic meters of concreting and 15 lakh square feet of infra development completed in a single year at Vizag; a hint of how deep its civil execution bench has become.

Commercially, civil is where PMPL plugs into India’s infrastructure pipeline; power plants, rail‑linked townships, urban infra; and where its brand as a disciplined EPC contractor compound, even if margins can be tighter and working capital heavier in some packages.

Mining, Development & Operations (MDO)

MDO is the “next‑wave” segment; long‑duration mine development and contract mining built on the same project‑execution and O&M skills.

Here PMPL develops mine infrastructure, handles overburden removal, runs mineral processing, and manages contract mining operations.

In Q2 FY26, MDO still contributed a small share of revenue, but its percentage of the total is already up ~2 percentage points year‑on‑year, with management explicitly pointing to margin expansion as MDO scales.

Electrical & Other Adjacent Segments

Alongside the big four, PMPL runs electrical, rail, pipeline and overseas businesses that sit inside “infrastructure construction” and related categories.

This includes overhead electrification (756 track‑km commissioned), gas pipelines (546 km of cross‑country pipeline), GIS substations and transmission lines in states like Assam and Madhya Pradesh.

Overseas, the company has commissioned over 9,200 MW in the power sector and executed large piping volumes at industrial sites such as Dangote, Nigeria.

Power Mech’s journey is basically one long escalation of responsibility.

It began with the unglamorous end of the value chain; annual maintenance and shutdown jobs on power plants, fixing what others had already built.

And over time, those maintenance work naturally expanded into full ETC power projects.

Once that project‑execution muscle was proven inside power plants, stepping into civil, rail and water felt less like diversification and more like using the same discipline on new sites.

And as we concluded where PMPL stands today. Now, it's time to look at where it will go from now on because of the growth drivers the company holds.

Growth Drivers

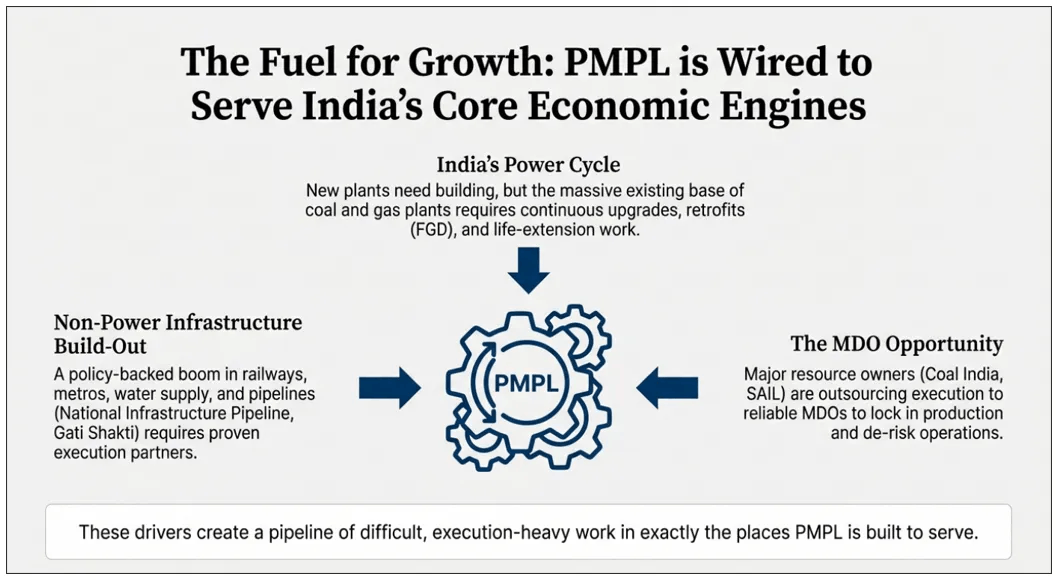

India’s power cycle: new plants, old workhorses

Even in a world talking non‑stop about solar and wind, India still runs on a backbone of coal and gas plants that can’t just be switched off and replaced overnight. These plants need periodic repairs, pollution‑control retrofits like flue gas desulphurisation (FGD), and life‑extension work to keep meeting grid demand and new emission norms.

Think of it like an old but reliable car in a family that now also owns an EV. The new battery car handles the short city runs, but the old diesel still does the long highway trips; as long as you keep servicing it, upgrading its brakes and cleaning up its exhaust.

Non‑power infrastructure: rail, water, urban, pipelines

Beyond power plants,

India is in the middle of a long, policy‑backed infrastructure build‑out; railways, metros, station redevelopment, water supply, pipelines, roads and urban projects under schemes like the National Infrastructure Pipeline and Gati Shakti.

This capex doesn’t need a “pure power” specialist; it needs contractors who can pour concrete, erect steel, lay pipelines and string cables, often in cramped, live environments.

Here PMPL plays the role of a multi‑tool.

It can take packages that mix civil (stations, depots, treatment plants), mechanical (pumps, conveyors, structural steel) and electrical (overhead electrification, substations).

Mining & MDO: long‑tail visibility

Large resource owners like Coal India or steel majors such as SAIL hire Mine Developer and Operators (MDOs) because they want to lock in production without bearing every ounce of execution pain. The MDO brings in project management muscle, takes on day‑to‑day mining and overburden removal, invests in equipment and often shoulders part of the operational risk, while the resource owner focuses on its core power generation or steelmaking.

Once a mine stabilises, it can run for 10–20 years or more, with fairly visible annual volumes and per‑tonne fees written into the contract.

PMPL’s own MDO work; like the Tasra coking coal block awarded by SAIL and the KBP coal mine for Coal India subsidiaries is structured exactly this way: long‑duration agreements for mine development, overburden removal, coal extraction, washing and dispatch.

Energy‑transition adjacencies: selling shovels in both camps

The energy transition doesn’t force PMPL to pick a side between coal and renewables; it mostly changes the type of “shovels” that need to be sold.

Older coal plants need FGD systems and emission controls to comply with norms, while renewable‑heavy grids need balance‑of‑plant work, grid connections, sometimes gas or battery‑based balancing capacity, and even EPC support for battery‑energy storage projects where PMPL has begun to win orders.

Putting together,

These growth drivers don’t promise a straight line; they promise a pipeline of difficult, execution‑heavy work in exactly the places PMPL is wired to serve.

Thermal plants that must be upgraded, infra that must be built, mines that must be run and grids that must be balanced all suit a company that specialises in making other people’s assets actually work, without owning them.

As we all know that with the setbacks, there follows drawdowns.

And here are the drawdowns for PMPL.

Risks

Big, complex projects and execution risk

PMPL’s strength is also a source of risk.

It takes on large, technically demanding EPC, infra and MDO projects where the downside of a misstep is meaningful. Rating notes explicitly flag significant execution risk in projects undertaken as “developer”, including MDO mines, a hybrid annuity (HAM) road project and renewable energy ventures.

In a fixed‑price or tightly bid contract, delays due to extended monsoon, land hand‑over issues, coordination failures or cost inflation can erode margins quickly.

The Q2 FY26 investor commentary, for instance, links a temporary slowdown in civil and electrical revenue to prolonged rains and delayed billings at key sites; a reminder that PMPL’s P&L is directly exposed to site realities it does not fully control.

The deeper risk is reputational. On marquee projects (large mines, major EPC packages), one visible failure can hurt future wins, especially with PSU clients who are conservative about counterparty track record.

Mining and development projects: leverage and “tail” risk

Long‑duration MDO and development projects are designed to improve earnings quality over time; but they also import new kinds of risk into the business. Lower‑than‑estimated revenue from MDO projects would be a negative trigger, because these contracts are expected to support margins and cash flows in coming years.

Mining brings concentrated exposure: to a specific block’s geology, clearances, local conditions and commodity cycles. If ramp‑up is slower than planned or regulatory terms shift, the heavy upfront investment in equipment and infrastructure can drag on returns and lock up capital for longer.

In simple terms, MDO can upgrade PMPL’s earnings profile if it works, but it can also magnify pain if assumptions on volume, cost, or pricing slip; and that risk sits on top of the normal EPC volatility.

But, to fight from the potential risks. PMPL holds its most important competitive advantage, that might defend the business from those risks.

Competitive Advantage

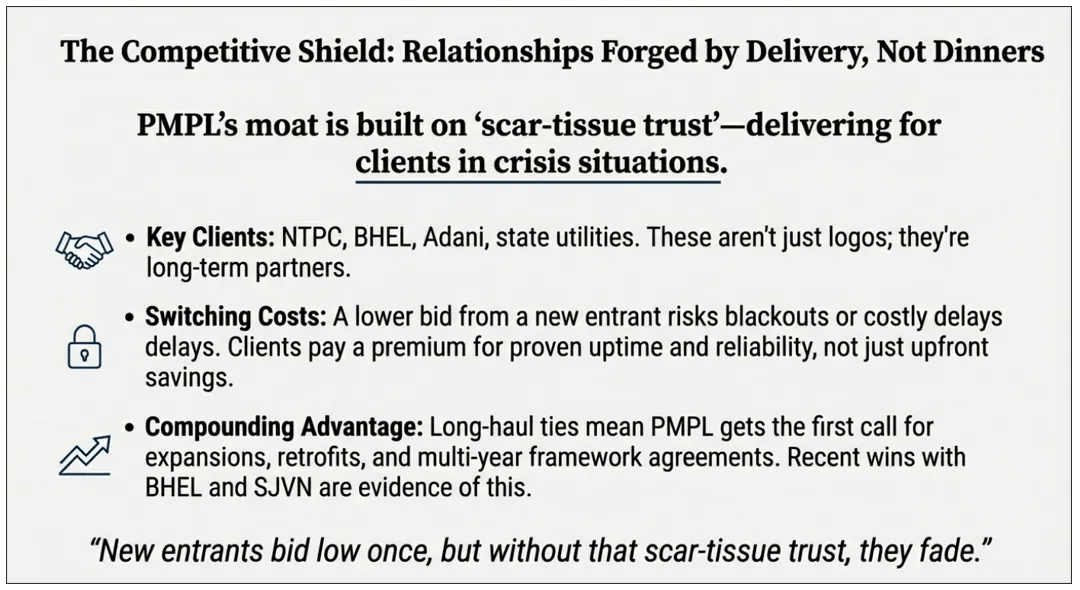

Relationships and Repeat Business

NTPC, BHEL, Adani, state utilities; these aren’t logos on a slide; they’re plants where Power Mech fixed crises at 2 AM, delivering when bids were forgotten. PSUs pre-qualify vetted players, framework agreements lock in multi-year work, O&M contracts stretch 5-10 years.

Switching?

A lower bid from a newbie risks blackouts or delays, clients pay for uptime, not savings. Long-haul ties mean Power Mech gets first dibs on expansions, like recent BHEL and SJVN wins, raising walls no discount jumps.

New entrants bid low once, but without that scar-tissue trust, they fade. Power Mech’s relationships compound through delivery, not dinners.

You might know that the narrative should match with the numbers. Otherwise, every business story is just another investment idea which is worth reading, but not worthy enough to put your money in.

And so, let’s go through the financials of PMPL to understand whether the narrative is actually matches with the numbers.

Financial Snapshot - What the Numbers Are Whispering

Growth & Scale:

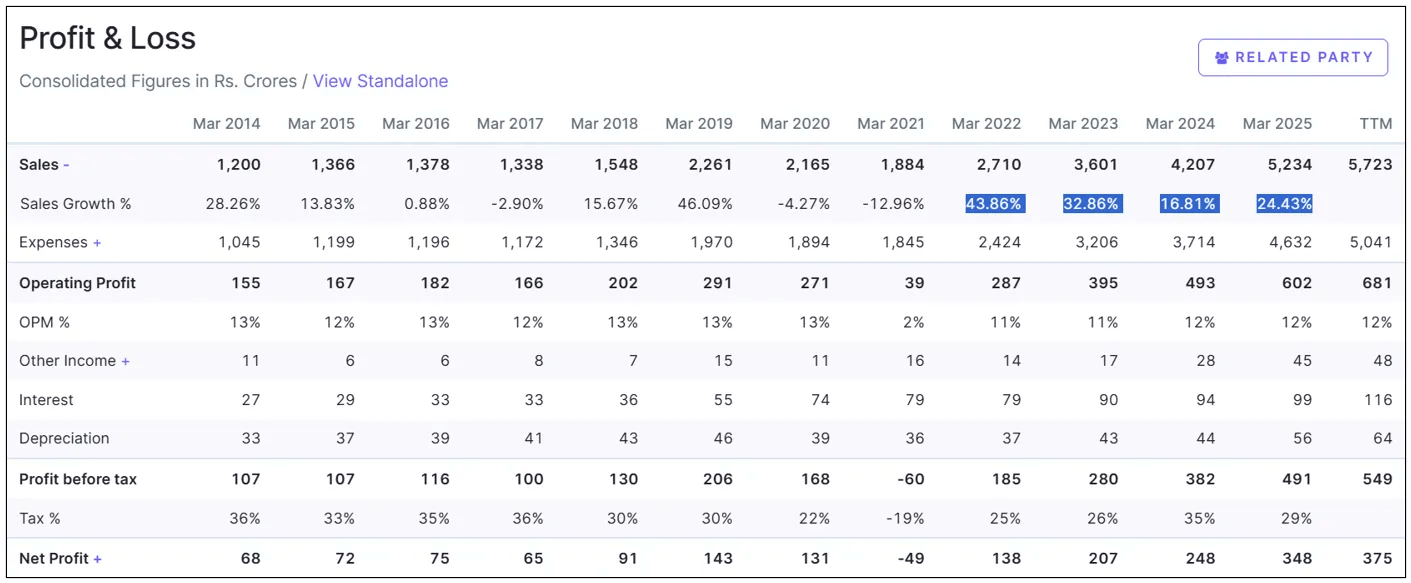

Power Mech’s top line has surged.

Revenue jumped from ₹2,710 Cr in FY22 to ₹5,234 Cr in FY25 (about a 25% CAGR). In H1 FY26 sales were ~₹2,531 Cr, up ~24% versus last year.

This storm of growth isn’t luck: it reflects a ramp-up in executing big power and infra contracts, plus new wins.

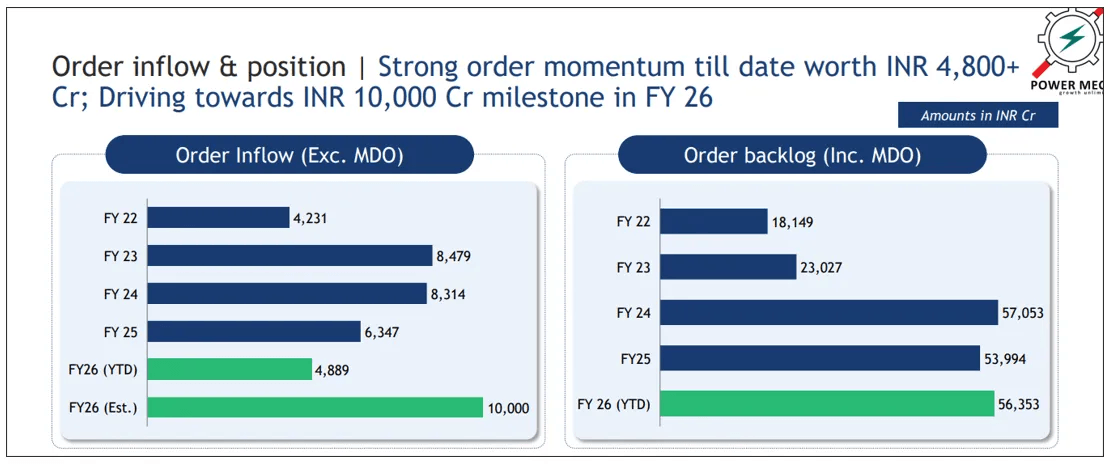

For example, the company highlighted ~₹4,800 Cr of new orders so far in FY26 (including marquee BHEL, Adani and SJVN projects). In effect, Power Mech is simply billing through more high-value projects (EPC orders, expansion into roads/water, long-term O&M and mining contracts), driving those strong numbers.

Margins and Business Mix:

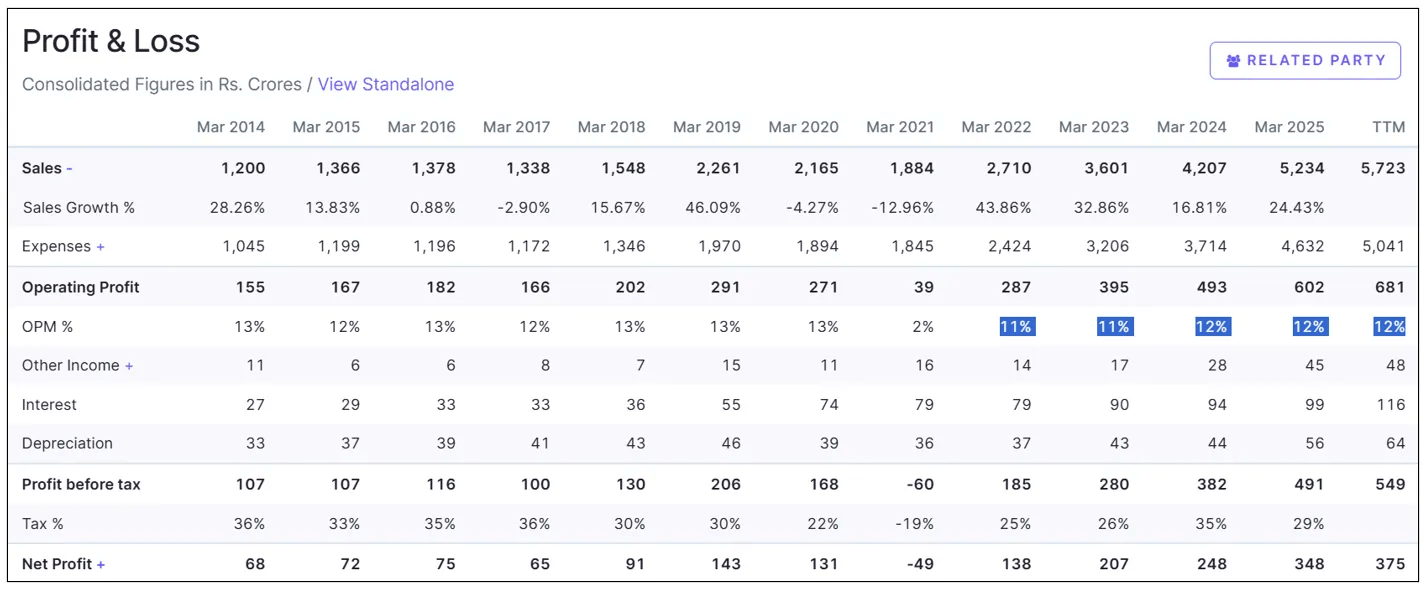

Even as scale grew, EBITDA margins stayed healthy.

Operating margins have hovered near the low teens (roughly 11–12%) through FY22–25.

A shift in mix helped.

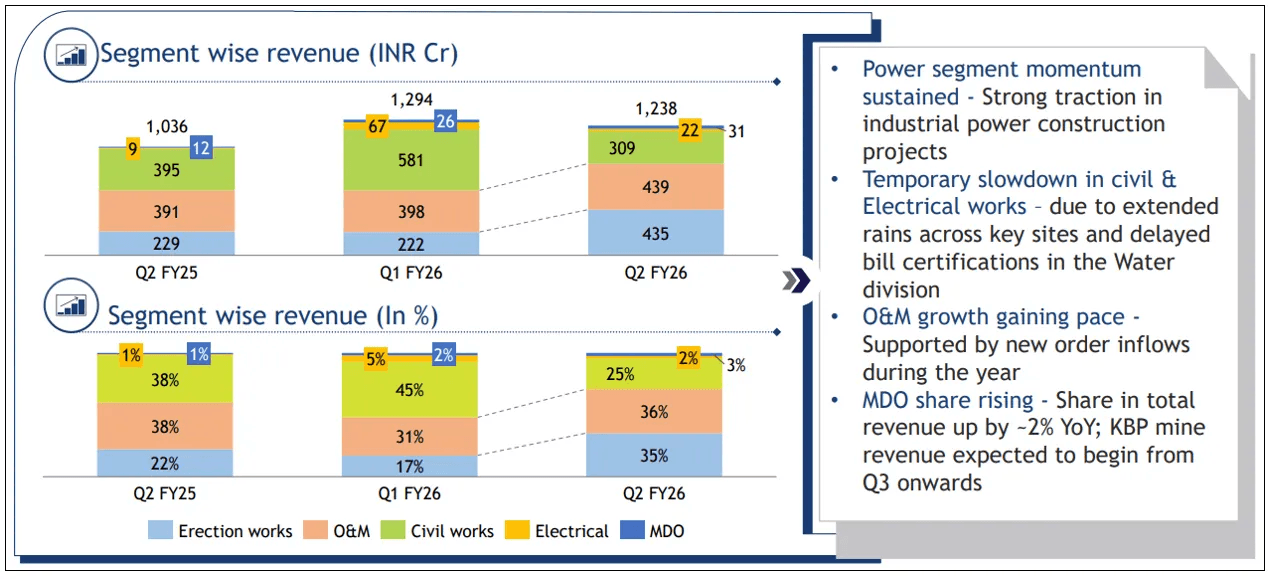

Civil &EPC work (generally lower-margin) is 61% of Q2 FY26 revenue, while O&M services (more annuity-like work) rose to ~36%, and new mining contracts began contributing (~3% in Q2 FY26).

In plain terms: more of the pie is coming from steady-service and mining, less from one-off civil projects.

Order Book and Visibility:

Backlog is strong.

As of Q2 FY26, Power Mech reported ~₹16,700 Cr of active orders (excluding mining contracts); that’s over 3 years of work at today’s run-rate.

In addition, high-margin mining development contracts (MDO) worth ~₹39,500 Cr are in play.

In other words, the company has multi-year revenue visibility: its current orderbook can keep the cranes swinging and engineers busy for years. This backlog, topped up by those big recent wins underpins forecast revenues and confirms that near-term growth is mostly locked in.

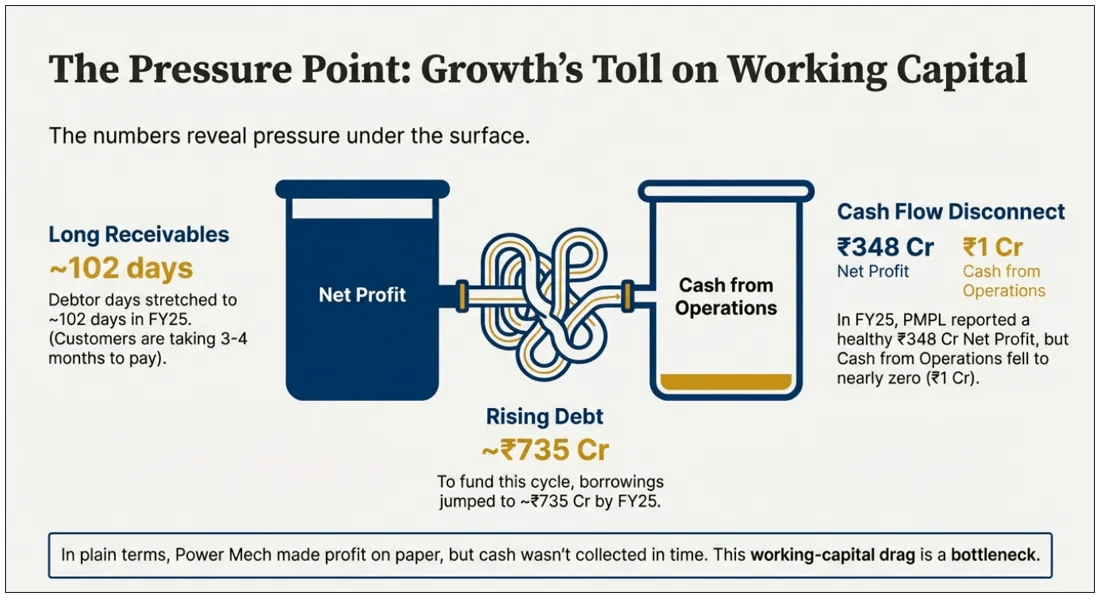

Balance Sheet, Working Capital and Cash Flows:

This working-capital drag (customers paying slowly) is a bottleneck. The company took on more debt to fund this cycle: borrowings jumped to ~₹735 Cr by FY25. Net leverage is not outrageous yet, but rising. Positively, ROCE stayed strong (around 23% in FY25), indicating the business still turns its capital effectively.

Wrap-up:

The financials confirm an execution-led growth model.

Order inflows and backlog are robust, fuelling healthy top-line jumps and steady mid-teens growth in core segments (O&M, erection, mining). Margins remain solid on the larger base, because of the business mix and tight execution control.

Where strain shows is in working capital: long receivables and nearly flat operating cash in FY25 signal a stress point.

In short, Power Mech’s strength is in winning and delivering big projects consistently (visible in the booming revenues and backlog), while its vulnerability lies in converting that work into cash on the books.

And, now let’s answer the final question. Does the business actually worth to be considered?

Valuations

Think of Power Mech as a reliable contractor who turns drawings into working plants and then stays on to keep them humming. That reliability shows up in steady revenue growth and a decent margin; numbers the company reported in FY25 and repeated in investor decks.

What you’re paying for is two things:

A repeatable execution machine (EPC + O&M) and;

A long-term optionality (mining/MDO contracts) that could turn into decades of steady cash.

The market’s current valuation; roughly P/E of 23 and EV/EBITDA of 10.7, treats those two features as “real but not guaranteed.”

The order book gives multi-year visibility and management has shown it can scale; that justifies paying a bit above average. But the company’s cash receipts have been lumpy; long receivable and unbilled cycles and a FY25 cash-flow wobble are real, practical problems. If collections improve and MDO ramps, the current multiple looks conservative. If cash conversion stays weak, the premium will feel expensive.

So, the market is saying: “We like the business, but earn our trust on cash collection and safe execution.” That’s a fair way to price a company built on doing the boring things very well.

This is not a recommendation, just a way to understand how the market is currently pricing the business.

About Ethica Invest

Ethica Invest is an ethical, Shariah-aligned investing platform that helps investors evaluate businesses through clearly defined financial, operational and governance filters. While rooted in Shariah principles, Ethica’s framework appeals across faiths by emphasising transparency, balance-sheet discipline and ethical business conduct.

Ethica Invest works with SEBI-registered analysts and investment professionals who provide structured, regulation-compliant insights into stocks and broader investment options. Readers who wish to understand PMPL from an ethical and long-term investing perspective, or who have broader questions around Shariah-compliant investing, can reach out to our Ethica team.

The objective is simple: help investors make informed decisions grounded in ethics, numbers and execution; not narratives alone.

General Disclaimer and Release: Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument.