Healing.

A simple word, but not a simple business.

In pharma, healing is built on hard things: clean rooms, approvals, audits, filings, stability data, process discipline, and years of patient execution before the market begins to trust you.

And when the disease is cancer, the bar rises further.

![]() Ethica Invest

Ethica Invest

Serious about long-term investing?

Unlock our professionally managed portfolios.

Because, cancer medicines are not ordinary pharma products. Some of them are toxic to handle. Some need sterile environments. Some must be freeze-dried. Some cannot be made in a normal factory without risking contamination or operator safety. This is why oncology manufacturing sits in a very different corner of the pharma world.

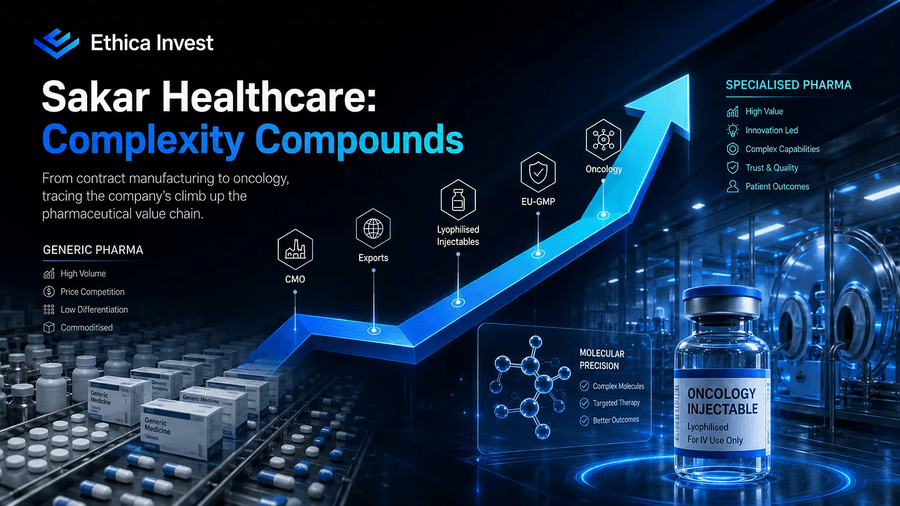

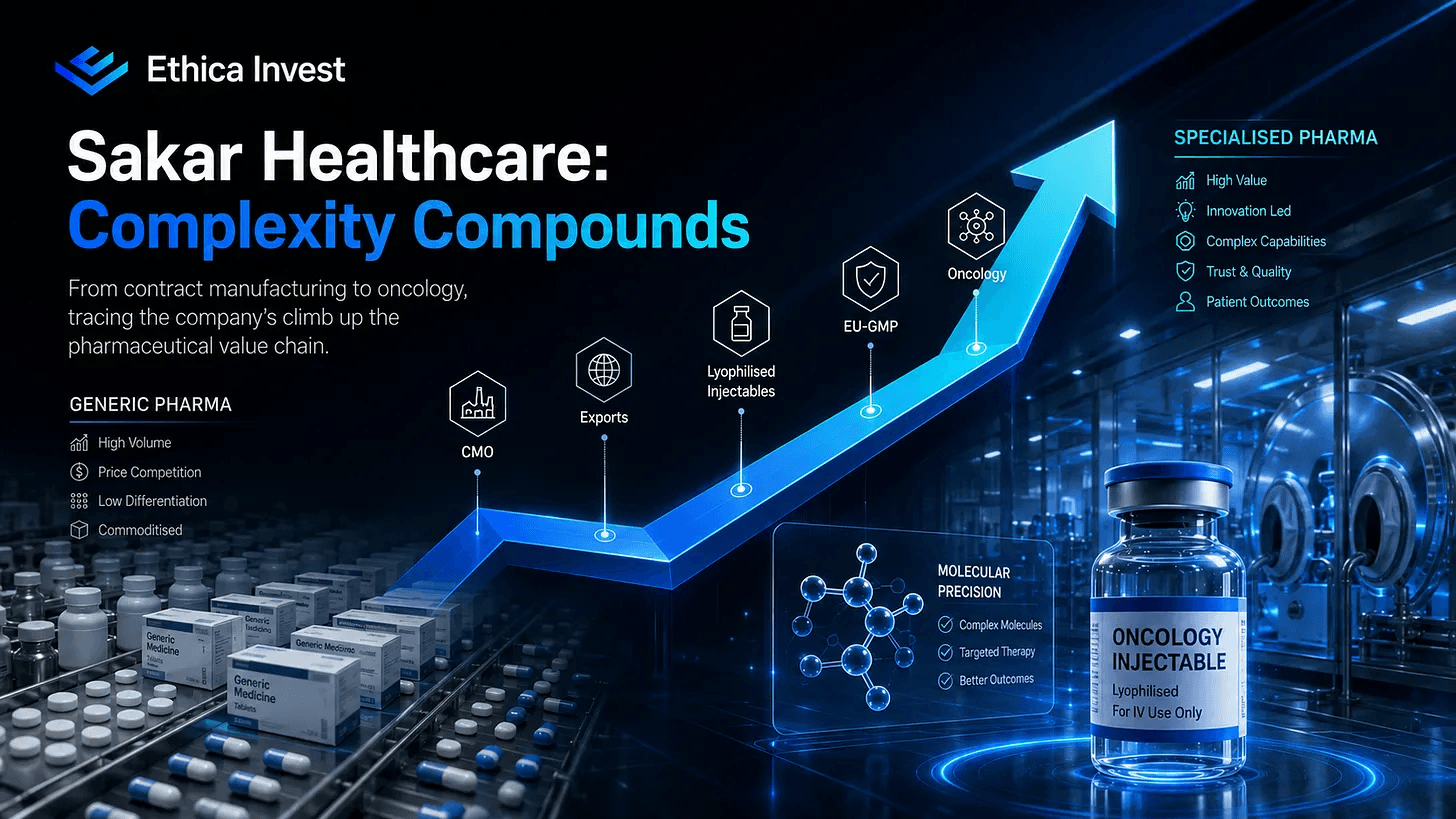

That is what makes Sakar Healthcare interesting.

The company is not just another small pharma name trying to sell more tablets. It is trying to move from a simpler contract-manufacturing identity into a more specialised, oncology-led, harder-to-replicate platform.

That transition is the real story.

And that is where the curiosity lies. Not in a flashy headline, but in a slow and deliberate transformation.

So before we talk about what Sakar Healthcare is today, it is worth asking how it became this way.

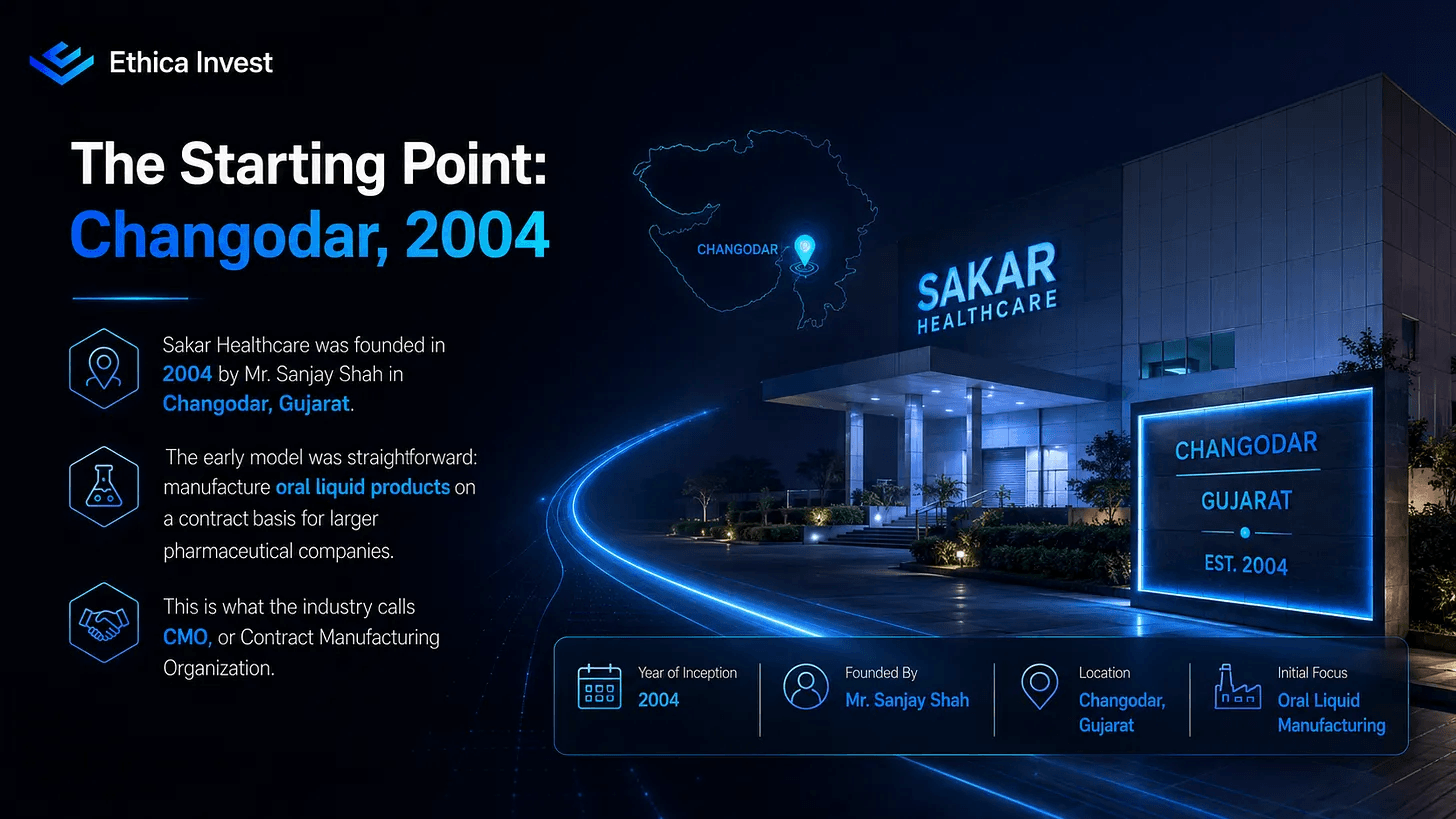

The Starting Point: Changodar, 2004

Sakar Healthcare was founded in 2004 by Mr. Sanjay Shah in Changodar, Gujarat.

The early model was straightforward: manufacture oral liquid products on a contract basis for larger pharmaceutical companies.

This is what the industry calls CMO, or Contract Manufacturing Organization:

You build the product, someone else owns the brand, takes the risk, and captures the premium.

It is not a bad business. But it has a hard ceiling.

Contract manufacturing is fundamentally a cost game. The client can always find someone cheaper. The manufacturer competes on price. Margins stay thin, and there is little compounding value; no brand, no IP, no regulatory moat.

Sakar operated in this space through its earliest years, building quality processes and earning its ISO 9001 certification. The team expanded the product portfolio steadily; adding small volume parenterals, dry powder injections, tablets, and capsules.

![]() Ethica Invest

Ethica Invest

Serious about long-term investing?

Unlock our professionally managed portfolios.

The company was developing manufacturing breadth.

The foundation was being laid. The strategic inflection had not yet arrived.

The Export Bet: Moving Beyond Domestic Contracts

In 2008, Sakar took a step that would define the next decade of its growth: it initiated export operations, beginning with African markets.

This was not a modest move for a company of its size.

Because, exporting requires regulatory compliance across multiple jurisdictions, a different quality language, and the willingness to absorb short-term costs in exchange for long-term market access.

But the logic was sound.

Domestic contract manufacturing kept you dependent on the domestic clients who hired you.

Own-brand exports:

Selling your own products into international markets under your own labels; fundamentally changed the value equation.

You owned the margin.

You owned the brand registration.

You built a customer relationship that was harder to replace than a contract.

Over the following years, Sakar expanded steadily across Southeast Asia, CIS countries, and Latin America.

By FY21, own-brand exports had grown to represent roughly 73% of net sales.

That transformation; from a domestic CMO to an export-led branded manufacturer; accounts for much of the revenue CAGR the company delivered through this period.

This was the business learning to price its own work.

Listing, Credibility, and the Technology Upgrade

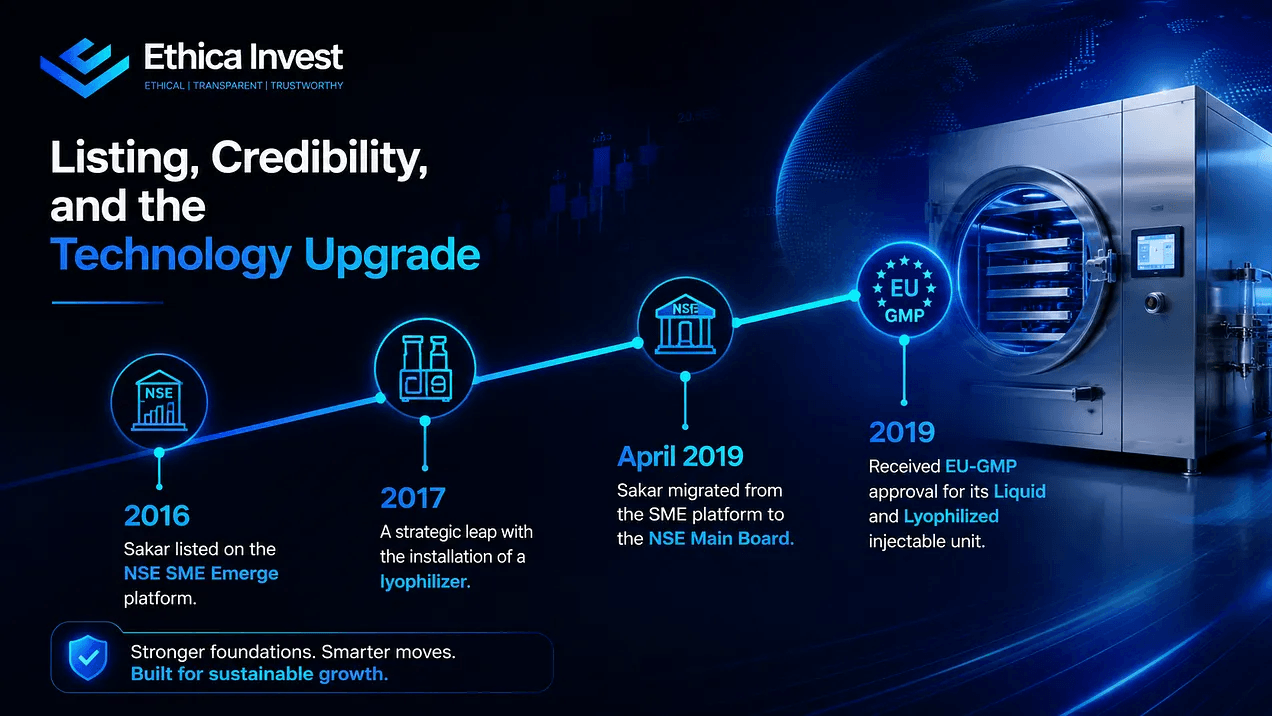

In 2016, Sakar listed on the NSE SME Emerge platform.

And a year later, in 2017, came a move that looked technical on the surface but carried meaningful strategic weight: the installation of a lyophilizer.

Lyophilized injections: also called freeze-dried injectables, are significantly more complex to produce than standard liquid injectables. They require specialized equipment, tighter quality controls, and a higher level of manufacturing expertise. They also command better margins and face less competition.

This was the first clear signal of where Sakar’s management wanted to take the business: toward complexity, toward value, and away from commodity.

By April 2019, Sakar migrated from the SME platform to the NSE Main Board. That same year, the company received EU-GMP approval for its Liquid and Lyophilized injectable unit.

The EU-GMP certification is not a routine compliance checkbox. It is the global benchmark for pharmaceutical manufacturing quality. Holding it opens access to European regulated markets, where price realizations are multiples of what semi-regulated markets offer.

The business model was working, and management knew it was time for the next, larger bet.

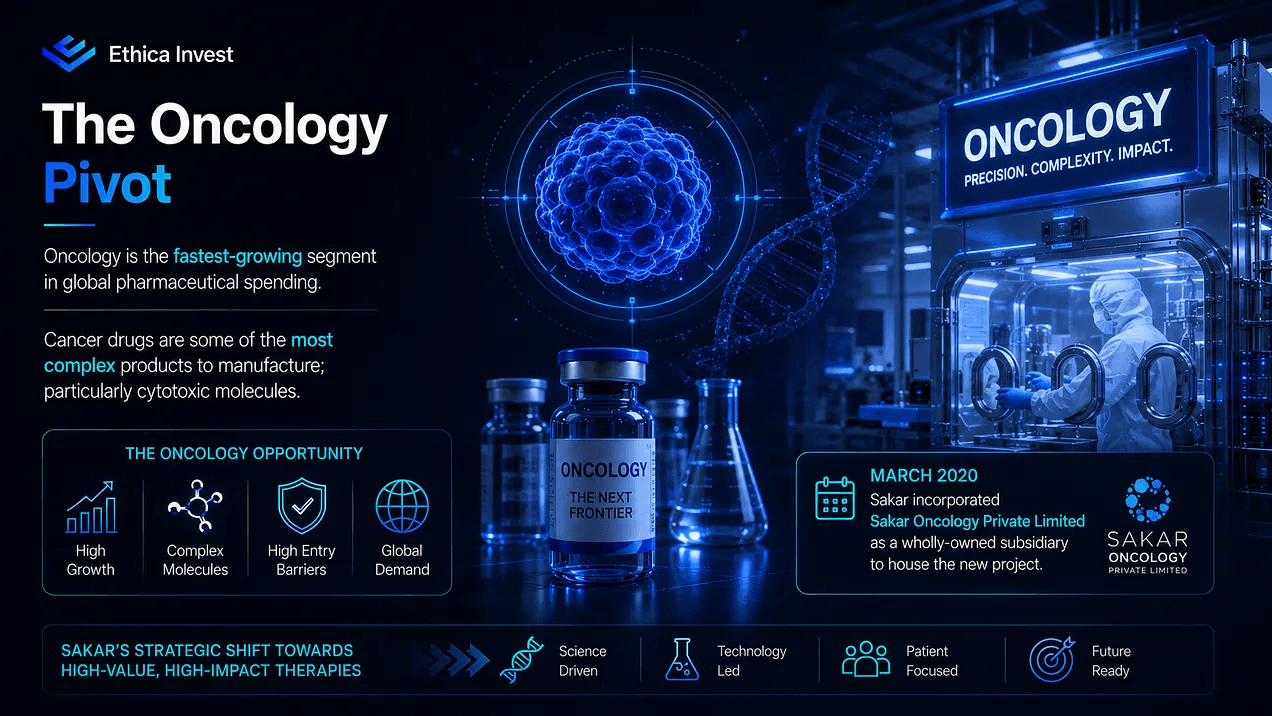

The Oncology Pivot: The Decision That Changes Everything

The decision to enter oncology was not arbitrary. It was analytical.

Oncology is the fastest-growing segment in global pharmaceutical spending. Cancer drugs are some of the most complex products to manufacture; particularly cytotoxic molecules, which require dedicated, isolated production environments because they are harmful to healthy human tissue.

That complexity is an enormous barrier to entry.

Very few facilities worldwide can produce them to the required standards. The manufacturers who can command premium contracts and long-term supply relationships.

In March 2020, Sakar incorporated Sakar Oncology Private Limited as a wholly-owned subsidiary to house the new project.

What followed was a multi-year, capital-intensive construction program: a greenfield oncology facility at Bavla, Gujarat, designed to produce both Active Pharmaceutical Ingredients and Finished Dosage Forms under the same roof.

This API-to-FDF integration is meaningful.

API stands for Active Pharmaceutical Ingredient. It is the core chemical that actually treats the disease.

FDF, or Finished Dosage Form, is the final medicine form a patient receives, such as a tablet, capsule, vial, or injection.

Most pharmaceutical manufacturers either make APIs or formulations. Doing both; controlling the entire production chain, gives you cost advantages, supply chain security, and flexibility that pure formulation players cannot match.

The ambition was clear. The cost was significant.

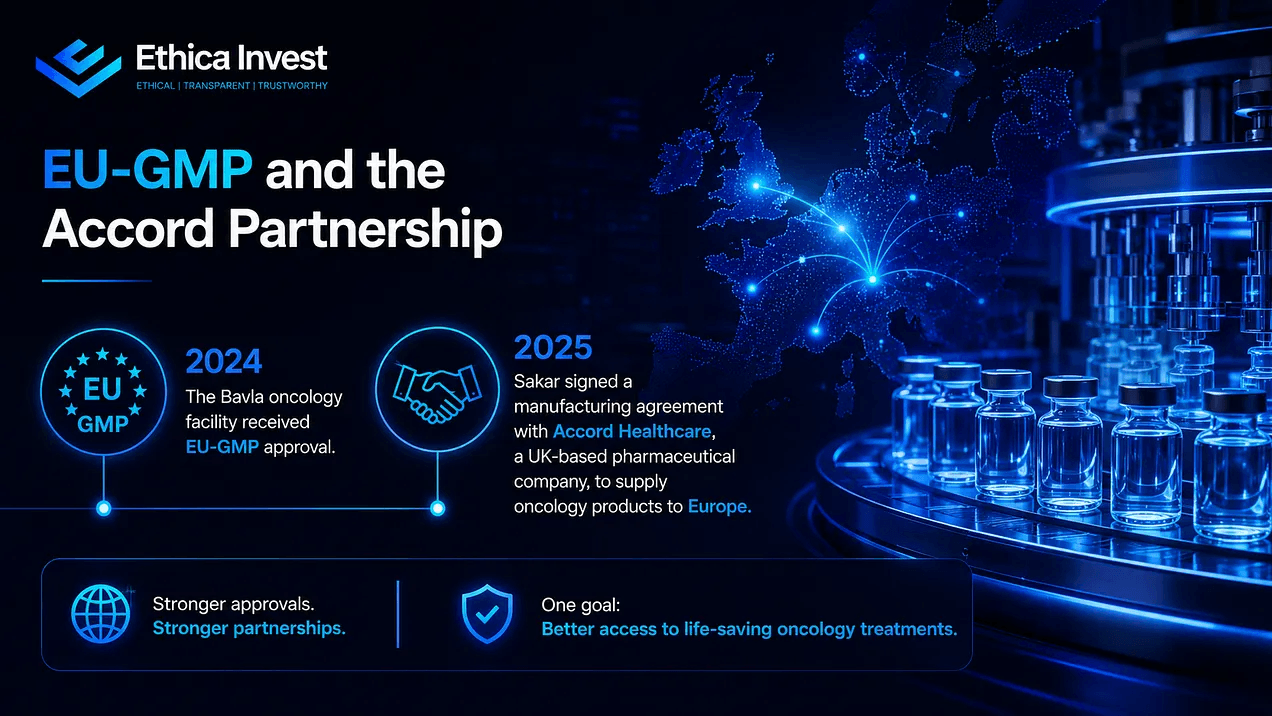

The Inflection Point: EU-GMP and the Accord Partnership

In 2024, the Bavla oncology facility received EU-GMP approval. This was the regulatory validation that unlocked everything.

GMP, or Good Manufacturing Practice, is the minimum manufacturing standard a medicine maker must meet. The European Medicines Agency says any manufacturer supplying medicines to the EU must comply with EU-GMP, and that medicines must be consistently high quality, fit for use, and aligned with their authorisation requirements.

For a small Indian company, an EU-GMP-approved oncology unit is not a casual credential. It is a passport into a more demanding, higher-trust part of the market.

By 2025, Sakar had signed a manufacturing agreement with Accord Healthcare, a UK-based pharmaceutical company, to supply oncology products to Europe. This was the first large-scale commercial validation of the Bavla facility’s potential.

The business had crossed the line from investment mode to monetization mode.

Now, Sakar’s own evolution makes sense only when seen against a broader change in pharma itself, where simple generics are losing ground to more specialised manufacturing.

Why the Pharma Industry Is Moving Up the Complexity Curve?

To understand Sakar, we first need to understand the pressure building inside Indian pharma.

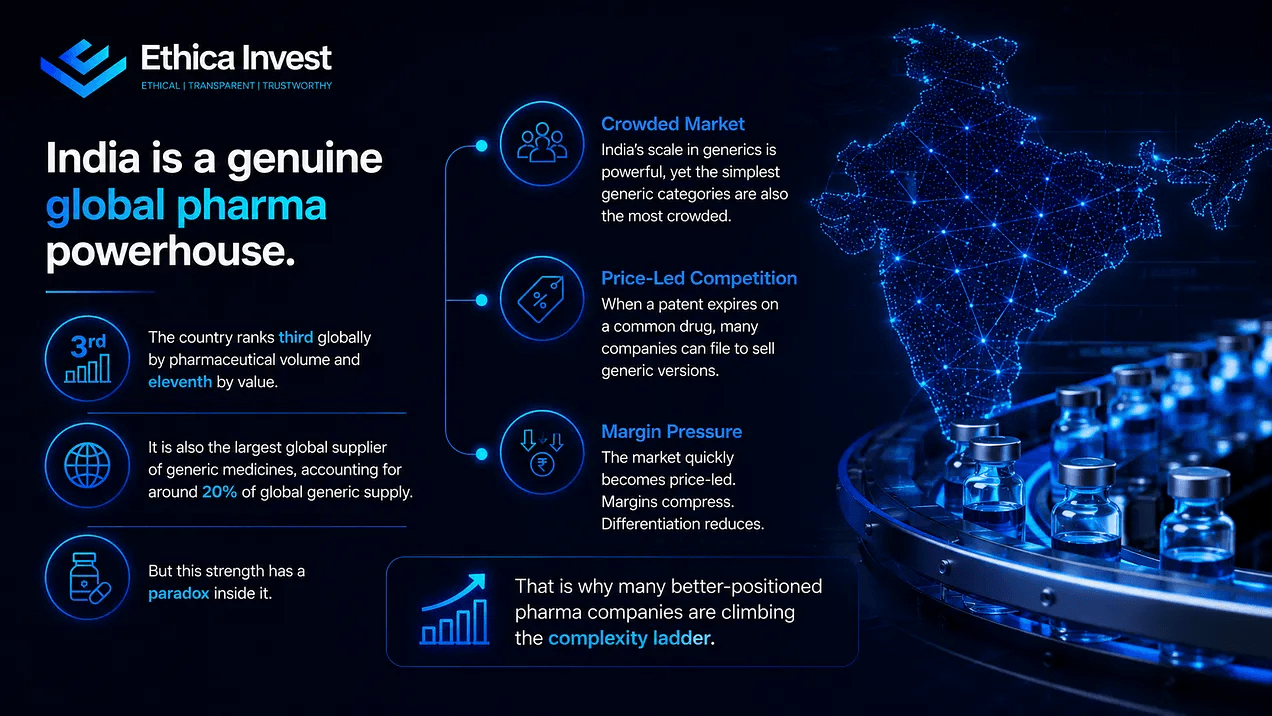

India is a genuine global pharma powerhouse.

The country ranks third globally by pharmaceutical volume and eleventh by value. It is also the largest global supplier of generic medicines, accounting for around 20% of global generic supply. Indian pharma exports reached about USD 30.5 billion in FY25, with exports going to 191 countries.

But this strength has a paradox inside it.

India’s scale in generics is powerful, yet the simplest generic categories are also the most crowded. When a patent expires on a common drug, many companies can file to sell generic versions. The market quickly becomes price-led. Margins compress. Differentiation reduces.

That is why many better-positioned pharma companies are climbing the complexity ladder.

The first step is moving from basic oral solids to sterile injectables.

Sterile injectables are harder because they must be made in extremely clean environments.

The next step is lyophilised injectables, which are freeze-dried medicines that need specialised equipment and tighter control.

And higher still sits oncology, especially cytotoxic oncology, where the products can be harmful to healthy tissue if not handled safely.

This is where the business changes. And the complexity becomes the moat.

And this is exactly the zone Sakar is trying to enter.

The Market Behind The Molecule

Oncology is the branch of medicine dealing with cancer.

Within pharma, oncology has become one of the most important and fastest-growing therapy areas.

The demand side is clear.

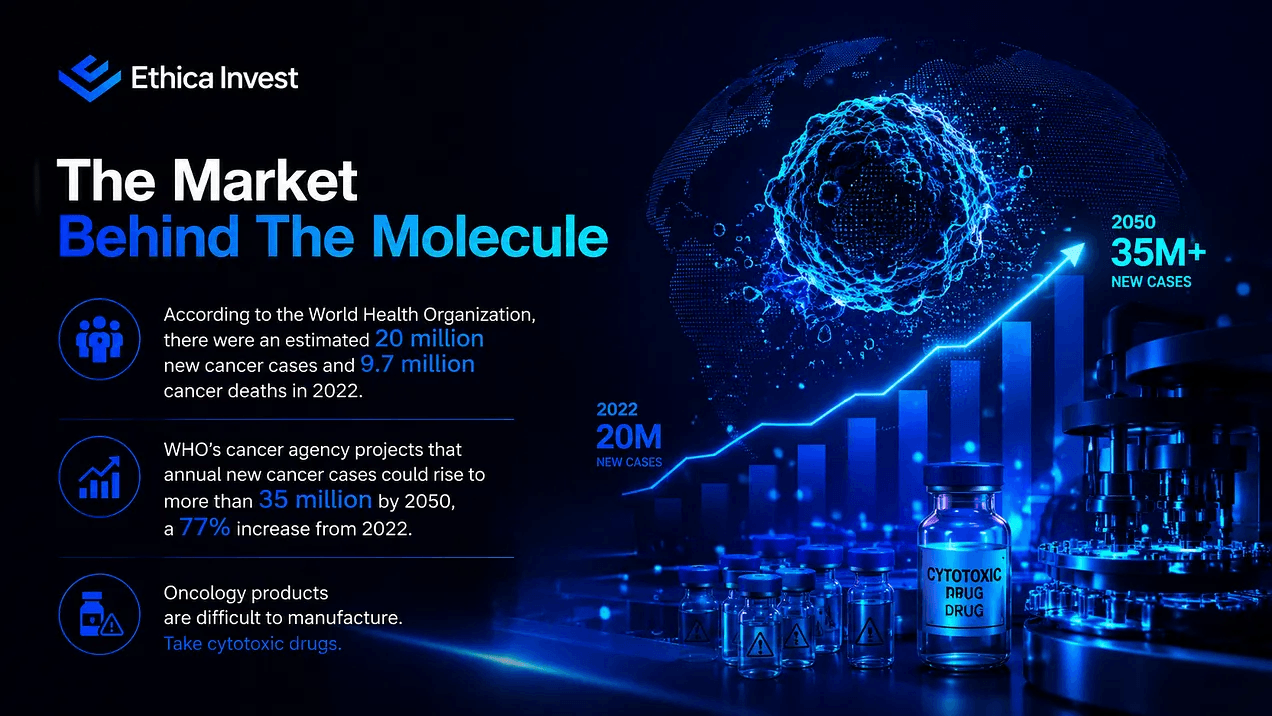

According to the World Health Organization, there were an estimated 20 million new cancer cases and 9.7 million cancer deaths in 2022. WHO’s cancer agency projects that annual new cancer cases could rise to more than 35 million by 2050, a 77% increase from 2022.

The spending side is equally important.

IQVIA estimates that global cancer medicine spending at list prices rose to USD 252 billion in 2024 and could reach USD 441 billion by 2029.

But oncology is attractive not just because the market is large.

It is attractive because many oncology products are difficult to manufacture.

Take cytotoxic drugs.

These are drugs designed to kill or damage rapidly dividing cancer cells. The problem is that they can also harm healthy cells. So the manufacturing environment has to protect the medicine, the worker, and the outside environment at the same time.

This is why oncology facilities are usually dedicated facilities. A company cannot simply decide to make cytotoxic injectables in an ordinary plant. It needs purpose-built infrastructure, trained people, validated systems, regulatory inspections, and a long approval trail.

A normal pharma factory is like a clean kitchen where hygiene matters.

A cytotoxic oncology plant is more like a controlled laboratory where the ingredient itself must be contained at every step.

And this is where EU-GMP matters.

Now, Sakar already have it with its oncology unit at Bavla.

Visual idea: A simple diagram showing three protection layers in cytotoxic manufacturing: product protection, worker protection, and environment protection.

And that approval is an important door-opener.

Sakar’s Place in the Value Chain: Not the Easy End

It is important to be precise here.

Sakar is not a global innovator discovering new molecules. It is not spending billions on early-stage cancer research. Its role is different.

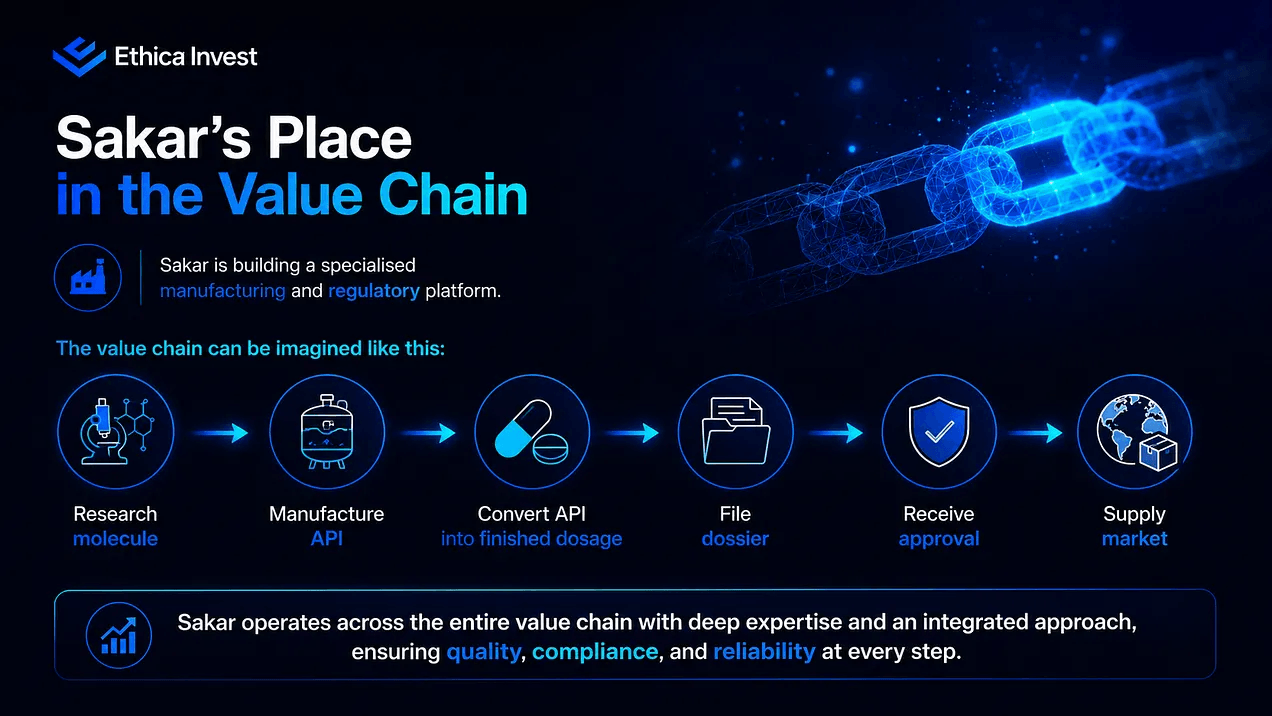

Sakar is building a specialised manufacturing and regulatory platform.

It works around known oncology molecules, develops product dossiers, manufactures APIs and formulations, and supplies products through models such as CMO, CDMO, out-licensing, technology transfer, and partner-led market access.

CMO; Contract Manufacturing Organisation; simply means manufacturing for another company.

CDMO; Contract Development & Manufacturing Organisation; goes one step further and includes development or technical support before manufacturing.

In simple words, Sakar is trying to be the trusted maker behind complex oncology products.

Most companies do not handle all parts equally well.

Some make APIs. Some make finished dosages. Some own registrations. Some depend on partners.

And for Sakar, let’s go deep into it.

Bavla: Infrastructure as Strategy

In pharma, moving up the value chain means; spending the money, building the facility, winning the approval, and then converting that approval into orders.

For Sakar, its Bavla facility is that move.

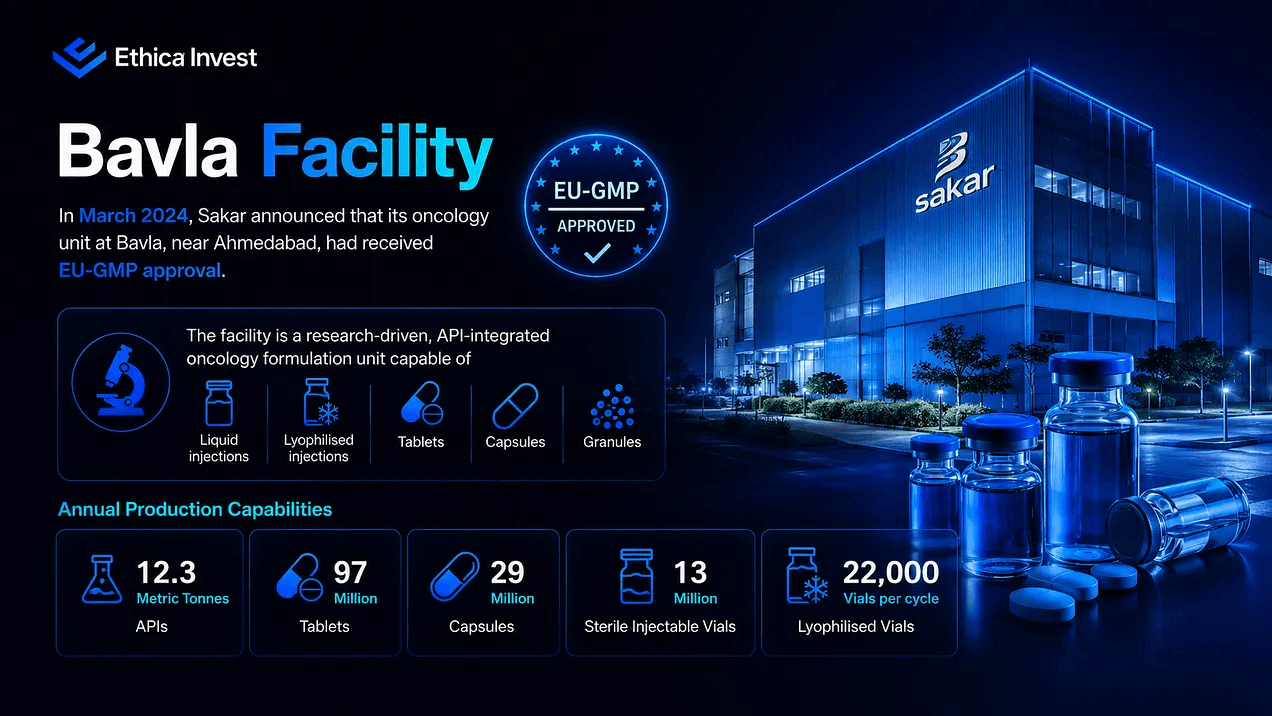

In March 2024, Sakar announced that its oncology unit at Bavla, near Ahmedabad, had received EU-GMP approval.

The company described it as a research-driven, API-integrated oncology formulation unit capable of liquid injections, lyophilised injections, tablets, capsules, and granules.

The facility Capacity is actually meaningful.

The annual production capabilities of 12.3 metric tonnes of APIs, 97 million tablets, 29 million capsules, 13 million sterile injectable vials, and 22,000 lyophilised vials per cycle.

These details matter because they show that Sakar is not merely adding one new product line.

It is trying to build a platform.

And a platform is different from a product.

A product gives you revenue from one molecule. A platform allows you to develop, file, approve, and commercialise multiple molecules over time.

That is also why the capex phase can look uncomfortable before it starts looking attractive.

A new facility brings depreciation, interest cost, staff cost, and validation cost before it brings full revenue. For a few years, the income statement carries the burden while the commercial engine is still warming up.

The payoff comes only if approvals and utilisation follow. In Sakar’s case, FY26 suggests that the platform has started moving from promise to proof.

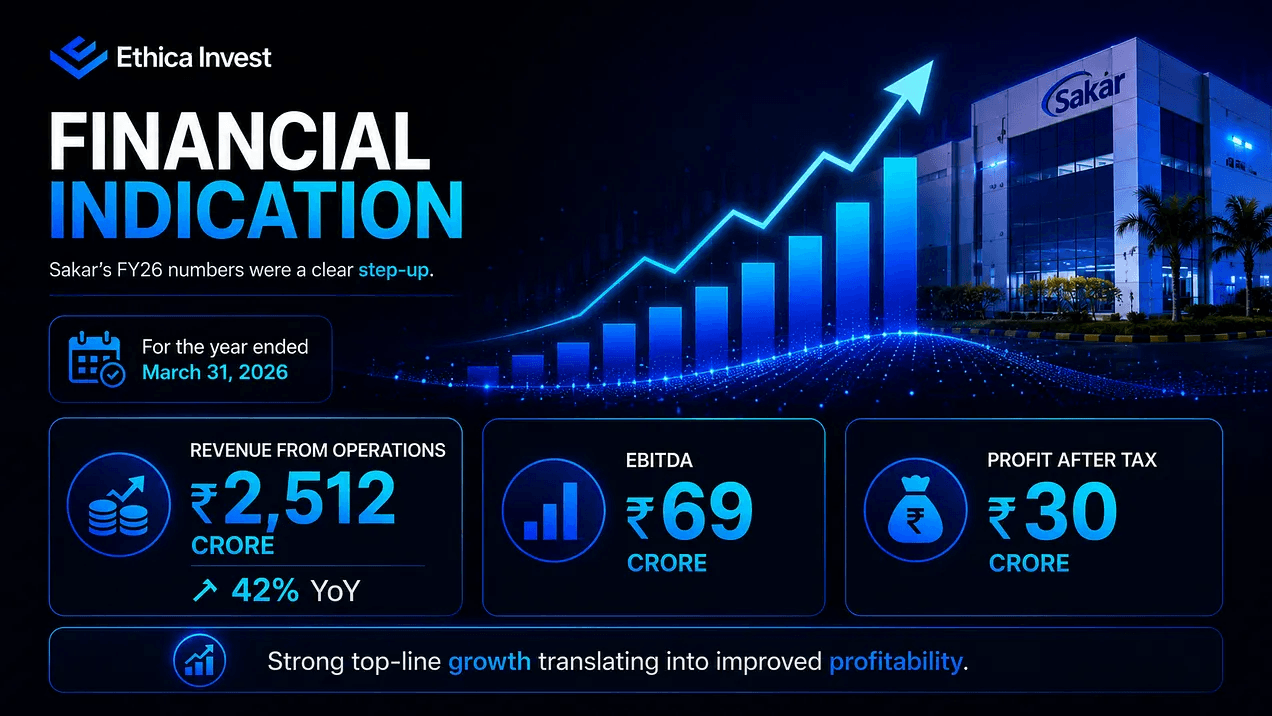

When the oncology thesis began showing in numbers

Sakar’s FY26 numbers were a clear step-up.

- For the year ended March 31, 2026, revenue from operations was Rs 2512 crore, up 42% yoy.

- EBITDA was Rs 69 crore.

- And profit after tax was Rs 30 crore.

In Q4 FY26 alone;

- Revenue was Rs 71 crore, EBITDA margin reached 37%, and PAT margin stood at 16%.

These numbers indicate that the company is beginning to absorb the fixed costs of the oncology facility. In capital-intensive manufacturing, once the plant is built and approved, additional volumes can add disproportionately to profit if pricing and quality remain strong.

The management commentary also points in that direction.

In the Q4 FY26 call, the company said;

Oncology contributed around 38% of total FY26 revenue”. It also said, “exports are expected to become the dominant contributor over the medium term as more approvals convert into commercial supplies.

This is the key line for investors to track: approvals converting into commercial supplies.

A marketing authorisation is not revenue by itself. It is permission to sell. The real value is created when that permission turns into orders, repeat supplies, partner confidence, and better capacity utilisation.

Sakar’s FY26 update shows progress on this front.

The company said, “it had completed over 60 business contracts with oncology products, had more than 35 discussions ongoing, had shared 250 dossiers globally, had submitted 125, and had received 12 marketing authorisations from regulatory authorities”.

In other words, the regulatory pipeline is no longer theoretical. It is beginning to convert.

Commercial validation: why partners matter

In pharma, especially in regulated markets, a partner relationship is not like a casual distribution agreement.

A serious pharma customer will look at the site, the quality system, the dossier, the supply reliability, and the regulatory history before depending on a manufacturer.

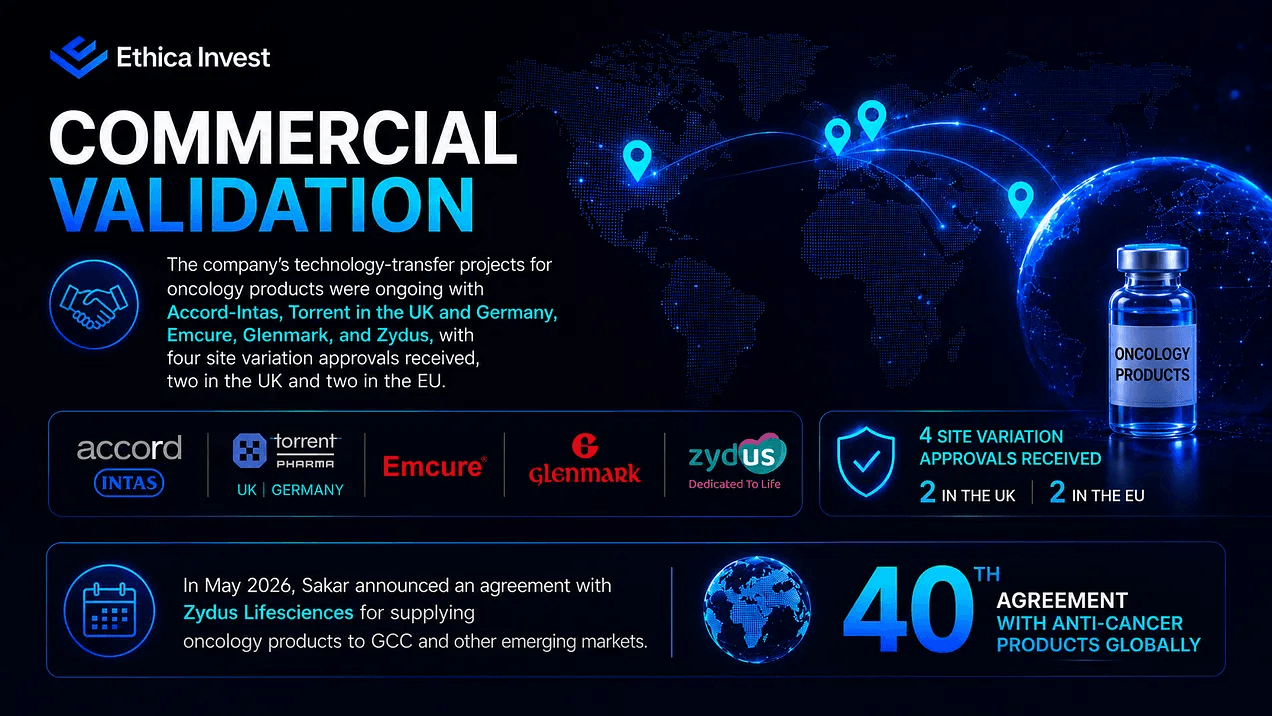

This is why Sakar’s partner list matters.

The company’s technology-transfer projects for oncology products were ongoing with Accord-Intas, Torrent in the UK and Germany, Emcure, Glenmark, and Zydus, with four site variation approvals received, two in the UK and two in the EU.

In May 2026, Sakar announced an agreement with Zydus Lifesciences for supplying oncology products to GCC and other emerging markets.

This marked the company’s 40th agreement with anti-cancer products globally.

It also disclosed 23 EU marketing-authorisation filings, 13 own MAs applied in the EU, 33 site variations submitted with global partners, and 21 APIs developed in-house.

This simply mean that Sakar is increasingly being evaluated by serious customers for serious products.

For a company of Sakar’s size, credibility is built in layers: first facility, then approval, then dossier, then partner, then order, then repeat order.

Now, the focus shifts from proof of concept to the actual triggers that can grow the business from here.

What Could Move This Business Forward?

The thesis for Sakar should not be reduced to one vague sentence like “oncology has huge potential.”

That is not enough.

The real question is: what specific developments can push revenue and profit higher?

1. Dossier Conversion.

A dossier is the technical file submitted to regulators. It contains the data that proves a medicine can be made consistently and safely. More dossiers do not automatically mean more sales, but they expand the number of products and markets Sakar can legally address. As more dossiers move from “shared” to “submitted” to “approved,” the addressable business widens.

2. Marketing Authorisations.

A marketing authorisation is the approval to sell a specific medicine in a specific market. This is the bridge between R&D and commercial revenue. Sakar’s 12 marketing authorisations as of FY26, along with additional EU filings and site variations, are important because they create multiple entry points into regulated and semi-regulated markets.

3. Capacity Utilisation.

This is perhaps the most powerful lever. Sakar’s Bavla oncology facility could potentially generate Rs 800–1,000 crore in revenue at optimal utilisation over four to five years, without significant incremental capex, while current utilisation remains low.

That statement should be treated as management ambition, not as certainty.

But the logic is sound. If the building, equipment, approvals, and teams are already in place, then rising volumes can improve margins because fixed costs get spread over a larger revenue base.

4. Export-Market Expansion.

Sakar is not only selling domestically. Oncology exports are already underway to markets such as the UK, Mauritius, Lebanon, Algeria, and several African countries, while Europe is expected to be the initial focus for phased regulated-market commercial exports.

Exports matter because regulated markets usually reward quality and approval status more than purely price-led domestic segments. They also increase the value of Sakar’s EU-GMP credential.

5. New Product Launches.

The Bavla facility supports multiple oncology dosage forms: oral solids, oral liquids, liquid injectables, lyophilised injectables, and APIs. The company has also pointed to more complex work such as liposomal, HME-based, and differentiated oncology formulations.

Liposomal formulations use tiny fat-like carriers to deliver drugs, while HME, or hot-melt extrusion, is a technique that can help improve the usability of hard-to-dissolve molecules.

These are not just scientific words. They indicate an attempt to move into products where formulation know-how matters.

In pharma, a more difficult product often means fewer competitors and better economics, at least until the market crowds in.

6. Partnerships.

Partners like, Accord, Torrent, Emcure, Glenmark, Zydus, and others are not just names. Each relationship can become a demand channel. If more partners validate the facility and more products move through technology transfer, Sakar can reduce dependence on any one molecule or customer.

7. Product Mix.

As oncology becomes a larger share of revenue, the company’s margin profile can change. Management has indicated that oncology contributed 38% of FY26 revenue and expects oncology to become the core growth engine.

That mix shift is important because it changes the identity of the business.

A company with 10% oncology revenue is still mainly a general pharma manufacturer. A company moving toward 40%, 50%, or more from oncology begins to be valued and analysed differently.

What to Watch?

No thesis worth taking seriously ignores what can go wrong.

1. The gap between approval and revenue.

A dossier approval or marketing authorisation gives the right to sell. It does not guarantee sales, pricing, payment, repeat orders, or market share. Investors should watch actual oncology revenue, not just approvals.

2. Execution at scale.

Sakar is no longer running only a simpler formulation business. It is managing regulated-market filings, oncology manufacturing, cytotoxic safety systems, export markets, technology transfers, partner audits, and product launches. This requires stronger systems and management bandwidth.

3. Partner concentration.

The Accord Healthcare partnership is a significant commercial relationship, and at this stage of the oncology division’s development, a limited number of such relationships are carrying a disproportionate share of the revenue. If any key relationship underperforms, is restructured, or is disrupted for any reason, the impact on near-term oncology revenue could be material. As more commercial partnerships are built, this risk naturally diminishes; but that diversification still needs to be proven.

4. Pricing pressure over time.

Complex oncology generics command better margins than simple generics, but they are not immune to competition as more manufacturers build cytotoxic capability and more products come off-patent. The manufacturers that stay ahead of that curve are the ones that continuously move into newer, more complex molecules. That requires ongoing investment in product development, dossier pipeline management, and technical R&D; capabilities that Sakar is building but has not yet tested at serious scale.

None of these risks make the thesis invalid.

They make it conditional.

And conditions need to be tracked carefully.

Closing View: From Survival To Identity

Sakar Healthcare’s story is not about sudden transformation. It is about a slow climb.

The company began in a practical part of pharma: manufacturing useful products, building quality discipline, and serving customers across domestic and export markets.

That business gave it survival.

Own-brand exports gave it better market access.

But oncology is the part that can potentially give it a sharper identity.

And, the Bavla facility is the centre of that identity. EU-GMP approval gives it credibility. API-to-FDF integration gives it control. Dossiers and marketing authorisations give it market access. Partnerships with larger pharma companies give it validation. FY26 numbers suggest that the operating leverage has begun to appear.

Still, the next phase will be more difficult than the last. Building a facility is one challenge. Filling it with profitable, repeat, regulated-market business is another.

That is why Sakar should be watched through a few simple questions:

- Are dossier submissions converting into approvals?

- Are approvals converting into launches?

- Are launches converting into repeat exports?

- Is oncology becoming a larger share of revenue?

- Are margins improving because of real utilisation, not one-off factors?

- Are partnerships broadening beyond a few names?

- Is compliance staying clean?

If the answers keep improving, Sakar may no longer be seen as just another small pharma manufacturer. It may be seen as a specialised oncology platform emerging from India’s broader shift toward complex, high-trust pharmaceutical manufacturing.

That is the real story.

Not just growth.

A change in identity.

About Ethica Invest

Ethica Invest is a principled, Shariah-compliant investment platform that helps investors like you in identifying companies using well-defined criteria for finances, operations, and governance. Though grounded in Shariah guidelines, Ethica’s approach goes beyond any single faith by prioritizing openness, strong balance sheets, and responsible business practices.

Ethica Invest works with SEBI-registered analysts and seasoned investment experts who deliver organized, compliant analysis on stocks and other opportunities. Those interested in seeking more on Shariah-aligned investing, can connect with our Ethica team.

The goal is straightforward: empower investors with decisions based on ethics, solid data, and performance; not just stories.